Air Transport Used Serviceable Material Market Overview - Definition, scope, and significance

The Air Transport Used Serviceable Material (USM) Market represents a critical segment of the aviation aftermarket, encompassing the trade and utilization of pre-owned, certified serviceable components and materials for aircraft maintenance, repair, and overhaul (MRO) operations. This market serves as an economical alternative to purchasing new parts, offering significant cost savings for airlines, maintenance providers, and aircraft operators while maintaining stringent safety and quality standards. The scope includes various product categories such as engines, airframe components, and other aircraft systems, serving diverse aircraft types from narrowbody and widebody commercial aircraft to business jets and regional aircraft. The significance of this market lies in its ability to extend the lifecycle of aviation components, reduce operational costs, and provide critical support for aging aircraft fleets, thereby enhancing the overall sustainability and economic efficiency of the air transport industry.

Air Transport Used Serviceable Material Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Air Transport Used Serviceable Material Market is driven by several compelling factors, including the increasing demand for cost-effective maintenance solutions, the growing fleet of aging aircraft requiring replacement parts, and the rising focus on sustainable aviation practices through component reuse. Airlines' continuous pressure to reduce operational costs while maintaining safety standards has significantly boosted the adoption of USM. However, the market faces restraints such as stringent regulatory requirements for part certification, concerns about component reliability, and the limited availability of certain specialized parts. Challenges include managing the complex logistics of part sourcing and distribution, ensuring quality control across a global supply chain, and addressing potential security risks associated with used components. Opportunities abound in the expansion of digital platforms for USM trading, the development of advanced inspection and refurbishment technologies, and the growing aftermarket support for emerging aircraft types and regional markets.

Air Transport Used Serviceable Material Market Growth Trends - Current and emerging trends shaping the market

The Air Transport Used Serviceable Material Market is experiencing several notable growth trends that are reshaping the industry landscape. Digital transformation is a key trend, with the emergence of online marketplaces and blockchain-based platforms for USM trading, enhancing transparency and efficiency in the supply chain. There is a growing emphasis on sustainability, driving the adoption of USM as a means to reduce waste and carbon footprint in aviation. The market is also witnessing increased specialization, with providers focusing on specific aircraft types or component categories to offer more targeted solutions. Another significant trend is the rise of strategic partnerships between USM providers and airlines, enabling more integrated and cost-effective maintenance solutions. Additionally, advancements in part inspection and testing technologies are improving the reliability and acceptance of used serviceable materials, further driving market growth.

COVID-19 Impact on the Air Transport Used Serviceable Material Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the Air Transport Used Serviceable Material Market, mirroring the severe disruptions experienced across the entire aviation industry. The unprecedented decline in air travel led to a significant reduction in aircraft utilization, resulting in decreased demand for maintenance services and USM parts. Many airlines grounded large portions of their fleets, leading to a temporary oversupply of used serviceable materials in the market. However, the pandemic also accelerated certain trends, such as the increased focus on cost reduction and the adoption of digital solutions for remote inspections and transactions. As the industry recovers, the USM market is witnessing a resurgence driven by the need for cost-effective maintenance solutions as airlines seek to rebuild their operations. The recovery trajectory suggests a gradual return to pre-pandemic levels, with the market expected to benefit from the extended storage of aircraft during the pandemic, which has created a new supply of used serviceable materials.

Air Transport Used Serviceable Material Market Competitive Landscape - Major competitors and market consolidation

