Europe Fourth Party Logistics Market Overview - Definition, scope, and significance

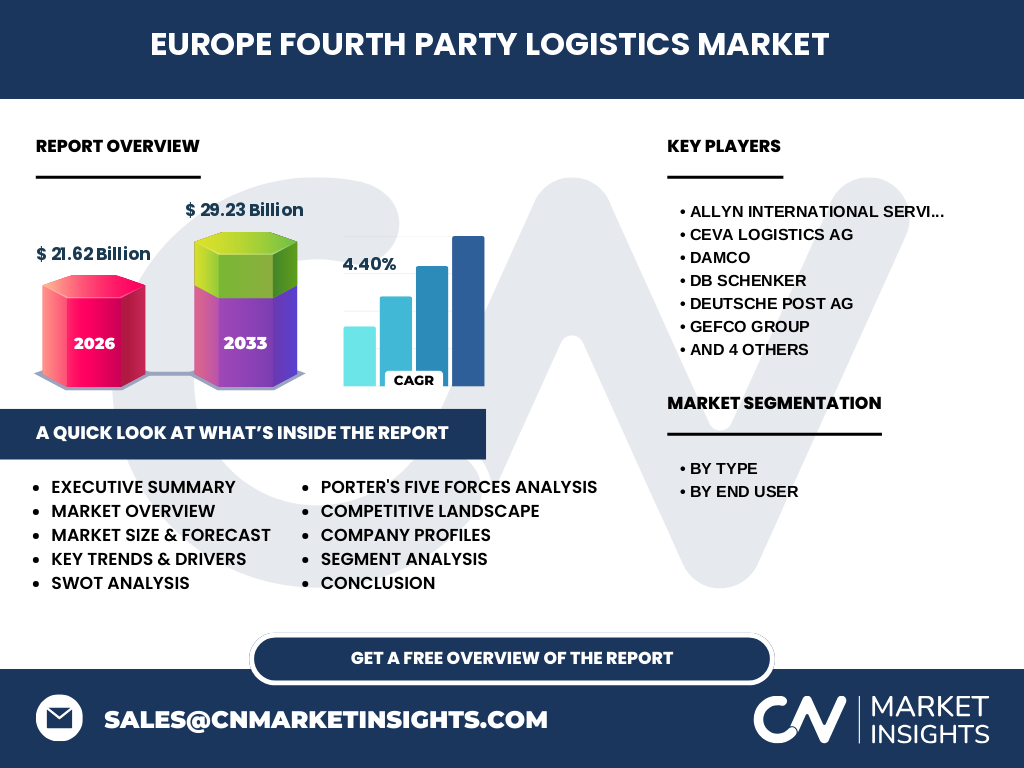

Fourth Party Logistics (4PL) represents a sophisticated outsourcing model where a single partner manages an entire supply chain by integrating, organizing, and overseeing multiple logistics service providers. Unlike traditional logistics providers, 4PL operators function as neutral intermediaries who design, build, and provide operational management of comprehensive supply chain solutions. In the European context, 4PL services encompass end-to-end supply chain management, including procurement, transportation, warehousing, distribution, and value-added services. The European 4PL market has gained significant traction due to increasing globalization, complex supply chain requirements, and the need for cost optimization. The market's significance is underscored by its projected growth from 21.62 billion in 2026 to 29.23 billion by 2033, reflecting a CAGR of 4.40%. This growth trajectory demonstrates the critical role 4PL services play in enabling European businesses to maintain competitive advantage through enhanced supply chain efficiency and flexibility.

Europe Fourth Party Logistics Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Europe Fourth Party Logistics market is primarily driven by the increasing complexity of supply chains, rising e-commerce penetration, and the need for cost optimization. Companies are seeking comprehensive logistics solutions that can provide end-to-end visibility and control, driving demand for 4PL services. The market is also benefiting from technological advancements, including IoT, AI, and blockchain, which enable better supply chain management and optimization. However, the market faces several restraints, including high implementation costs, resistance to change from traditional logistics models, and data security concerns. Key challenges include the need for skilled professionals, integration complexities with existing systems, and maintaining service quality across multiple partners. Despite these challenges, significant opportunities exist in emerging sectors such as healthcare and consumer electronics, as well as in the development of sustainable logistics solutions. The market is also seeing opportunities in digital transformation initiatives and the growing demand for customized logistics solutions.

