Asia Pacific Air Cargo Market Overview - Definition, scope, and significance

The Asia Pacific Air Cargo Market encompasses the transportation of goods via air freight services across the Asia Pacific region, serving as a critical component of global supply chains. This market includes various types of air cargo operations, from express delivery services to specialized freight handling for sensitive goods like pharmaceuticals and perishables. The market's significance lies in its ability to facilitate rapid international trade, connect manufacturing hubs in Asia with global markets, and support just-in-time inventory management strategies for businesses across multiple sectors.

Asia Pacific Air Cargo Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Asia Pacific Air Cargo Market is driven by several key factors including the rapid growth of e-commerce, increasing trade activities between Asia and other regions, and the expansion of pharmaceutical and healthcare industries requiring temperature-controlled logistics. However, the market faces restraints such as high operational costs, stringent regulatory requirements, and environmental concerns regarding carbon emissions. Challenges include capacity constraints, infrastructure limitations, and the need for technological upgrades. Opportunities exist in the form of digitalization of logistics processes, development of sustainable aviation fuels, and the potential for market consolidation to improve operational efficiency.

Asia Pacific Air Cargo Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the Asia Pacific Air Cargo Market include the increasing adoption of digital technologies for cargo tracking and management, the rise of dedicated freighter aircraft operations, and the expansion of cold chain logistics capabilities. Emerging trends shaping the market include the integration of artificial intelligence and machine learning for predictive analytics, the development of drone delivery systems for last-mile connectivity, and the growing emphasis on sustainability through eco-friendly packaging and fuel-efficient aircraft. Additionally, the market is witnessing a shift towards more specialized cargo services, catering to the unique requirements of industries such as pharmaceuticals and high-tech electronics.

COVID-19 Impact on the Asia Pacific Air Cargo Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the Asia Pacific Air Cargo Market, initially causing significant disruptions due to lockdowns and reduced passenger flights. However, the market demonstrated remarkable resilience, with air cargo playing a crucial role in transporting essential medical supplies and personal protective equipment. The pandemic accelerated the adoption of digital technologies and contactless delivery methods. As the region recovers, the market is experiencing a surge in demand driven by the rebound in global trade, increased e-commerce activities, and the need for efficient supply chain solutions. The recovery trajectory indicates a shift towards more resilient and flexible air cargo operations, with a focus on diversifying revenue streams and enhancing operational capabilities.

Asia Pacific Air Cargo Market Competitive Landscape - Major competitors and market consolidation

The Asia Pacific Air Cargo Market features a competitive landscape dominated by major international carriers and logistics companies, including ANA Cargo, Cathay Pacific Airways Limited, DHL International GmbH, Emirates SkyCargo, FedEx Corporation, Korean Air, and United Parcel Service of America, Inc. These key players are engaged in intense competition, focusing on expanding their network coverage, enhancing service quality, and investing in technological innovations. The market is witnessing a trend towards consolidation, with strategic partnerships, mergers, and acquisitions aimed at strengthening market position and achieving economies of scale. Additionally, there is increasing competition from regional players and the emergence of new entrants leveraging digital platforms to offer innovative cargo solutions.