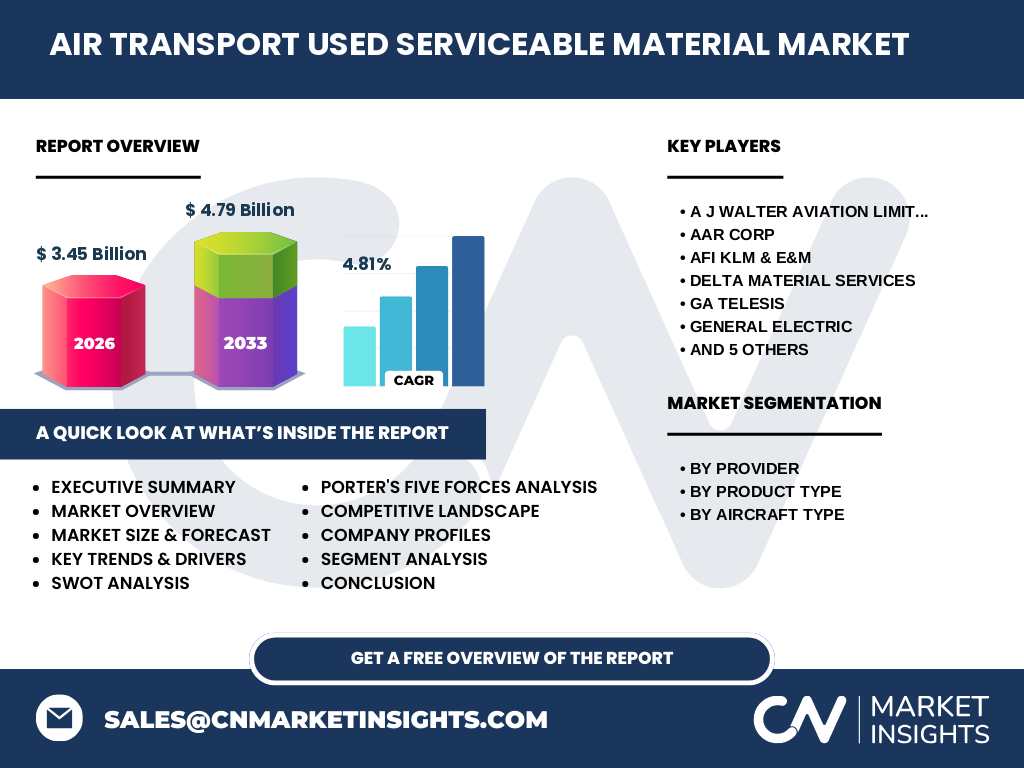

The Air Transport Used Serviceable Material Market features a competitive landscape characterized by a mix of large multinational corporations and specialized regional players. Key competitors include industry giants such as A J Walter Aviation Limited, AAR Corp, AFI KLM & E&M, Delta Material Services, GA Telesis, General Electric, Honeywell International Inc., Liebherr Group, Lufthansa Technik, and Pratt & Whitney. These companies compete on factors such as inventory breadth, quality assurance processes, global reach, and value-added services. The market is witnessing increased consolidation as larger players acquire specialized USM providers to expand their product offerings and geographic presence. Competition is also intensifying in terms of digital capabilities, with companies investing in advanced e-commerce platforms and data analytics to enhance customer experience and optimize inventory management. The competitive landscape is further shaped by the entry of new players offering innovative solutions, such as 3D printing of replacement parts and advanced material recycling technologies.

Executive Summary - High-level overview and key findings about Air Transport Used Serviceable Material Market

The Air Transport Used Serviceable Material Market is a dynamic and essential segment of the aviation aftermarket, offering significant cost savings and sustainability benefits to airlines and MRO providers. With a projected market size of $3.45 billion in 2026 and a forecasted growth to $4.79 billion by 2033, representing a CAGR of 4.81%, the market demonstrates robust potential for expansion. Key drivers include the increasing demand for cost-effective maintenance solutions, the growing fleet of aging aircraft, and the rising focus on sustainable aviation practices. The market is characterized by a diverse range of product types and aircraft segments, with narrowbody aircraft and engine components representing significant portions of the market. Despite challenges such as regulatory compliance and quality assurance, the industry is poised for growth, driven by technological advancements, digital transformation, and the recovery of the global aviation sector post-COVID-19. The competitive landscape features a mix of established players and innovative newcomers, all vying to capitalize on the market's growth potential through strategic partnerships, digital initiatives, and value-added services.

Air Transport Used Serviceable Material Market Forecast - Projections for 2025-2032 period

The Air Transport Used Serviceable Material Market is poised for steady growth over the 2025-2032 period, with projections indicating a market size of $3.45 billion in 2026 and an expected increase to $4.79 billion by 2033. This represents a compound annual growth rate (CAGR) of 4.81%, reflecting the market's resilience and potential for expansion. The forecast is underpinned by several factors, including the continued recovery of the global aviation industry, increasing aircraft fleet sizes, and the growing adoption of USM as a cost-effective maintenance strategy. The market is expected to benefit from the increasing number of aging aircraft requiring replacement parts, as well as the rising focus on sustainable aviation practices. Regional markets, particularly in Asia-Pacific and the Middle East, are anticipated to show strong growth due to expanding airline fleets and increasing MRO activities. The forecast also suggests a growing share for digital platforms and advanced inspection technologies in the USM supply chain, potentially reshaping market dynamics and creating new opportunities for both established players and innovative newcomers.