Europe Fourth Party Logistics Market Growth Trends - Current and emerging trends shaping the market

The Europe Fourth Party Logistics market is experiencing several transformative trends that are reshaping the industry landscape. Digital transformation remains a key driver, with 4PL providers increasingly adopting advanced technologies such as artificial intelligence, machine learning, and blockchain to enhance supply chain visibility and efficiency. The market is also witnessing a growing emphasis on sustainability, with companies seeking eco-friendly logistics solutions to meet environmental regulations and consumer expectations. Another significant trend is the rise of omnichannel logistics, particularly driven by the e-commerce boom, requiring 4PL providers to offer integrated solutions across multiple sales channels. The market is also seeing increased adoption of cloud-based platforms for better supply chain management and real-time tracking capabilities. Additionally, there is a growing focus on risk management and resilience in supply chains, leading to increased demand for 4PL services that can provide comprehensive risk mitigation strategies and alternative sourcing options.

COVID-19 Impact on the Europe Fourth Party Logistics Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has significantly impacted the Europe Fourth Party Logistics market, initially causing disruptions in supply chains and logistics operations across the region. The pandemic exposed vulnerabilities in traditional supply chain models, leading to increased demand for more resilient and flexible logistics solutions. 4PL providers played a crucial role in helping businesses navigate these challenges by offering alternative routing options, managing inventory more effectively, and ensuring continuity of supply. The crisis accelerated the adoption of digital technologies and automation in logistics operations, as companies sought to enhance their supply chain visibility and control. As the market recovers, there is a growing emphasis on building more robust and adaptable supply chain networks. The pandemic has also highlighted the importance of regional supply chains, leading to increased demand for 4PL services that can provide localized solutions while maintaining global connectivity. This shift in market dynamics is expected to drive sustained growth in the 4PL sector as businesses prioritize supply chain resilience and flexibility.

Europe Fourth Party Logistics Market Competitive Landscape - Major competitors and market consolidation

The Europe Fourth Party Logistics market features a competitive landscape characterized by both established logistics giants and specialized 4PL providers. Major players such as Deutsche Post AG, DB Schenker, and UPS Supply Chain Solutions dominate the market with their extensive networks and comprehensive service offerings. These companies are increasingly focusing on digital transformation and sustainability initiatives to maintain their competitive edge. The market is also witnessing consolidation through mergers and acquisitions, as larger players seek to expand their capabilities and geographic reach. Regional players like GEFCO Group and CEVA Logistics AG are strengthening their positions by offering specialized solutions for specific industries. The competitive landscape is further shaped by the entry of technology-driven startups that are disrupting traditional 4PL models with innovative digital solutions. Competition is intensifying in areas such as supply chain visibility, real-time tracking, and sustainability, with providers differentiating themselves through their technological capabilities and industry expertise.

Executive Summary - High-level overview and key findings about Europe Fourth Party Logistics Market

The Europe Fourth Party Logistics market presents a compelling growth story, with the market size projected to increase from 21.62 billion in 2026 to 29.23 billion by 2033, representing a CAGR of 4.40%. This growth is driven by increasing demand for comprehensive supply chain solutions, technological advancements, and the need for greater supply chain visibility and control. The market is characterized by diverse service offerings, including the Synergy Plus Operating Model, Solution Integrator Model, and Industry Innovator Model, catering to various end-user segments such as aerospace & defense, automotive, and healthcare. Key market trends include digital transformation, sustainability initiatives, and the growing importance of risk management in supply chains. While the market faces challenges such as high implementation costs and integration complexities, opportunities abound in emerging sectors and technological innovations. The competitive landscape is dynamic, with both established players and new entrants vying for market share through innovation and strategic partnerships.

Europe Fourth Party Logistics Market Forecast - Projections for 2025-2032 period

The Europe Fourth Party Logistics market is poised for steady growth over the forecast period of 2025-2032, with the market size expected to reach 29.23 billion by 2033, up from 21.62 billion in 2026. This represents a compound annual growth rate of 4.40%, indicating sustained market expansion. The forecast period is expected to be characterized by continued digital transformation, with increased adoption of AI, IoT, and blockchain technologies driving efficiency and visibility in supply chain operations. The market is also likely to see growing demand from emerging sectors such as healthcare and consumer electronics, as these industries increasingly recognize the value of comprehensive 4PL solutions. Sustainability initiatives are expected to gain further momentum, with 4PL providers offering more eco-friendly logistics solutions to meet regulatory requirements and consumer expectations. The forecast also suggests increased market consolidation through strategic partnerships and acquisitions, as companies seek to expand their capabilities and geographic reach. Overall, the market outlook remains positive, with steady growth anticipated across all major segments and regions.

