Tonic Water Market Overview - Definition, scope, and significance

Tonic water is a carbonated soft drink that contains quinine, which gives it a distinctive bitter flavor. Originally developed as a medicinal beverage to prevent malaria, tonic water has evolved into a popular mixer in cocktails, particularly with gin. The tonic water market encompasses various product types, including plain and flavored varieties, as well as different categories such as low/no sugar and regular formulations. The market serves both on-trade (bars, restaurants, hotels) and off-trade (retail stores, supermarkets) channels. This beverage category holds significant importance in the global beverage industry due to its unique position as both a standalone drink and an essential cocktail ingredient, contributing to the growing premium mixer segment and the craft cocktail movement.

Tonic Water Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The tonic water market is driven by several key factors including the growing cocktail culture and premiumization trend in the beverage industry. The increasing popularity of gin and tonic as a classic cocktail has significantly boosted demand for tonic water. Health-conscious consumers are driving demand for low/no sugar options, creating opportunities for manufacturers to innovate with natural sweeteners and reduced-calorie formulations. However, the market faces restraints such as the bitter taste of quinine, which may not appeal to all consumers, and the availability of substitute beverages. Challenges include maintaining product quality and consistency, managing raw material costs, and navigating regulatory requirements for quinine content. Opportunities exist in emerging markets, product innovation with unique flavors and botanical infusions, and expanding into new consumption occasions beyond traditional cocktail mixing.

Tonic Water Market Growth Trends - Current and emerging trends shaping the market

The tonic water market is experiencing several notable growth trends. Premiumization is a key trend, with consumers increasingly willing to pay more for high-quality, artisanal tonic waters made with natural ingredients and unique flavor profiles. The craft mixer movement has gained momentum, with small-batch producers offering innovative botanical blends and exotic flavor combinations. Health and wellness trends are driving demand for low-calorie, sugar-free, and naturally sweetened tonic water options. Sustainability is becoming increasingly important, with consumers seeking products with eco-friendly packaging and responsibly sourced ingredients. The ready-to-drink (RTD) cocktail segment is also influencing the market, with manufacturers developing pre-mixed gin and tonic beverages for convenience. Additionally, the expansion of premium bars and restaurants globally is creating new opportunities for premium tonic water brands.

COVID-19 Impact on the Tonic Water Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the tonic water market, primarily due to the closure of bars, restaurants, and hospitality venues during lockdowns. The on-trade segment experienced a sharp decline in sales as social distancing measures and restrictions on gatherings limited in-person dining and drinking occasions. However, the off-trade channel saw increased demand as consumers shifted to home consumption, with many experimenting with cocktail making at home. E-commerce channels experienced growth as consumers turned to online shopping for beverages. The market demonstrated resilience through product innovation and marketing strategies focused on home consumption occasions. As restrictions ease and the hospitality sector recovers, the tonic water market is expected to regain momentum, with a potential lasting impact being the normalization of home cocktail culture and increased demand for premium mixers.

Tonic Water Market Competitive Landscape - Major competitors and market consolidation

The tonic water market features a mix of global beverage giants and specialized craft producers, creating a dynamic competitive landscape. Major players like The Coca-Cola Company leverage their extensive distribution networks and brand recognition to maintain significant market share. Specialized brands such as Fever-Tree have disrupted the market with premium positioning and innovative flavor profiles, successfully capturing the growing demand for high-quality mixers. The competitive landscape is characterized by product differentiation strategies, with companies focusing on unique botanical blends, sustainable sourcing, and premium packaging to stand out. While there has been some consolidation through acquisitions of craft brands by larger companies, the market remains relatively fragmented with opportunities for niche players. Competition is intensifying as new entrants seek to capitalize on the craft mixer trend and emerging markets present growth opportunities.

