Asia Pacific Automotive Parts Packaging Market Overview - Definition, scope, and significance

The Asia Pacific Automotive Parts Packaging Market encompasses the specialized packaging solutions designed for the safe transportation, storage, and handling of automotive components across the Asia Pacific region. This market serves the critical function of protecting automotive parts ranging from small electrical components to large engine assemblies during their journey through complex global supply chains. The significance of this market lies in its essential role in supporting the automotive manufacturing ecosystem, which represents one of the largest industrial sectors in the Asia Pacific region. With major automotive manufacturing hubs in countries like China, Japan, South Korea, and India, the demand for specialized packaging solutions has grown substantially as manufacturers seek to minimize damage, reduce logistics costs, and improve supply chain efficiency. The market includes various packaging types such as reusable containers, disposable packaging, protective materials, and specialized solutions for different automotive components including batteries, cooling systems, lighting components, engine parts, and electrical systems.

Asia Pacific Automotive Parts Packaging Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Asia Pacific Automotive Parts Packaging Market is driven by several key factors including the rapid growth of the automotive manufacturing sector in the region, increasing emphasis on supply chain optimization, and rising demand for sustainable packaging solutions. The expansion of electric vehicle production has created new packaging requirements for battery systems and related components, while the growing complexity of automotive electronics has necessitated more sophisticated protective packaging solutions. However, the market faces restraints such as fluctuating raw material prices, stringent environmental regulations regarding packaging waste, and the high initial investment required for reusable packaging systems. Challenges include managing the diverse packaging needs across different automotive components, addressing the skilled labor shortage in packaging operations, and adapting to rapidly changing automotive technologies. Opportunities exist in developing innovative packaging solutions for emerging automotive technologies, expanding into growing automotive markets in Southeast Asia, and leveraging digital technologies for smart packaging solutions that enhance supply chain visibility and efficiency.

Asia Pacific Automotive Parts Packaging Market Growth Trends - Current and emerging trends shaping the market

The Asia Pacific Automotive Parts Packaging Market is experiencing several transformative trends that are reshaping the industry landscape. One prominent trend is the increasing adoption of reusable and returnable packaging systems, driven by both economic and environmental considerations. Manufacturers are moving away from single-use packaging solutions toward durable, multi-trip packaging that can be tracked, sanitized, and reused multiple times throughout the supply chain. Another significant trend is the integration of smart packaging technologies, including RFID tags, IoT sensors, and QR codes, which enable real-time tracking, condition monitoring, and improved inventory management. The market is also witnessing a shift toward sustainable packaging materials, with growing demand for biodegradable, recyclable, and recycled-content packaging solutions that align with corporate sustainability goals and regulatory requirements. Additionally, the rise of e-commerce in the automotive aftermarket segment is driving demand for packaging solutions that can withstand longer distribution channels while providing enhanced protection for automotive parts shipped directly to consumers.

COVID-19 Impact on the Asia Pacific Automotive Parts Packaging Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly impacted the Asia Pacific Automotive Parts Packaging Market, causing disruptions across the entire automotive supply chain. During the initial phases of the pandemic, lockdowns and manufacturing shutdowns led to a sharp decline in automotive production, which directly affected the demand for automotive parts packaging. Supply chain disruptions resulted in material shortages and transportation challenges, forcing packaging manufacturers to adapt their operations and explore alternative sourcing strategies. However, the pandemic also accelerated certain market trends, including the adoption of automation in packaging operations to reduce dependency on manual labor and the increased focus on resilient supply chain strategies. As the automotive industry recovered, the packaging market demonstrated resilience through the implementation of enhanced safety protocols, increased hygiene standards in packaging facilities, and the acceleration of digitalization initiatives. The recovery trajectory has been characterized by a gradual return to pre-pandemic production levels, coupled with sustained demand for packaging solutions that support more flexible and responsive supply chain models.