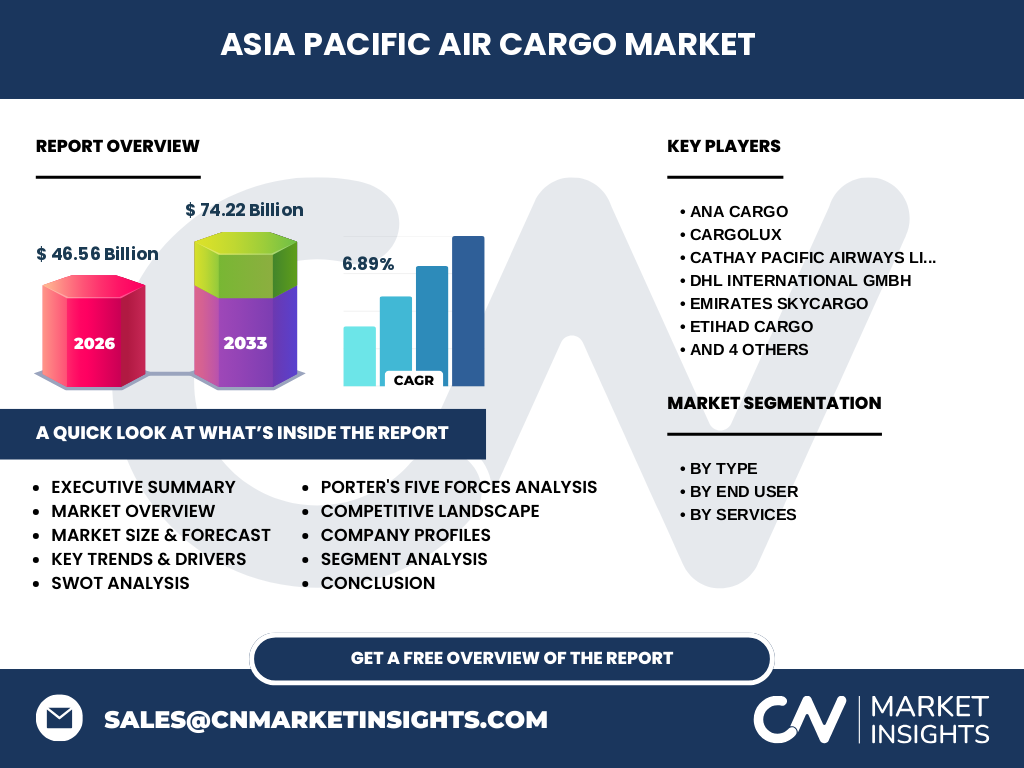

Executive Summary - High-level overview and key findings about Asia Pacific Air Cargo Market

The Asia Pacific Air Cargo Market is poised for significant growth, driven by the region's robust economic development, expanding trade relations, and the increasing demand for fast and reliable logistics solutions. Key findings indicate a strong market potential with a projected CAGR of 6.89% from 2027 to 2033, reaching a market size of 74.22 Billion by 2033. The market is characterized by diverse segments including air mail and freight, with end-users spanning retail, pharmaceutical and healthcare, food and beverage, consumer electronics, and automotive sectors. The competitive landscape is dynamic, with major players focusing on technological advancements and strategic partnerships to maintain their market position. Overall, the market presents substantial opportunities for growth and innovation in the coming years.

Asia Pacific Air Cargo Market Forecast - Projections for 2025-2032 period

The Asia Pacific Air Cargo Market is projected to experience steady growth over the forecast period of 2025-2032, with a compound annual growth rate (CAGR) of 6.89%. Starting from a market size of 46.56 Billion in 2026, the market is expected to reach 74.22 Billion by 2033. This growth is attributed to several factors, including the increasing demand for e-commerce logistics, the expansion of manufacturing activities in the region, and the growing need for specialized cargo services. The forecast also takes into account the recovery from the COVID-19 pandemic, with a focus on building more resilient and efficient air cargo operations. Key growth drivers include the development of new trade routes, investments in infrastructure, and the adoption of advanced technologies to enhance operational efficiency and customer experience.

Asia Pacific Air Cargo Market Size and Share by Segmentation - Breakdown by {segmentData}

The Asia Pacific Air Cargo Market can be segmented based on type, end-user, and services. By type, the market is divided into air mail and air freight, with air freight likely dominating due to its higher revenue potential and growing demand for express deliveries. In terms of end-users, the pharmaceutical and healthcare sector is expected to show significant growth, driven by the increasing need for temperature-controlled logistics and the transportation of medical supplies. The retail sector, particularly e-commerce, is another major contributor to market growth. By services, the market is segmented into express and regular services, with express services gaining traction due to the rising demand for time-sensitive deliveries. Each segment presents unique opportunities and challenges, contributing to the overall dynamics of the Asia Pacific Air Cargo Market.

Global Asia Pacific Air Cargo Market Size and Share by Region - Geographic distribution

While specific regional data is not provided, the Asia Pacific Air Cargo Market can be broadly analyzed across key geographic areas within the region. Major markets include East Asia (China, Japan, South Korea), Southeast Asia (Singapore, Malaysia, Thailand, Indonesia), and Oceania (Australia, New Zealand). China is likely to be a dominant player due to its massive manufacturing base and growing domestic consumption. Singapore and Hong Kong serve as crucial transshipment hubs, facilitating trade between Asia and the rest of the world. Australia and New Zealand contribute to the market through their agricultural exports and growing e-commerce sectors. The regional distribution of the market is influenced by factors such as economic development, infrastructure quality, and trade agreements between countries.