Air Transport Used Serviceable Material Market Size and Share by Segmentation - Breakdown by {segmentData}

The Air Transport Used Serviceable Material Market can be segmented by Provider, Product Type, and Aircraft Type, each contributing to the overall market dynamics. By Provider, the market is divided into OEM (Original Equipment Manufacturer) and Non-OEM segments. OEM providers, leveraging their brand reputation and technical expertise, typically command a significant market share, particularly in critical components and newer aircraft types. Non-OEM providers, including independent MRO companies and specialized USM traders, offer competitive alternatives, often focusing on older aircraft types and niche components. In terms of Product Type, the market is segmented into Engine, Component, and Airframe categories. Engine parts, due to their high value and critical nature, represent a substantial portion of the market. Component parts, including avionics and electrical systems, form another significant segment, while Airframe components cater to structural and exterior parts of aircraft. By Aircraft Type, the market serves Narrowbody Aircraft, Widebody Aircraft, Business Jets, and Regional Jets. Narrowbody aircraft, being the most numerous in commercial fleets, drive significant demand for USM, followed by widebody aircraft for long-haul operations. Business jets and regional aircraft segments, while smaller, present unique opportunities for specialized USM providers.

Global Air Transport Used Serviceable Material Market Size and Share by Region - Geographic distribution

The global Air Transport Used Serviceable Material Market exhibits distinct regional characteristics, with varying levels of market maturity and growth potential across different geographies. North America, led by the United States, represents a mature market with a significant share due to the presence of major airlines, MRO providers, and a large installed base of commercial aircraft. Europe follows closely, driven by strong aviation hubs in countries like Germany, France, and the UK, along with a robust network of USM providers and airlines. The Asia-Pacific region is emerging as a high-growth market, fueled by the rapid expansion of airline fleets in countries such as China, India, and Southeast Asian nations. This region is expected to witness the highest growth rate, driven by increasing air travel demand and the establishment of new MRO facilities. The Middle East, with its strategic location and growing airline industry, particularly in the UAE and Qatar, represents another significant market for USM. Latin America and Africa, while currently smaller markets, are showing potential for growth as their aviation sectors develop and modernize. The regional distribution of the market is influenced by factors such as fleet age, regulatory environment, economic conditions, and the presence of major aviation hubs and MRO facilities.

Regional Analysis of the Air Transport Used Serviceable Material Market - Detailed regional market performance

Regional analysis of the Air Transport Used Serviceable Material Market reveals diverse market dynamics and growth patterns across different geographies. In North America, the market is characterized by a high degree of maturity, with established players and a well-developed supply chain. The region benefits from a large installed base of commercial aircraft and a strong focus on cost optimization by airlines. Europe presents a similar picture of market maturity, with additional emphasis on sustainability and regulatory compliance driving USM adoption. The region's strong aviation manufacturing base and numerous MRO hubs contribute to a robust USM market. Asia-Pacific is emerging as the fastest-growing region, driven by rapid fleet expansion, increasing air travel demand, and the establishment of new MRO facilities. Countries like China and India are seeing significant investments in aviation infrastructure, creating new opportunities for USM providers. The Middle East region, led by the UAE and Qatar, is experiencing strong growth due to its strategic location as a global aviation hub and the presence of rapidly expanding airlines. Latin America and Africa, while currently smaller markets, are showing signs of growth as their aviation sectors develop, with increasing focus on fleet modernization and cost-effective maintenance solutions.

Leading Company Profiles in the Air Transport Used Serviceable Material Market - Industry players and strategies

The Air Transport Used Serviceable Material Market is dominated by several key players, each employing distinct strategies to maintain and expand their market positions. A J Walter Aviation Limited, known for its extensive inventory and global reach, focuses on providing comprehensive USM solutions across various aircraft types. AAR Corp leverages its broad service portfolio, including logistics and supply chain management, to offer integrated USM solutions. AFI KLM E&M, backed by the Air France-KLM group, combines its airline heritage with advanced MRO capabilities to serve a global customer base. Delta Material Services, a subsidiary of Delta Air Lines, benefits from direct access to a large fleet of aircraft, allowing for unique insights into part demand and lifecycle management. GA Telesis has positioned itself as a global distributor and provider of innovative USM solutions, with a strong emphasis on digital platforms. General Electric, through its aviation division, offers USM solutions backed by OEM expertise, particularly for GE-powered aircraft. Honeywell International Inc. leverages its broad aerospace portfolio to provide specialized USM for avionics and other critical systems. Liebherr Group focuses on high-quality USM for its proprietary systems, while Lufthansa Technik combines its MRO expertise with a strong USM offering. Pratt & Whitney, as an engine OEM, provides USM solutions with the backing of its engine technology and global service network.