Europe Fourth Party Logistics Market Size and Share by Segmentation - Breakdown by {segmentData}

The Europe Fourth Party Logistics market can be segmented by both type and end-user, providing a comprehensive view of market dynamics. By type, the market is divided into three main categories: the Synergy Plus Operating Model, Solution Integrator Model, and Industry Innovator Model. Each of these models caters to different business needs and complexities, with the Solution Integrator Model currently holding the largest market share due to its versatility and widespread applicability across industries. The Industry Innovator Model is experiencing the fastest growth, driven by increasing demand for specialized solutions in sectors such as aerospace & defense and healthcare. By end-user, the market serves diverse industries including aerospace & defense, automotive, consumer electronics, food & beverage, industrial, healthcare, and retail. The automotive sector currently dominates the market, accounting for a significant share due to the complex supply chain requirements of this industry. However, the healthcare segment is expected to witness the highest growth rate, driven by increasing demand for efficient and compliant logistics solutions in the pharmaceutical and medical device sectors.

Global Europe Fourth Party Logistics Market Size and Share by Region - Geographic distribution

The Europe Fourth Party Logistics market exhibits distinct regional variations in terms of market size and growth dynamics. Western Europe, comprising countries such as Germany, France, and the United Kingdom, currently dominates the market, accounting for the largest share due to the presence of major logistics hubs and advanced infrastructure. This region is characterized by high adoption rates of 4PL services, particularly in the automotive and industrial sectors. Central and Eastern Europe are emerging as high-growth markets, driven by increasing industrialization and the relocation of manufacturing facilities to these regions. Countries like Poland, Czech Republic, and Hungary are witnessing rapid growth in 4PL adoption, particularly in the automotive and electronics sectors. Southern Europe, while currently smaller in market size, is showing promising growth potential, especially in countries like Italy and Spain, where there is increasing demand for sophisticated logistics solutions in the food & beverage and retail sectors. The Nordic countries are leading in terms of sustainability initiatives, driving demand for eco-friendly 4PL solutions.

Regional Analysis of the Europe Fourth Party Logistics Market - Detailed regional market performance

The Europe Fourth Party Logistics market demonstrates varied performance across different regions, reflecting diverse economic conditions, industrial landscapes, and regulatory environments. Western Europe, led by Germany, France, and the United Kingdom, represents the most mature market, characterized by high adoption rates of 4PL services and advanced technological infrastructure. This region is particularly strong in automotive and industrial logistics, with a growing emphasis on sustainability and digital transformation. Central and Eastern Europe are experiencing rapid growth, driven by increasing foreign direct investment and the relocation of manufacturing facilities. Countries like Poland and the Czech Republic are becoming key logistics hubs, particularly for automotive and electronics industries. Southern Europe, while traditionally more focused on tourism and agriculture, is seeing increasing demand for 4PL services in the food & beverage and retail sectors. The Nordic countries are at the forefront of sustainable logistics initiatives, with high adoption rates of green technologies and eco-friendly supply chain solutions. Each region presents unique opportunities and challenges, requiring 4PL providers to adapt their strategies to local market conditions and customer needs.

Leading Company Profiles in the Europe Fourth Party Logistics Market - Industry players and strategies

The Europe Fourth Party Logistics market is dominated by several key players, each with distinct strategies and market positions. Deutsche Post AG, through its DHL Supply Chain division, leads the market with its extensive global network and comprehensive service offerings. The company's strategy focuses on digital transformation and sustainability initiatives, leveraging advanced technologies to enhance supply chain visibility and efficiency. DB Schenker, another major player, emphasizes its expertise in complex, industry-specific logistics solutions, particularly in the automotive and industrial sectors. UPS Supply Chain Solutions differentiates itself through its strong technology platform and integrated air and ocean freight services. GEFCO Group specializes in automotive logistics, offering tailored solutions for this sector across Europe. CEVA Logistics AG focuses on providing end-to-end supply chain solutions with a strong emphasis on innovation and customer service. These companies are increasingly investing in digital capabilities, sustainability initiatives, and strategic partnerships to maintain their competitive edge. Additionally, smaller, specialized 4PL providers are carving out niches in specific industries or services, contributing to the market's diversity and dynamism.