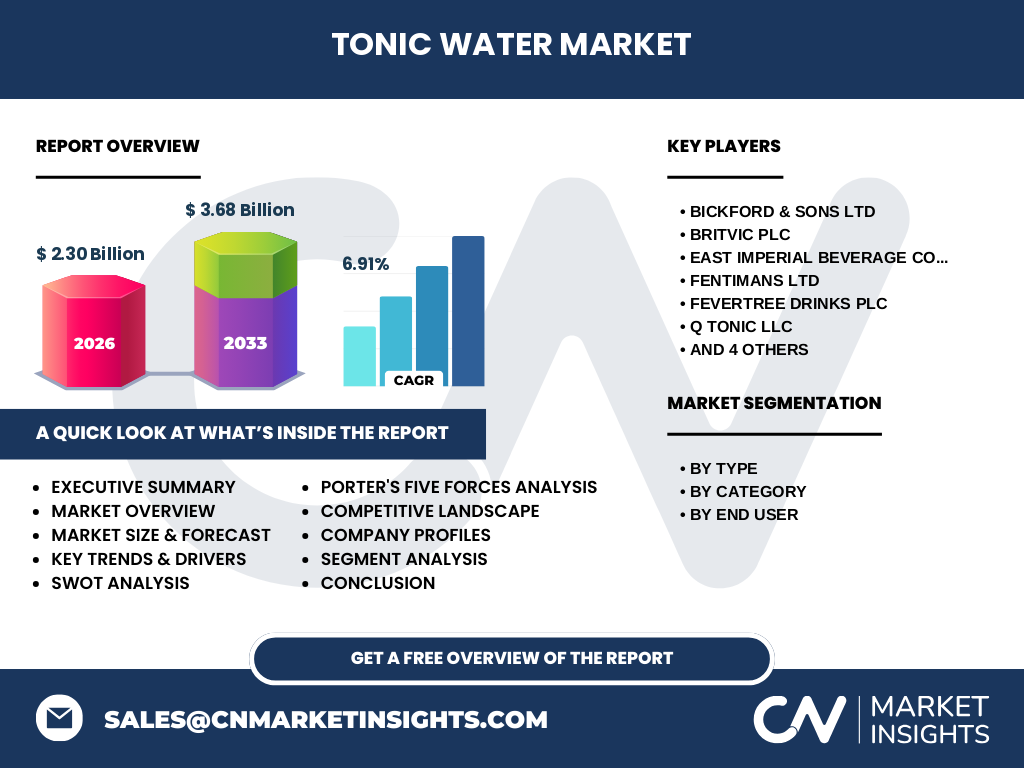

Executive Summary - High-level overview and key findings about Tonic Water Market

The global tonic water market is experiencing steady growth, driven by the premiumization trend in the beverage industry and the enduring popularity of gin and tonic cocktails. With a market size of $2.30 billion in 2026 and projected to reach $3.68 billion by 2033, representing a CAGR of 6.91%, the market demonstrates robust expansion potential. Key growth drivers include the rising cocktail culture, increasing demand for low/no sugar options, and product innovation in flavors and formulations. The market is segmented by type (plain and flavored), category (low/no sugar and regular), and end user (on-trade and off-trade), each presenting unique opportunities. While the COVID-19 pandemic temporarily impacted on-trade sales, the market has shown resilience through increased home consumption and e-commerce channels. The competitive landscape features a mix of global giants and craft producers, with premiumization and sustainability emerging as key differentiators. Regional analysis reveals varying growth rates, with emerging markets presenting significant opportunities for expansion.

Tonic Water Market Forecast - Projections for 2025-2032 period

The tonic water market is projected to experience steady growth from 2025 to 2032, with the market size expected to increase from $2.30 billion in 2026 to $3.68 billion by 2033. This represents a compound annual growth rate (CAGR) of 6.91% over the forecast period. The growth trajectory is supported by several factors, including the continued expansion of the cocktail culture, increasing consumer preference for premium and craft beverages, and the rising demand for low-calorie and sugar-free options. The on-trade segment is expected to recover and grow as bars and restaurants resume normal operations post-pandemic, while the off-trade channel will likely maintain its momentum driven by home consumption trends. Product innovation, particularly in flavored and botanical-infused tonic waters, is anticipated to drive market expansion. Emerging markets in Asia-Pacific and Latin America are expected to contribute significantly to growth, as Western drinking culture influences local consumption patterns. The premium segment is forecasted to outpace the standard segment in terms of growth rate, reflecting the broader trend towards premiumization in the beverage industry.