Asia Pacific Automotive Parts Packaging Market Competitive Landscape - Major competitors and market consolidation

The competitive landscape of the Asia Pacific Automotive Parts Packaging Market is characterized by a mix of global packaging giants and regional specialists, with ongoing consolidation through mergers, acquisitions, and strategic partnerships. Major international players such as Mondi Group, Sealed Air Corp., and Smurfit Kappa leverage their global expertise and extensive product portfolios to serve large automotive manufacturers, while regional companies like CMTP Packaging Pty Ltd. and Ckdpack Packaging Inc. focus on localized solutions and customer relationships. The market has seen increasing consolidation as larger companies acquire specialized packaging firms to expand their technological capabilities and geographic presence. Competition is primarily based on product innovation, customization capabilities, sustainability credentials, and total cost of ownership rather than just unit pricing. Companies are investing in research and development to create packaging solutions that address emerging automotive technologies, particularly for electric vehicles and advanced driver assistance systems. The competitive intensity varies across different segments, with standardized packaging solutions facing more competition than highly specialized, customized packaging systems.

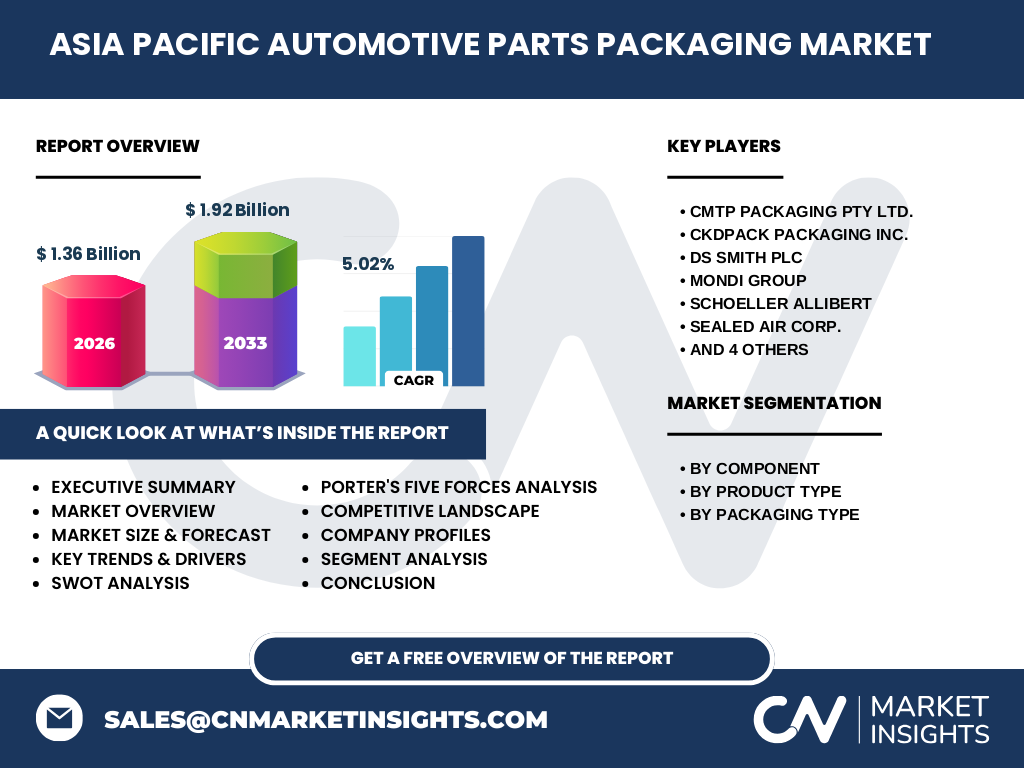

Executive Summary - High-level overview and key findings about Asia Pacific Automotive Parts Packaging Market

The Asia Pacific Automotive Parts Packaging Market represents a dynamic and evolving sector that plays a crucial role in supporting the region's automotive manufacturing industry. With a projected market size of 1.36 billion by 2026 and expected growth to 1.92 billion by 2033, representing a CAGR of 5.02%, the market demonstrates steady expansion driven by the region's automotive production growth and increasing sophistication of packaging requirements. The market is characterized by diverse segmentation across components (battery, cooling systems, lighting components, engine components, electricals), product types (pallets, crates, cartons, bags & pouches, trays), and packaging types (reusable and disposable). Key industry players including DS Smith Plc, Schoeller Allibert, Signode Packaging Systems, Sonoco Products Co., and The Nefab Group are actively shaping market dynamics through innovation and strategic initiatives. The market faces both opportunities and challenges, with sustainability requirements and technological advancements driving innovation while supply chain complexities and regulatory compliance present ongoing challenges. The regional analysis reveals varying growth rates and market characteristics across different Asia Pacific countries, reflecting the diverse nature of automotive manufacturing and packaging requirements throughout the region.