Porter's Five Forces Analysis of the Europe Fourth Party Logistics Market - Competitive forces assessment

The Europe Fourth Party Logistics market is characterized by a complex interplay of competitive forces as analyzed through Porter's Five Forces framework. The threat of new entrants is moderate, as establishing a comprehensive 4PL operation requires significant capital investment, industry expertise, and established relationships with multiple logistics providers. However, technological advancements are lowering barriers to entry in some areas, particularly for digital-focused 4PL startups. The bargaining power of buyers is high, as large corporations have the ability to negotiate favorable terms and demand customized solutions. This is particularly true in sectors with complex supply chain requirements, such as automotive and aerospace. The bargaining power of suppliers is relatively low, as 4PL providers typically work with multiple logistics service providers, reducing dependency on any single supplier. The threat of substitute products or services is moderate, with traditional 3PL services and in-house logistics operations serving as potential alternatives. However, the unique value proposition of 4PL services in terms of comprehensive supply chain management and cost optimization provides a competitive advantage. Competitive rivalry is intense, with major players competing on service quality, technological capabilities, and industry expertise. This competition is driving innovation and pushing providers to continuously enhance their offerings.

SWOT Analysis of the Europe Fourth Party Logistics Market - Strengths, weaknesses, opportunities, threats

The Europe Fourth Party Logistics market exhibits a complex set of strengths, weaknesses, opportunities, and threats. Key strengths include the growing demand for comprehensive supply chain solutions, advanced technological infrastructure in Europe, and the presence of established logistics networks. The market also benefits from increasing awareness of the benefits of 4PL services among large corporations and the region's strong focus on sustainability and innovation. However, weaknesses such as high implementation costs, complex integration processes, and the need for specialized expertise pose challenges to market growth. Opportunities abound in emerging sectors such as healthcare and e-commerce, as well as in the development of sustainable logistics solutions and the adoption of advanced technologies like AI and blockchain. The market also has significant potential for growth in Central and Eastern Europe, driven by increasing industrialization and foreign investment. Threats to the market include economic uncertainties, regulatory changes, and increasing competition from both traditional logistics providers expanding their services and new technology-driven entrants. Additionally, data security concerns and the need for continuous innovation to meet evolving customer demands present ongoing challenges for market participants.

Europe Fourth Party Logistics Market Value Chain Analysis - Industry structure and value flow

The value chain in the Europe Fourth Party Logistics market is characterized by a complex network of activities and relationships that create and deliver value to end customers. At the core of this value chain are 4PL providers who act as orchestrators, integrating and managing multiple logistics service providers to deliver comprehensive supply chain solutions. The value chain begins with strategic planning and design, where 4PL providers analyze customer requirements and develop tailored logistics strategies. This is followed by the implementation phase, which involves selecting and managing various logistics service providers, including transportation companies, warehousing operators, and technology providers. The value chain also includes continuous monitoring and optimization of logistics operations, leveraging advanced technologies for real-time visibility and performance management. Key value-adding activities include supply chain design, carrier management, freight forwarding, customs brokerage, and value-added services such as packaging and assembly. The integration of technology throughout the value chain, particularly in areas such as data analytics, IoT, and blockchain, is becoming increasingly important in enhancing efficiency and creating competitive advantage. The final stage of the value chain involves performance measurement and reporting, ensuring transparency and continuous improvement in logistics operations.

Key Investment Insights in the Europe Fourth Party Logistics Market - Strategic investment recommendations

The Europe Fourth Party Logistics market presents several compelling investment opportunities for both strategic and financial investors. Key investment insights include the growing demand for digital transformation in logistics operations, which is driving investments in advanced technologies such as AI, IoT, and blockchain. Investors should consider opportunities in companies that are developing innovative solutions for supply chain visibility, real-time tracking, and predictive analytics. The market also offers significant potential in sustainability-focused logistics solutions, with increasing demand for eco-friendly transportation and warehousing options. Investments in companies that are developing green technologies or offering carbon-neutral logistics services are likely to see strong growth. The healthcare and pharmaceutical sectors represent another area of opportunity, driven by increasing demand for specialized logistics solutions that comply with strict regulatory requirements. Additionally, the market for last-mile delivery solutions and urban logistics is expected to grow rapidly, presenting opportunities for investment in innovative delivery models and technologies. Investors should also consider the potential for consolidation in the market, with opportunities to create value through strategic acquisitions and the integration of complementary service offerings.

