Europe Semiconductor Manufacturing Equipment Market Overview - Definition, scope, and significance

The Europe Semiconductor Manufacturing Equipment Market encompasses the production, distribution, and application of specialized machinery and tools used in the fabrication of semiconductor devices. This market includes equipment for wafer manufacturing, assembly and packaging, and testing processes that are essential for producing integrated circuits, microchips, and other semiconductor components. The significance of this market lies in its critical role as the backbone of Europe's semiconductor industry, enabling the continent to maintain technological sovereignty and compete in the global electronics supply chain. As Europe seeks to reduce its dependency on Asian semiconductor manufacturing, the development and deployment of advanced semiconductor manufacturing equipment has become a strategic priority for ensuring the region's technological competitiveness and economic security.

Europe Semiconductor Manufacturing Equipment Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the Europe Semiconductor Manufacturing Equipment Market include the increasing demand for advanced electronics across automotive, industrial, and consumer applications, coupled with government initiatives to strengthen domestic semiconductor capabilities. The European Union's CHIPS Act and related funding programs have created substantial momentum for local semiconductor manufacturing capacity. However, the market faces significant restraints including high capital investment requirements, complex supply chain dependencies, and intense global competition from established Asian manufacturers. Key challenges include the shortage of skilled workforce, the need for continuous technological innovation to keep pace with Moore's Law, and the geopolitical tensions affecting semiconductor trade. Opportunities exist in the growing demand for automotive semiconductors, the expansion of 5G infrastructure, and the emergence of new applications in artificial intelligence and edge computing that require specialized semiconductor manufacturing capabilities.

Europe Semiconductor Manufacturing Equipment Market Growth Trends - Current and emerging trends shaping the market

The Europe Semiconductor Manufacturing Equipment Market is experiencing several transformative growth trends. Advanced packaging technologies, particularly 2.5D and 3D integration, are gaining prominence as manufacturers seek to overcome the limitations of traditional scaling. There is a notable shift toward equipment that supports heterogeneous integration and chiplet architectures, enabling more flexible and efficient semiconductor designs. The market is also witnessing increased adoption of artificial intelligence and machine learning in manufacturing processes, leading to smarter, more automated production lines. Sustainability has emerged as a critical trend, with manufacturers focusing on energy-efficient equipment and processes to reduce the environmental impact of semiconductor production. Additionally, the trend toward regionalization of semiconductor supply chains is creating new opportunities for European equipment manufacturers to establish themselves as reliable local suppliers to the growing network of European fabs.

COVID-19 Impact on the Europe Semiconductor Manufacturing Equipment Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the Europe Semiconductor Manufacturing Equipment Market through supply chain interruptions, factory closures, and reduced capital expenditure as companies prioritized short-term survival over long-term investments. However, the pandemic also exposed the vulnerabilities of global semiconductor supply chains, particularly Europe's heavy reliance on Asian manufacturing, which paradoxically accelerated government and industry initiatives to strengthen local semiconductor capabilities. The recovery trajectory has been characterized by a surge in demand for semiconductor equipment as companies raced to expand capacity and reduce future supply chain risks. The pandemic fundamentally shifted the strategic importance of semiconductor manufacturing equipment, with governments recognizing it as critical infrastructure. This recognition has translated into unprecedented levels of public funding and policy support, creating a more favorable environment for market recovery and sustained growth beyond pre-pandemic levels.

Europe Semiconductor Manufacturing Equipment Market Competitive Landscape - Major competitors and market consolidation

The competitive landscape of the Europe Semiconductor Manufacturing Equipment Market is characterized by a mix of global technology leaders and specialized regional players. ASML Holding N.V. dominates the lithography equipment segment, maintaining a near-monopoly position in advanced EUV technology. Other major international competitors include Applied Materials, Lam Research, and Tokyo Electron, which compete across various equipment segments. The European market also features specialized local companies that focus on niche technologies and integrated solutions. Market consolidation has been ongoing, with larger players acquiring smaller innovative companies to expand their technology portfolios and market reach. The competitive dynamics are further shaped by strategic partnerships between equipment manufacturers, semiconductor companies, and research institutions to develop next-generation manufacturing technologies. This collaborative approach is particularly evident in Europe, where public-private partnerships play a crucial role in advancing semiconductor manufacturing capabilities.