Porter's Five Forces Analysis of the Air Transport Used Serviceable Material Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the Air Transport Used Serviceable Material Market. The threat of new entrants is moderate, as the market requires significant capital investment, established relationships with airlines, and compliance with stringent regulatory requirements. However, the potential for digital disruption and the entry of innovative startups focusing on niche segments remains. The bargaining power of buyers, primarily airlines and MRO providers, is significant due to the availability of multiple USM sources and the price-sensitive nature of the market. Suppliers, including part owners and refurbishers, have moderate bargaining power, influenced by the rarity of certain components and the complexity of the supply chain. The threat of substitutes, such as new parts or advanced repair techniques, is relatively low but growing, particularly with the development of additive manufacturing technologies. Competitive rivalry within the USM market is intense, characterized by price competition, service differentiation, and the struggle for market share among both established players and emerging competitors. The overall analysis suggests a market with moderate barriers to entry, significant buyer power, and intense competition, driving innovation and efficiency in USM provision.

SWOT Analysis of the Air Transport Used Serviceable Material Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Air Transport Used Serviceable Material Market reveals key internal and external factors influencing its growth and development. Strengths of the market include the significant cost savings offered to airlines, the ability to extend the lifecycle of aircraft components, and the growing acceptance of USM as a reliable maintenance solution. The market also benefits from a well-established global supply chain and the backing of major industry players. However, weaknesses exist in the form of potential quality concerns, the complexity of part traceability, and the dependency on aircraft retirements for part supply. Opportunities in the market are abundant, including the expansion into emerging aviation markets, the development of advanced inspection and refurbishment technologies, and the increasing focus on sustainable aviation practices. The market also stands to benefit from the growing trend of fleet modernization and the potential for digital transformation in USM trading. Threats to the market include stringent regulatory changes, the potential for new technologies to disrupt traditional USM models, and economic uncertainties that could impact airline spending on maintenance. Additionally, the market faces challenges from the cyclical nature of the aviation industry and the potential for geopolitical tensions to disrupt global supply chains.

Air Transport Used Serviceable Material Market Value Chain Analysis - Industry structure and value flow

The Air Transport Used Serviceable Material Market value chain encompasses a complex network of activities and stakeholders, each contributing to the flow of value from part acquisition to end-user delivery. The chain begins with part sourcing, which includes acquisitions from aircraft retirements, airline inventory reductions, and specialized part scavengers. This is followed by the inspection and certification phase, where parts undergo rigorous testing to ensure compliance with aviation standards. The refurbishment and repair stage involves the restoration of parts to serviceable condition, often requiring specialized skills and equipment. Inventory management and logistics form a critical component of the value chain, ensuring the availability and timely delivery of parts to customers. The distribution phase involves the sale of USM through various channels, including direct sales, online platforms, and partnerships with MRO providers. Value-added services, such as warranty offerings, technical support, and customized part kits, enhance the overall offering. At the end of the chain, the parts are utilized by airlines and MRO providers for aircraft maintenance and repair. Throughout this value chain, technology plays an increasingly important role, from digital marketplaces to advanced tracking systems, enhancing efficiency and transparency in the USM market.

Key Investment Insights in the Air Transport Used Serviceable Material Market - Strategic investment recommendations

Strategic investment in the Air Transport Used Serviceable Material Market offers numerous opportunities for growth and value creation. Key investment insights suggest focusing on digital transformation initiatives, including the development of advanced e-commerce platforms and blockchain-based traceability solutions, to enhance market efficiency and transparency. Investments in advanced inspection and testing technologies can improve part quality assurance and expand the range of serviceable components. The growing emphasis on sustainability presents opportunities for investments in recycling and refurbishment technologies, aligning with the aviation industry's environmental goals. Geographic expansion, particularly in high-growth regions such as Asia-Pacific and the Middle East, offers potential for market share growth. Strategic partnerships and acquisitions can provide access to new technologies, customer bases, and specialized market segments. Investments in data analytics and predictive maintenance capabilities can offer competitive advantages in inventory management and customer service. Additionally, focusing on niche segments, such as components for emerging aircraft types or specialized military applications, can provide targeted growth opportunities. Overall, successful investment strategies in the USM market should balance technological innovation, geographic expansion, and strategic partnerships to capitalize on the market's growth potential.