Asia Pacific Automotive Parts Packaging Market Forecast - Projections for 2025-2032 period

The Asia Pacific Automotive Parts Packaging Market is projected to experience steady growth throughout the 2025-2032 period, with the market expected to reach 1.36 billion by 2026 and expand further to 1.92 billion by 2033, representing a compound annual growth rate of 5.02%. This growth trajectory reflects the sustained expansion of automotive manufacturing activities across the Asia Pacific region, coupled with increasing demand for sophisticated packaging solutions that can protect increasingly complex automotive components. The forecast period is expected to witness accelerated adoption of reusable packaging systems as manufacturers seek to optimize total cost of ownership and meet sustainability targets. The growth will be particularly pronounced in emerging automotive markets within Southeast Asia, where increasing foreign direct investment in automotive manufacturing is creating new demand for packaging solutions. Technological advancements in packaging materials and design are expected to drive market evolution, with smart packaging solutions gaining traction among major automotive manufacturers. The forecast also accounts for potential market disruptions from economic fluctuations, regulatory changes, and technological shifts in the automotive industry, particularly the transition toward electric vehicles and autonomous driving technologies.

Asia Pacific Automotive Parts Packaging Market Size and Share by Segmentation - Breakdown by {segmentData}

The Asia Pacific Automotive Parts Packaging Market exhibits distinct segmentation patterns across components, product types, and packaging types, each contributing differently to the overall market dynamics. By component segmentation, engine components and electrical systems represent significant market shares due to their high value and sensitivity to damage during transportation, requiring specialized protective packaging solutions. The battery segment is experiencing rapid growth, driven by the electric vehicle revolution across the Asia Pacific region, with packaging requirements becoming increasingly stringent due to safety considerations. In terms of product type segmentation, pallets and crates dominate the market share due to their widespread use in bulk transportation and their ability to be reused multiple times, offering cost advantages over disposable alternatives. Cartons and bags & pouches serve the packaging needs for smaller components and aftermarket parts, representing a substantial but smaller market share. The packaging type segmentation reveals that reusable packaging systems are gaining market share over disposable options, reflecting the industry's shift toward sustainability and cost optimization, although disposable packaging continues to serve specific applications where return logistics are impractical.

Global Asia Pacific Automotive Parts Packaging Market Size and Share by Region - Geographic distribution

The Asia Pacific Automotive Parts Packaging Market demonstrates significant geographic variation in terms of market size and share, reflecting the diverse automotive manufacturing landscape across the region. China dominates the regional market, accounting for the largest share due to its massive automotive production capacity and extensive supplier network, with major packaging hubs located in manufacturing centers such as Shanghai, Guangzhou, and Tianjin. Japan represents another substantial market share, characterized by advanced packaging technologies and a strong emphasis on quality and precision in automotive parts protection. South Korea's market share is driven by its sophisticated automotive industry, particularly in electric vehicle production, creating demand for specialized packaging solutions. India is emerging as a significant growth market, with increasing automotive production and a growing focus on domestic manufacturing under initiatives like "Make in India." Southeast Asian countries including Thailand, Vietnam, and Indonesia are experiencing rapid market growth as they attract automotive manufacturing investments, though their current market shares remain smaller compared to the established automotive manufacturing giants. Australia and New Zealand represent niche markets with specific requirements for packaging solutions adapted to their geographic isolation and transportation challenges.

Regional Analysis of the Asia Pacific Automotive Parts Packaging Market - Detailed regional market performance

The regional analysis of the Asia Pacific Automotive Parts Packaging Market reveals distinct market characteristics and growth patterns across different countries and sub-regions. China's market performance is characterized by massive scale and rapid innovation, with packaging companies investing heavily in automation and smart packaging technologies to serve the world's largest automotive market. The Chinese market is also experiencing regulatory pressure to reduce packaging waste, driving adoption of reusable systems and sustainable materials. Japan's market demonstrates mature growth with a strong emphasis on precision packaging solutions for high-value components, particularly for hybrid and electric vehicles, reflecting the country's technological leadership in automotive manufacturing. South Korea's market performance is closely tied to its automotive export activities, with packaging solutions designed to withstand long-distance transportation while minimizing damage and returns. India's market is showing dynamic growth, driven by increasing domestic production and the government's push for local manufacturing, though challenges remain in terms of infrastructure and skilled workforce availability. The Southeast Asian markets are experiencing the fastest growth rates, albeit from smaller bases, as countries like Vietnam and Thailand establish themselves as automotive manufacturing hubs, creating demand for both basic and increasingly sophisticated packaging solutions.