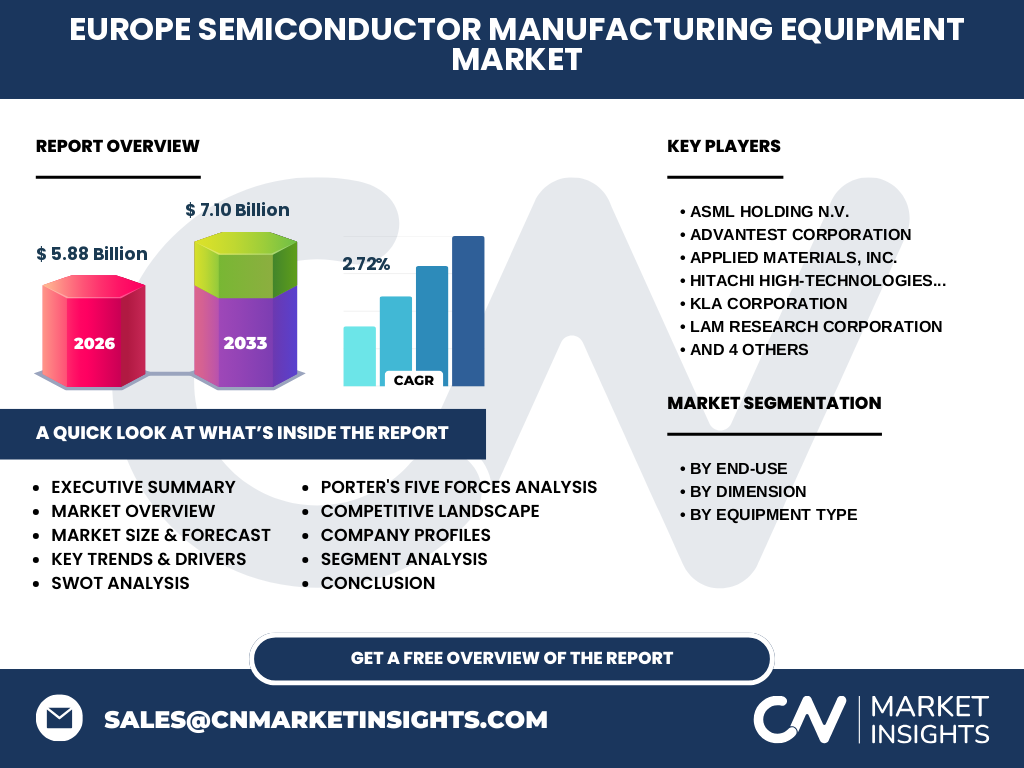

Executive Summary - High-level overview and key findings about Europe Semiconductor Manufacturing Equipment Market

The Europe Semiconductor Manufacturing Equipment Market is at a critical inflection point, driven by unprecedented government support, technological innovation, and the strategic imperative to achieve semiconductor sovereignty. The market, valued at 5.88 Billion in 2026, is projected to grow to 7.10 Billion by 2033, representing a steady CAGR of 2.72%. This growth is underpinned by the European Union's ambitious semiconductor strategy, which includes substantial funding for domestic manufacturing capacity and technology development. The market is characterized by increasing demand for advanced equipment supporting 2.5D and 3D integration technologies, as well as a growing emphasis on sustainability and automation. While challenges remain in terms of global competition and supply chain dependencies, the strategic importance of semiconductor manufacturing equipment has never been higher, positioning the European market for sustained growth and technological advancement in the coming years.

Europe Semiconductor Manufacturing Equipment Market Forecast - Projections for 2025-2032 period

The Europe Semiconductor Manufacturing Equipment Market is projected to experience steady growth from 2025 to 2032, with the market size expanding from 5.88 Billion in 2026 to 7.10 Billion by 2033. This represents a compound annual growth rate of 2.72%, reflecting the market's resilience and the strong foundation provided by European government initiatives and industry investments. The forecast period will be characterized by increasing demand for advanced manufacturing equipment, particularly for next-generation semiconductor nodes and advanced packaging solutions. The growth trajectory will be influenced by the successful implementation of the European Chips Act, the establishment of new semiconductor fabs across the continent, and the continuous technological evolution toward smaller process nodes and more complex 3D architectures. Regional market dynamics will vary, with Western European countries leading in equipment deployment while Eastern European nations emerge as potential growth markets for semiconductor manufacturing capabilities.