Air Transport Used Serviceable Material Market Conclusion - Summary and key takeaways

The Air Transport Used Serviceable Material Market represents a vital and growing segment of the aviation aftermarket, offering significant cost savings and sustainability benefits to airlines and MRO providers. With a projected market size of $3.45 billion in 2026 and a forecasted growth to $4.79 billion by 2033, representing a CAGR of 4.81%, the market demonstrates robust potential for expansion. Key drivers include the increasing demand for cost-effective maintenance solutions, the growing fleet of aging aircraft, and the rising focus on sustainable aviation practices. The market is characterized by a diverse range of product types and aircraft segments, with narrowbody aircraft and engine components representing significant portions of the market. Despite challenges such as regulatory compliance and quality assurance, the industry is poised for growth, driven by technological advancements, digital transformation, and the recovery of the global aviation sector post-COVID-19. The competitive landscape features a mix of established players and innovative newcomers, all vying to capitalize on the market's growth potential through strategic partnerships, digital initiatives, and value-added services. As the aviation industry continues to evolve, the USM market is expected to play an increasingly important role in supporting cost-effective and sustainable aircraft operations.

Research Methodology - How this research was conducted

The research methodology employed for this Air Transport Used Serviceable Material Market analysis combines both primary and secondary research approaches to ensure comprehensive and accurate insights. Primary research involved interviews with industry experts, including executives from leading USM providers, airline maintenance managers, and aviation consultants. These interviews provided valuable firsthand insights into market dynamics, challenges, and emerging trends. Secondary research encompassed a thorough review of industry reports, company annual reports, regulatory filings, and trade publications. Data from aviation industry associations and government sources were also analyzed to understand broader market trends and regulatory environments. The market size and forecast figures were derived using a combination of top-down and bottom-up approaches, considering factors such as fleet sizes, part replacement cycles, and regional market characteristics. The analysis also incorporated Porter's Five Forces framework and SWOT analysis to provide a strategic perspective on the market. Throughout the research process, data triangulation techniques were employed to validate findings and ensure the reliability of the conclusions presented in this report.

Research Scope - Coverage and limitations

The research scope for this Air Transport Used Serviceable Material Market analysis encompasses a comprehensive examination of the global market, focusing on key regions including North America, Europe, Asia-Pacific, the Middle East, Latin America, and Africa. The study covers various market segments based on provider type (OEM and Non-OEM), product type (Engine, Component, and Airframe), and aircraft type (Narrowbody Aircraft, Widebody Aircraft, Business Jets, and Regional Jets). The analysis includes an evaluation of market drivers, restraints, challenges, and opportunities, along with a detailed competitive landscape featuring leading companies in the industry. The research also provides market forecasts for the period 2025-2032, offering insights into future growth trends and potential investment opportunities. However, it is important to note certain limitations of this research. The analysis is primarily based on available public information and expert opinions, and may not capture all nuances of regional markets or emerging niche segments. Additionally, the rapidly evolving nature of the aviation industry and potential unforeseen global events could impact the accuracy of long-term forecasts. Despite these limitations, this research aims to provide a robust and insightful overview of the Air Transport Used Serviceable Material Market, serving as a valuable resource for industry stakeholders and decision-makers.

Key Companies and Recent Developments in the Air Transport Used Serviceable Material Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Air Transport Used Serviceable Material Market is characterized by the presence of several key players who have recently announced significant developments, partnerships, and strategic initiatives. A J Walter Aviation Limited has expanded its global footprint through strategic acquisitions, enhancing its inventory depth and geographic reach. The company has also invested in advanced e-commerce platforms to improve customer experience and streamline part sourcing. AAR Corp has announced a partnership with a leading digital logistics provider to optimize its supply chain operations and improve inventory management. AFI KLM E&M has launched a new sustainability initiative focused on extending the lifecycle of aircraft components through advanced refurbishment techniques. Delta Material Services, leveraging its airline heritage, has introduced a predictive maintenance program using AI to optimize part replacement cycles. GA Telesis has expanded its operations in the Asia-Pacific region, establishing new facilities to cater to the growing demand in emerging markets. General Electric has announced advancements in additive manufacturing for aircraft parts, potentially disrupting traditional USM supply chains. Honeywell International Inc. has launched a new line of reconditioned avionics components with enhanced performance and reliability. Liebherr Group has introduced a blockchain-based traceability system for its USM offerings, enhancing transparency and trust in the supply chain. Lufthansa Technik has formed a strategic alliance with a major airline to provide integrated USM and MRO solutions. Pratt & Whitney has announced a new warranty program for its used serviceable engine parts, aiming to boost customer confidence in USM adoption.