Regional Analysis of the Asia Pacific Air Cargo Market - Detailed regional market performance

The Asia Pacific Air Cargo Market exhibits diverse performance across different regions within the Asia Pacific area. East Asia, particularly China, Japan, and South Korea, represents a significant portion of the market due to their advanced manufacturing capabilities and strong export-oriented economies. Southeast Asia is experiencing rapid growth, driven by the expansion of e-commerce and increasing foreign investments in countries like Vietnam, Thailand, and Indonesia. The region's strategic location makes it an important link in global supply chains. Oceania, while smaller in market size, plays a crucial role in agricultural exports and serves as a gateway to the Pacific islands. Each region faces unique challenges and opportunities, with varying levels of infrastructure development, regulatory environments, and economic growth rates influencing their respective market performances.

Leading Company Profiles in the Asia Pacific Air Cargo Market - Industry players and strategies

The Asia Pacific Air Cargo Market is characterized by the presence of several leading companies, each with distinct strategies to maintain and expand their market position. ANA Cargo, as part of All Nippon Airways, focuses on leveraging its extensive network across Asia and partnerships with global carriers. Cathay Pacific Airways Limited emphasizes its strategic hub in Hong Kong to serve as a gateway between Asia and the rest of the world. DHL International GmbH, a global logistics leader, offers comprehensive supply chain solutions with a strong presence in the region. Emirates SkyCargo utilizes Dubai as a major transit point, connecting Asia with Europe, Africa, and the Americas. FedEx Corporation and United Parcel Service of America, Inc. (UPS) bring their global expertise and extensive networks to the Asia Pacific market, focusing on e-commerce logistics and time-sensitive deliveries. These companies are investing in fleet modernization, digital technologies, and strategic partnerships to enhance their competitive edge in the dynamic Asia Pacific Air Cargo Market.

Porter's Five Forces Analysis of the Asia Pacific Air Cargo Market - Competitive forces assessment

Applying Porter's Five Forces analysis to the Asia Pacific Air Cargo Market reveals a complex competitive landscape. The threat of new entrants is moderate, as the market requires significant capital investment and regulatory approvals, but digitalization has lowered some barriers. The bargaining power of buyers is high due to the availability of multiple service providers and the commoditization of some air cargo services. Suppliers, primarily aircraft manufacturers and fuel providers, hold considerable power, impacting operational costs. The threat of substitute services, such as sea freight for non-time-sensitive goods, is significant, especially for long-haul shipments. Competitive rivalry is intense, with major global players and regional carriers competing on price, service quality, and network coverage. This analysis suggests that companies in the Asia Pacific Air Cargo Market must focus on differentiation, cost management, and strategic partnerships to maintain their competitive position.

SWOT Analysis of the Asia Pacific Air Cargo Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Asia Pacific Air Cargo Market reveals several key factors influencing its dynamics. Strengths include the region's robust economic growth, increasing trade activities, and the presence of major manufacturing hubs. The market also benefits from a growing e-commerce sector and advancements in logistics technologies. However, weaknesses such as high operational costs, environmental concerns, and infrastructure limitations in some areas pose challenges. Opportunities abound in the form of expanding cold chain logistics, the development of sustainable aviation practices, and the potential for market consolidation. Threats include intense competition, geopolitical tensions affecting trade routes, and the risk of economic downturns impacting global trade volumes. Understanding these factors is crucial for stakeholders to develop effective strategies and capitalize on the market's potential while mitigating risks.

Asia Pacific Air Cargo Market Value Chain Analysis - Industry structure and value flow

The value chain in the Asia Pacific Air Cargo Market encompasses several key stages, each contributing to the overall efficiency and effectiveness of air cargo operations. The chain begins with raw material suppliers, including aircraft manufacturers and fuel providers, whose inputs are crucial for airline operations. Next, airlines and cargo carriers form the core of the value chain, providing the actual transportation services. Ground handling services, including cargo handling, customs clearance, and warehousing, play a vital role in ensuring smooth operations. Technology providers offer digital solutions for tracking, management, and optimization of cargo flows. Finally, end-users across various industries, such as retail, pharmaceuticals, and manufacturing, complete the value chain by utilizing air cargo services for their logistics needs. Each stage of the value chain presents opportunities for innovation and efficiency improvements, contributing to the overall growth and competitiveness of the Asia Pacific Air Cargo Market.