Europe Semiconductor Manufacturing Equipment Market Size and Share by Segmentation - Breakdown by {segmentData}

The Europe Semiconductor Manufacturing Equipment Market segmentation reveals distinct patterns across different categories. By end-use, Semiconductor Fabrication Plants/Foundries represent the largest segment, driven by the establishment of new manufacturing facilities and the expansion of existing ones. Semiconductor Electronics Manufacturing follows as a significant segment, supported by the growing demand for consumer electronics and automotive semiconductors. The Test Home segment, while smaller, is experiencing growth due to the increasing complexity of semiconductor devices requiring sophisticated testing solutions. By dimension, 2D equipment currently dominates the market, but 2.5D and 3D equipment segments are growing rapidly as manufacturers adopt advanced packaging technologies. In terms of equipment type, Wafer Manufacturing Equipment holds the largest market share, reflecting the fundamental importance of wafer processing in semiconductor fabrication. Assembly & Packaging Equipment and Test Equipment segments are also substantial, with increasing demand for advanced packaging solutions driving growth in the assembly and packaging category.

Global Europe Semiconductor Manufacturing Equipment Market Size and Share by Region - Geographic distribution

The geographic distribution of the Europe Semiconductor Manufacturing Equipment Market shows distinct regional characteristics across the continent. Western European countries, particularly Germany, the Netherlands, and France, dominate the market due to their established semiconductor ecosystems, advanced technological capabilities, and significant investments in research and development. The Netherlands, home to ASML, holds a particularly strong position in lithography equipment manufacturing. Southern European countries like Italy and Spain are emerging as important markets, supported by government initiatives and growing electronics manufacturing sectors. Eastern European nations, while currently smaller markets, are showing promising growth potential due to lower operational costs and increasing foreign direct investment in semiconductor manufacturing. The Nordic countries contribute significantly to the market through their expertise in materials science and equipment innovation. Overall, the regional distribution reflects Europe's diverse industrial landscape and the varying levels of semiconductor manufacturing maturity across different countries.

Regional Analysis of the Europe Semiconductor Manufacturing Equipment Market - Detailed regional market performance

Regional analysis of the Europe Semiconductor Manufacturing Equipment Market reveals diverse performance patterns across different areas. Germany leads the regional market, driven by its strong automotive industry's demand for semiconductors and its established electronics manufacturing base. The country's focus on Industry 4.0 and smart manufacturing has created substantial demand for advanced semiconductor equipment. The Netherlands, with ASML's headquarters, represents a critical region for lithography equipment manufacturing and export. France has emerged as a significant market due to government support for semiconductor research and the presence of major electronics companies. Southern Europe, particularly Italy and Spain, shows growing potential with increasing investments in semiconductor manufacturing capabilities and supportive government policies. Eastern European countries like Poland and the Czech Republic are developing their semiconductor equipment markets, attracted by lower costs and strategic location advantages. The UK, despite Brexit challenges, maintains a strong position in semiconductor design and testing equipment. Each region's performance is influenced by local industrial strengths, government policies, and integration with global supply chains.

Leading Company Profiles in the Europe Semiconductor Manufacturing Equipment Market - Industry players and strategies

The Europe Semiconductor Manufacturing Equipment Market features several leading companies with distinct strategic approaches. ASML Holding N.V. stands as the dominant player, particularly in lithography equipment, with its EUV technology being critical for advanced semiconductor manufacturing. The company's strategy focuses on continuous innovation and maintaining technological leadership through substantial R&D investments. Applied Materials, while headquartered in the US, maintains significant operations in Europe and focuses on integrated solutions across the semiconductor manufacturing process. Lam Research Corporation specializes in deposition and etching equipment, with a strategy centered on advanced node manufacturing. KLA Corporation leads in process control and yield management solutions, emphasizing data analytics and AI integration in its equipment. Advantest Corporation dominates the semiconductor testing segment, with a strategy focused on addressing the growing complexity of semiconductor devices. These companies are increasingly pursuing strategies of vertical integration, strategic partnerships, and localization of manufacturing to strengthen their positions in the European market.