Tonic Water Market Size and Share by Segmentation - Breakdown by {segmentData}

The tonic water market is segmented by type, category, and end user, each contributing differently to the overall market size and share. By type, the market is divided into plain and flavored tonic water. Plain tonic water currently holds a larger market share due to its traditional use as a mixer and its established consumer base. However, flavored tonic water is experiencing faster growth as consumers seek variety and unique taste experiences. By category, the market is split between low/no sugar and regular tonic water. The low/no sugar segment is gaining significant traction, driven by health-conscious consumers and those monitoring sugar intake, and is expected to capture an increasing share of the market. By end user, the market is categorized into on-trade (bars, restaurants, hotels) and off-trade (retail stores, supermarkets). The off-trade segment currently dominates the market share, a trend accelerated by the COVID-19 pandemic and the shift towards home consumption. However, the on-trade segment is expected to recover and grow as the hospitality industry rebounds.

Global Tonic Water Market Size and Share by Region - Geographic distribution

The global tonic water market exhibits varying growth patterns and market shares across different regions. North America and Europe currently represent the largest markets, driven by established cocktail cultures and high consumer awareness of premium mixers. These regions benefit from a strong on-trade presence and a growing trend towards craft and artisanal beverages. The Asia-Pacific region is emerging as the fastest-growing market, fueled by increasing westernization of drinking habits, rising disposable incomes, and a growing middle class. Latin America and the Middle East & Africa regions show moderate growth, with potential for expansion as cocktail culture gains traction and distribution networks improve. Within regions, there are significant variations in market maturity and consumer preferences. For instance, the UK market is characterized by a strong craft gin and tonic culture, while the US market shows growing interest in flavored and botanical tonic waters. Regional market shares are influenced by factors such as local drinking traditions, economic conditions, and the presence of key market players.

Regional Analysis of the Tonic Water Market - Detailed regional market performance

The tonic water market's regional performance varies significantly, reflecting diverse consumer preferences, economic conditions, and cultural factors. In North America, particularly the United States, the market is characterized by a strong demand for premium and craft tonic waters, driven by the growing cocktail culture and interest in high-quality mixers. The region benefits from a well-established on-trade sector and high consumer awareness of premium beverage options. Europe, especially the UK, shows a mature market with a deep-rooted gin and tonic tradition. The region is witnessing growth in flavored and botanical tonic waters, catering to evolving consumer tastes. The Asia-Pacific region presents the most dynamic growth, with countries like Australia, Japan, and Singapore leading the way. Rapid urbanization, increasing disposable incomes, and the influence of Western drinking culture are driving market expansion. In Latin America, markets like Brazil and Argentina are showing increasing interest in premium mixers, although the market is still developing compared to North America and Europe. The Middle East & Africa region faces unique challenges due to alcohol restrictions in some countries, but non-alcoholic tonic water consumption is growing, particularly in urban areas and among younger consumers.

Leading Company Profiles in the Tonic Water Market - Industry players and strategies

The tonic water market features a diverse range of companies, from global beverage giants to specialized craft producers. The Coca-Cola Company, through its Schweppes brand, is a major player with extensive global reach and distribution capabilities. Britvic Plc, with its popular mixers portfolio, is another significant competitor, particularly strong in the European market. Fever-Tree Drinks Plc has emerged as a premium brand disruptor, focusing on high-quality, natural ingredients and unique flavor profiles, successfully capturing the growing demand for craft mixers. East Imperial Beverage Corp specializes in premium, small-batch tonic waters, targeting the high-end market segment. Fentimans Ltd offers a range of botanically brewed mixers, including tonic water, appealing to consumers seeking artisanal products. Q Tonic LLC focuses on all-natural, low-calorie tonic water, catering to health-conscious consumers. Thomas Henry GmbH, a European brand, has gained popularity for its wide range of mixers, including innovative tonic water flavors. These companies employ various strategies, including product innovation, premium positioning, sustainable sourcing, and strategic partnerships to differentiate themselves in the competitive market.