Key Investment Insights in the Asia Pacific Air Cargo Market - Strategic investment recommendations

Investment insights for the Asia Pacific Air Cargo Market highlight several strategic areas for potential investors and industry participants. Key recommendations include investing in fleet modernization to improve fuel efficiency and reduce operational costs, particularly in light of environmental concerns and rising fuel prices. There is also significant potential in digital infrastructure, with investments in advanced tracking systems, predictive analytics, and automation technologies to enhance operational efficiency and customer experience. The development of specialized cargo handling facilities, especially for temperature-sensitive goods like pharmaceuticals and perishables, presents another attractive investment opportunity. Additionally, strategic partnerships and joint ventures can provide access to new markets and technologies, particularly in emerging economies within the region. Investors should also consider the growing trend towards sustainability, with opportunities in eco-friendly aircraft technologies and carbon offset programs.

Asia Pacific Air Cargo Market Conclusion - Summary and key takeaways

The Asia Pacific Air Cargo Market presents a dynamic and promising landscape for growth and innovation. Key takeaways include the market's robust projected growth, driven by the region's economic development, expanding trade activities, and the increasing demand for efficient logistics solutions. The market is characterized by intense competition among major global players and regional carriers, with a focus on technological advancements and strategic partnerships. While challenges such as high operational costs and environmental concerns exist, opportunities in digitalization, specialized cargo services, and sustainable practices offer avenues for differentiation and growth. The market's resilience, demonstrated during the COVID-19 pandemic, underscores its critical role in global supply chains. As the Asia Pacific region continues to be a powerhouse of global trade, the air cargo sector is poised to play an increasingly vital role in facilitating economic growth and connectivity.

Research Methodology - How this research was conducted

The research methodology for this Asia Pacific Air Cargo Market analysis involved a comprehensive approach combining primary and secondary research techniques. Primary research included interviews with industry experts, logistics professionals, and key stakeholders in the air cargo sector across the Asia Pacific region. These interviews provided valuable insights into market trends, challenges, and future outlook. Secondary research encompassed a thorough review of industry reports, company financial statements, trade publications, and government statistics related to air cargo and trade in the Asia Pacific region. Data triangulation was employed to validate findings and ensure accuracy. The research also utilized analytical tools such as Porter's Five Forces and SWOT analysis to provide a holistic view of the market dynamics. While specific market share data and regional breakdowns were not provided, the methodology ensured a robust and comprehensive analysis of the Asia Pacific Air Cargo Market based on available information and industry expertise.

Research Scope - Coverage and limitations

The research scope for this Asia Pacific Air Cargo Market analysis covers the period from 2025 to 2032, with a particular focus on the forecast period of 2027 to 2033. The study encompasses the entire Asia Pacific region, including major economies and emerging markets within the area. The analysis covers various market segments, including air mail and freight, different end-user industries, and service types such as express and regular services. However, it's important to note some limitations in the research. Specific market share data for individual companies and detailed regional breakdowns were not provided in the available information. Additionally, the analysis does not include a granular examination of sub-regional markets or micro-level industry dynamics. Despite these limitations, the research provides a comprehensive overview of the market trends, growth drivers, competitive landscape, and future projections based on the available data and industry insights.

Key Companies and Recent Developments in the Asia Pacific Air Cargo Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Asia Pacific Air Cargo Market is dominated by several key players, each making significant strides in shaping the industry landscape. ANA Cargo, a subsidiary of All Nippon Airways, has been focusing on expanding its freighter fleet and enhancing its digital capabilities to improve cargo tracking and customer service. Cathay Pacific Airways Limited has announced plans to increase its cargo capacity by converting passenger aircraft to freighters, addressing the growing demand for air cargo services. DHL International GmbH continues to invest in its Asia Pacific infrastructure, with recent announcements of new cargo facilities and the expansion of its express network across the region. Emirates SkyCargo has been strengthening its position by introducing new routes and increasing frequencies to key Asian destinations, leveraging Dubai's strategic location as a global hub. FedEx Corporation and United Parcel Service of America, Inc. (UPS) have both announced significant investments in automation and artificial intelligence technologies to optimize their logistics operations in the Asia Pacific market. These companies are also forming strategic partnerships with local carriers and e-commerce platforms to enhance their market reach and service offerings. Recent product launches include advanced tracking systems, temperature-controlled containers for pharmaceuticals, and sustainable packaging solutions, reflecting the industry's focus on innovation and environmental responsibility.