Porter's Five Forces Analysis of the Europe Semiconductor Manufacturing Equipment Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the Europe Semiconductor Manufacturing Equipment Market. The threat of new entrants is relatively low due to the high capital requirements, complex technology, and established relationships between equipment manufacturers and semiconductor companies. However, the strategic importance of semiconductor manufacturing is encouraging some new players to enter niche segments. The bargaining power of buyers, primarily semiconductor manufacturers, is significant given the concentration of the semiconductor industry and the large volumes of equipment purchased. Suppliers of critical components and materials wield considerable power, particularly for specialized parts essential to advanced equipment. The threat of substitute products is low, as semiconductor manufacturing requires highly specialized equipment with no viable alternatives. Competitive rivalry is intense among the major players, characterized by rapid technological innovation, price competition, and the pursuit of comprehensive solution offerings. The overall analysis suggests a market with high barriers to entry but significant opportunities for established players who can innovate and adapt to changing customer needs.

SWOT Analysis of the Europe Semiconductor Manufacturing Equipment Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Europe Semiconductor Manufacturing Equipment Market reveals significant insights into its strategic position. Strengths include Europe's strong research and development capabilities, particularly in materials science and equipment innovation, supported by world-class universities and research institutions. The region benefits from substantial government support through initiatives like the European Chips Act, providing financial backing and policy framework for growth. Europe's diverse industrial base creates demand across multiple semiconductor application areas, from automotive to industrial automation. However, weaknesses exist in the form of fragmented markets across different countries, creating challenges for economies of scale, and a shortage of skilled workforce specialized in advanced semiconductor manufacturing. Opportunities are abundant in the growing demand for automotive semiconductors, the expansion of 5G infrastructure, and the potential for Europe to establish itself as a leader in sustainable semiconductor manufacturing practices. Threats include intense global competition, particularly from Asian manufacturers with established supply chains, and the risk of technological dependence on non-European companies for critical equipment components.

Europe Semiconductor Manufacturing Equipment Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the Europe Semiconductor Manufacturing Equipment Market reveals a complex ecosystem of interconnected activities and stakeholders. At the foundation of the value chain are raw material suppliers providing specialized components, chemicals, and materials essential for equipment manufacturing. Equipment manufacturers then integrate these components into sophisticated machinery, incorporating advanced technologies such as precision mechanics, optics, and software control systems. Semiconductor manufacturers represent the primary customers, utilizing this equipment to produce integrated circuits and other semiconductor devices. The value chain also includes research institutions and universities that drive innovation through fundamental research and technology development. Service providers play a crucial role in maintaining and optimizing equipment performance throughout its lifecycle. The flow of value is characterized by high capital intensity, long development cycles, and the critical importance of technological innovation at each stage. The European value chain is distinguished by its emphasis on sustainability and the integration of digital technologies for enhanced manufacturing efficiency.

Key Investment Insights in the Europe Semiconductor Manufacturing Equipment Market - Strategic investment recommendations

Investment insights for the Europe Semiconductor Manufacturing Equipment Market point to several strategic opportunities for stakeholders. The most compelling investment area is in advanced packaging equipment supporting 2.5D and 3D integration technologies, as these represent the future of semiconductor scaling beyond traditional Moore's Law limitations. Investments in automation and artificial intelligence-enabled manufacturing equipment are particularly attractive, given the industry's push toward smarter, more efficient production processes. The growing emphasis on sustainability presents investment opportunities in energy-efficient equipment and processes that reduce the environmental impact of semiconductor manufacturing. Regional manufacturing capabilities represent another strategic investment area, as companies seek to reduce supply chain dependencies and establish local production facilities. Additionally, investments in workforce development and training programs are crucial to address the skills gap in advanced semiconductor manufacturing. For equipment manufacturers, strategic partnerships with semiconductor companies and research institutions offer pathways to innovation and market access, while investments in digital platforms for equipment monitoring and predictive maintenance are becoming increasingly important.