Europe Fourth Party Logistics Market Conclusion - Summary and key takeaways

The Europe Fourth Party Logistics market is positioned for steady growth, with the market size projected to increase from 21.62 billion in 2026 to 29.23 billion by 2033, representing a CAGR of 4.40%. This growth is driven by increasing demand for comprehensive supply chain solutions, technological advancements, and the need for greater supply chain visibility and control. The market is characterized by diverse service offerings catering to various end-user segments, with the automotive sector currently dominating but healthcare showing the highest growth potential. Key trends shaping the market include digital transformation, sustainability initiatives, and the growing importance of risk management in supply chains. While the market faces challenges such as high implementation costs and integration complexities, opportunities abound in emerging sectors and technological innovations. The competitive landscape is dynamic, with both established players and new entrants vying for market share through innovation and strategic partnerships. Overall, the Europe Fourth Party Logistics market presents a compelling growth story, driven by the increasing complexity of global supply chains and the need for more efficient and flexible logistics solutions.

Research Methodology - How this research was conducted

The research for this Europe Fourth Party Logistics market report was conducted using a comprehensive methodology that combines both primary and secondary research approaches. Primary research involved extensive interviews with industry experts, including 4PL providers, logistics consultants, and end-users across various sectors. These interviews provided valuable insights into market trends, challenges, and future outlook. Secondary research encompassed a thorough analysis of industry reports, company financial statements, trade publications, and regulatory documents. Market size and growth projections were derived using a combination of top-down and bottom-up approaches, considering factors such as industry trends, economic indicators, and technological advancements. Data triangulation was employed to validate findings and ensure accuracy. The research also included a detailed analysis of competitive landscapes, company profiles, and recent developments in the market. Special attention was given to understanding regional variations and segment-specific dynamics. The methodology ensured a holistic view of the market, capturing both quantitative data and qualitative insights to provide a comprehensive analysis of the Europe Fourth Party Logistics market.

Research Scope - Coverage and limitations

This research report on the Europe Fourth Party Logistics market provides comprehensive coverage of the industry, focusing on key aspects such as market size, growth trends, competitive landscape, and future outlook. The scope includes an analysis of the market by type (Synergy Plus Operating Model, Solution Integrator Model, and Industry Innovator Model) and by end-user (aerospace & defense, automotive, consumer electronics, food & beverage, industrial, healthcare, and retail). The report covers major European countries and regions, providing insights into regional market dynamics and growth opportunities. However, it's important to note some limitations in the research scope. The report primarily focuses on the European market and does not extensively cover global trends or comparisons with other regions. Additionally, while the report provides detailed analysis of major market segments, some niche segments may not be covered in depth. The research is based on available data and industry insights up to a certain point, and rapid market changes or unforeseen events may impact future market dynamics. Despite these limitations, the report aims to provide a comprehensive and insightful analysis of the Europe Fourth Party Logistics market, serving as a valuable resource for industry stakeholders and decision-makers.

Key Companies and Recent Developments in the Europe Fourth Party Logistics Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Europe Fourth Party Logistics market is characterized by the presence of several key players who are continuously innovating and expanding their service offerings. Deutsche Post AG (DHL Supply Chain) has recently announced significant investments in automation and digitalization, including the implementation of AI-driven warehouse management systems and the expansion of its robotics capabilities. DB Schenker has focused on enhancing its sustainability initiatives, launching new eco-friendly transportation solutions and setting ambitious carbon reduction targets. UPS Supply Chain Solutions has strengthened its position through strategic partnerships, particularly in the technology sector, to enhance its digital capabilities and offer more integrated supply chain solutions. GEFCO Group has expanded its automotive logistics services, introducing new solutions for electric vehicle supply chains and battery logistics. CEVA Logistics AG has made significant strides in healthcare logistics, launching specialized services for pharmaceutical and medical device companies. XPO Logistics has invested heavily in last-mile delivery technologies, introducing new platforms for real-time tracking and customer communication. These companies, along with others like Logistics Plus Inc. and Allyn International Services Inc., are driving innovation in the market through strategic partnerships, technology investments, and the development of industry-specific solutions. Recent developments also include increased focus on sustainability, with many providers launching carbon-neutral logistics options and investing in green technologies.