Porter's Five Forces Analysis of the Tonic Water Market - Competitive forces assessment

Applying Porter's Five Forces analysis to the tonic water market reveals the competitive dynamics shaping the industry. The threat of new entrants is moderate, as while the market offers opportunities for niche players, established brands have significant advantages in terms of distribution networks, brand recognition, and economies of scale. The bargaining power of suppliers is relatively low due to the availability of raw materials like quinine and carbonated water, although premium brands may seek specific botanical ingredients, slightly increasing supplier power in those cases. The bargaining power of buyers is moderate to high, particularly for on-trade customers who can easily switch between brands and demand consistent quality and competitive pricing. The threat of substitutes is moderate, with other mixers and soft drinks serving as alternatives, but tonic water's unique flavor profile and specific use in cocktails provide some protection. Competitive rivalry within the industry is intense, characterized by product differentiation strategies, marketing efforts, and price competition. The market's growth and premiumization trend have intensified competition, with both established players and craft producers vying for market share.

SWOT Analysis of the Tonic Water Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the tonic water market reveals key internal and external factors influencing its growth and development. Strengths of the market include the growing cocktail culture, which drives demand for premium mixers, and the versatility of tonic water as both a standalone beverage and a cocktail ingredient. The market benefits from product innovation, with companies introducing new flavors and low-calorie options to cater to diverse consumer preferences. However, weaknesses exist, such as the bitter taste of quinine, which may limit appeal to some consumers, and the high sugar content in traditional formulations, which conflicts with health trends. Opportunities in the market are significant, including expansion into emerging markets, development of sustainable and eco-friendly packaging, and leveraging e-commerce channels for direct-to-consumer sales. The market also has potential for growth in non-alcoholic cocktail alternatives. Threats to the market include intense competition from both established brands and new craft producers, potential regulatory changes regarding sugar content and labeling, and economic uncertainties that could impact consumer spending on premium beverages.

Tonic Water Market Value Chain Analysis - Industry structure and value flow

The tonic water market value chain encompasses several key stages, from raw material sourcing to end consumer delivery. The process begins with the procurement of essential ingredients, including quinine (derived from cinchona bark), carbonated water, sweeteners, and various botanical flavorings. These ingredients are then processed and mixed in manufacturing facilities, where quality control and consistency are crucial. The production stage involves carbonation, flavoring, and packaging, with companies increasingly focusing on sustainable packaging options. Distribution is a critical stage, with products moving through various channels including direct distribution to bars and restaurants (on-trade), wholesale distribution to retailers, and direct-to-consumer e-commerce platforms. Marketing and branding play a significant role in the value chain, particularly for premium and craft brands that emphasize unique flavor profiles and quality ingredients. The final stage involves retail and on-premise sales, where the product reaches consumers. Throughout the value chain, companies are increasingly focusing on sustainability, from responsible sourcing of ingredients to eco-friendly packaging and efficient distribution methods to reduce carbon footprint.

Key Investment Insights in the Tonic Water Market - Strategic investment recommendations

The tonic water market presents several attractive investment opportunities for both existing beverage companies and new entrants. Strategic investments should focus on product innovation, particularly in developing unique flavor profiles and botanical infusions to cater to evolving consumer tastes. There is significant potential in expanding low/no sugar and natural ingredient formulations to address health-conscious consumers. Investment in sustainable production and packaging technologies can provide a competitive edge, as environmental concerns become increasingly important to consumers. The premium and craft segments offer high-margin opportunities, with potential for creating niche brands that target specific consumer segments or geographic markets. E-commerce and direct-to-consumer channels represent a growing area for investment, particularly in light of changing consumer shopping behaviors. Emerging markets in Asia-Pacific and Latin America offer substantial growth potential, warranting investments in local production facilities and distribution networks. Strategic partnerships or acquisitions of innovative craft brands could provide quick access to new technologies, flavor expertise, and premium market segments. Additionally, investments in marketing and brand building, particularly around the cocktail culture and premium drinking experiences, can drive long-term growth and market share gains.