Europe Semiconductor Manufacturing Equipment Market Conclusion - Summary and key takeaways

The Europe Semiconductor Manufacturing Equipment Market stands at a pivotal juncture, characterized by strong government support, technological innovation, and strategic importance for regional economic security. With a projected growth from 5.88 Billion in 2026 to 7.10 Billion by 2033 at a CAGR of 2.72%, the market demonstrates steady and sustainable growth potential. The European Union's semiconductor strategy, coupled with increasing demand for advanced electronics across automotive, industrial, and consumer applications, provides a robust foundation for market expansion. While challenges exist in terms of global competition and supply chain dependencies, the strategic imperative to achieve semiconductor sovereignty has elevated the importance of domestic equipment manufacturing capabilities. The market's future will be shaped by advancements in advanced packaging technologies, the integration of artificial intelligence in manufacturing processes, and the growing emphasis on sustainability. Success in this market will require continuous innovation, strategic partnerships, and alignment with the broader goals of European technological sovereignty and economic competitiveness.

Research Methodology - How this research was conducted

The research methodology for this Europe Semiconductor Manufacturing Equipment Market analysis employed a comprehensive and multi-faceted approach to ensure accuracy and reliability. Primary research formed the foundation, involving interviews with key industry stakeholders including equipment manufacturers, semiconductor companies, industry experts, and government officials involved in semiconductor policy. These interviews provided valuable insights into market dynamics, technological trends, and strategic developments. Secondary research complemented the primary data through extensive review of industry reports, company financial statements, patent filings, technical publications, and government policy documents. Market size and forecast calculations were derived using both top-down and bottom-up approaches, triangulating data from multiple sources to ensure robustness. The segmentation analysis was based on detailed examination of equipment types, end-use applications, and dimensional technologies, supported by industry classification standards. Regional analysis incorporated economic indicators, industrial development data, and investment patterns across different European countries. The methodology also included competitive analysis through examination of company strategies, product portfolios, and market positioning, ensuring a comprehensive understanding of the competitive landscape.

Research Scope - Coverage and limitations

The research scope for this Europe Semiconductor Manufacturing Equipment Market analysis encompasses the comprehensive examination of equipment used in semiconductor fabrication, assembly, packaging, and testing across the European continent. The study covers the period from 2025 to 2032, with historical data and future projections providing context for market trends and growth trajectories. The analysis includes all major equipment categories: wafer manufacturing equipment, assembly and packaging equipment, and test equipment, examining their respective market sizes, growth rates, and technological developments. Geographic coverage extends across all European regions, with detailed analysis of Western, Southern, and Eastern European markets, recognizing the diverse industrial landscapes and development stages across the continent. The research also encompasses various semiconductor applications including consumer electronics, automotive, industrial, and telecommunications sectors. Limitations of the study include the rapid pace of technological change in the semiconductor industry, which may affect long-term projections, and the potential impact of unforeseen geopolitical events on market dynamics. Additionally, the analysis focuses on equipment manufacturing and does not extensively cover the broader semiconductor supply chain or end-market applications beyond their influence on equipment demand.

Key Companies and Recent Developments in the Europe Semiconductor Manufacturing Equipment Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Europe Semiconductor Manufacturing Equipment Market features several key companies driving innovation and market growth through strategic developments. ASML Holding N.V. continues to dominate with its EUV lithography technology, recently announcing advancements in high-numerical aperture EUV systems that promise to extend semiconductor scaling capabilities. The company has also strengthened its partnerships with European research institutions to develop next-generation lithography solutions. Applied Materials, Inc. has launched new dielectric deposition and etching systems optimized for advanced packaging applications, supporting the industry's transition to 2.5D and 3D integration. Lam Research Corporation recently introduced AI-enabled process control systems that enhance yield and productivity in advanced node manufacturing. KLA Corporation has expanded its portfolio of inspection and metrology equipment with solutions specifically designed for heterogeneous integration and advanced packaging. Advantest Corporation announced new testing solutions for automotive semiconductors, addressing the growing demand for high-reliability testing in the automotive sector. These companies, along with other major players like Tokyo Electron and Rudolph Technologies, are actively pursuing strategic partnerships, research collaborations, and product innovations to strengthen their positions in the European market and address the evolving needs of semiconductor manufacturers.