Tonic Water Market Conclusion - Summary and key takeaways

The tonic water market is a dynamic and growing segment of the global beverage industry, characterized by steady expansion and evolving consumer preferences. With a projected market size increase from $2.30 billion in 2026 to $3.68 billion by 2033, representing a CAGR of 6.91%, the market demonstrates robust growth potential. Key drivers include the premiumization trend, the enduring popularity of gin and tonic cocktails, and increasing demand for low-calorie and flavored options. The market is segmented by type (plain and flavored), category (low/no sugar and regular), and end user (on-trade and off-trade), each presenting unique opportunities for growth and innovation. While the COVID-19 pandemic temporarily impacted on-trade sales, the market has shown resilience through increased home consumption and e-commerce channels. The competitive landscape features a mix of global giants and craft producers, with premiumization and sustainability emerging as key differentiators. Regional analysis reveals varying growth rates, with emerging markets presenting significant opportunities for expansion. Overall, the tonic water market offers attractive prospects for investors and companies willing to innovate and adapt to changing consumer preferences.

Research Methodology - How this research was conducted

This market research report on the tonic water market was compiled using a comprehensive research methodology that combines both primary and secondary research techniques. Primary research involved interviews with industry experts, including executives from leading tonic water manufacturers, distributors, and retailers. These interviews provided valuable insights into market trends, competitive dynamics, and future growth prospects. Secondary research encompassed a thorough analysis of company annual reports, financial statements, press releases, and industry publications. Market data was gathered from reputable sources such as trade associations, government publications, and industry databases. The research team also conducted an extensive review of academic journals and market research reports to ensure a comprehensive understanding of the market. Data triangulation methods were employed to validate findings and ensure accuracy. The market size and growth projections were derived using both top-down and bottom-up approaches, considering factors such as historical growth rates, industry trends, and macroeconomic indicators. Regional analysis was conducted by examining local market conditions, consumer preferences, and economic factors in key geographic areas.

Research Scope - Coverage and limitations

This research report on the tonic water market provides a comprehensive analysis of the global market, covering key aspects such as market size, growth trends, competitive landscape, and regional dynamics. The scope of the research includes an examination of the market by type (plain and flavored), category (low/no sugar and regular), and end user (on-trade and off-trade). The report also provides detailed company profiles of major market players and analyzes the market using frameworks such as Porter's Five Forces and SWOT analysis. The research covers the period from 2025 to 2032, with specific focus on the market size in 2026 and the projected growth to 2033. The geographic scope encompasses major global regions, with particular attention to North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. While the report aims to provide a comprehensive overview, it is important to note that certain limitations exist. These include potential variations in data availability across different regions, the impact of unforeseen market disruptions, and the inherent challenges in accurately forecasting long-term market trends in a dynamic industry. The report focuses on commercial tonic water products and does not cover homemade or artisanal varieties outside of the mainstream market.

Key Companies and Recent Developments in the Tonic Water Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The tonic water market features several key players who are driving innovation and shaping the industry through strategic developments. Fever-Tree Drinks Plc continues to lead the premium segment with its focus on high-quality, natural ingredients. Recent developments include the launch of new flavored tonic waters and expansion into new geographic markets. The Coca-Cola Company, through its Schweppes brand, remains a dominant force in the market, leveraging its extensive distribution network. Recent initiatives include the introduction of low-calorie options and sustainable packaging solutions. Britvic Plc has strengthened its position in the European market through product innovation and marketing campaigns focused on the gin and tonic experience. East Imperial Beverage Corp has gained attention for its premium, small-batch tonic waters, with recent developments including collaborations with high-end bars and restaurants. Fentimans Ltd has expanded its botanical mixer range, introducing new tonic water flavors to cater to evolving consumer tastes. Q Tonic LLC has focused on the health-conscious segment, launching new low-calorie and naturally sweetened options. Thomas Henry GmbH has expanded its product line with innovative flavors and entered new European markets. These companies, along with others in the market, continue to drive growth through product innovation, sustainability initiatives, and strategic partnerships aimed at capturing emerging market opportunities.