Leading Company Profiles in the Asia Pacific Automotive Parts Packaging Market - Industry players and strategies

The Asia Pacific Automotive Parts Packaging Market features a diverse array of leading companies, each employing distinct strategies to capture market share and drive growth. Mondi Group has established a strong presence through its focus on sustainable packaging solutions and extensive product portfolio, leveraging its global expertise while adapting to regional requirements. Sealed Air Corp. differentiates itself through innovative protective packaging technologies and a strong emphasis on automation and smart packaging integration. DS Smith Plc has built its strategy around circular economy principles, offering comprehensive packaging solutions that emphasize recyclability and reuse. Schoeller Allibert specializes in reusable plastic packaging systems, particularly crates and pallets, capitalizing on the growing demand for returnable packaging in automotive supply chains. Smurfit Kappa leverages its expertise in paper-based packaging to serve the automotive aftermarket segment while developing specialized solutions for original equipment manufacturers. Sonoco Products Co. focuses on precision-engineered packaging solutions for high-value automotive components, while The Nefab Group emphasizes global supply chain optimization through its integrated packaging and logistics services. These companies are pursuing strategies that include geographic expansion, technological innovation, sustainability initiatives, and strategic partnerships with automotive manufacturers to strengthen their market positions.

Porter's Five Forces Analysis of the Asia Pacific Automotive Parts Packaging Market - Competitive forces assessment

The Porter's Five Forces analysis of the Asia Pacific Automotive Parts Packaging Market reveals a competitive landscape shaped by several key forces. The threat of new entrants remains moderate due to the significant capital requirements for establishing packaging manufacturing facilities and the importance of established relationships with automotive manufacturers. However, opportunities exist for specialized packaging companies that can address emerging automotive technologies or regional market gaps. The bargaining power of buyers, primarily automotive OEMs and Tier 1 suppliers, is substantial given their large purchase volumes and the commoditized nature of certain packaging solutions, though this is somewhat mitigated for highly specialized or customized packaging systems. Suppliers of raw materials wield considerable influence, particularly for plastic resins and specialty materials, though packaging companies often mitigate this through long-term contracts and diversified sourcing strategies. The threat of substitute products exists, particularly from alternative packaging materials or in-house packaging solutions developed by large automotive manufacturers, though the complexity of automotive supply chains generally favors specialized packaging providers. Competitive rivalry is intense, characterized by price competition for standard packaging solutions and differentiation through innovation, quality, and service for specialized applications. The overall industry attractiveness is moderate to high, supported by steady market growth and the essential nature of packaging in automotive manufacturing, though profitability varies significantly across different market segments and regions.

SWOT Analysis of the Asia Pacific Automotive Parts Packaging Market - Strengths, weaknesses, opportunities, threats

The Asia Pacific Automotive Parts Packaging Market exhibits distinct strengths, weaknesses, opportunities, and threats that shape its competitive dynamics and growth potential. Key strengths include the region's robust automotive manufacturing base, which provides a stable demand foundation, and the increasing sophistication of packaging technologies that enable better protection and supply chain efficiency. The market also benefits from strong innovation capabilities and the presence of both global packaging giants and agile regional players that can address diverse customer needs. However, weaknesses exist in the form of high initial investment requirements for advanced packaging systems and the challenges associated with managing complex reverse logistics for reusable packaging. Environmental concerns regarding packaging waste and the volatility of raw material prices also present ongoing challenges. Significant opportunities are emerging from the electric vehicle revolution, which is creating demand for new packaging solutions for battery systems and electronic components, as well as from the growing emphasis on sustainability that favors innovative, eco-friendly packaging materials and designs. Threats to the market include potential economic slowdowns affecting automotive production, increasing regulatory pressures regarding packaging waste and carbon emissions, and the risk of technological disruption from alternative packaging approaches or in-house solutions developed by automotive manufacturers.

Asia Pacific Automotive Parts Packaging Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the Asia Pacific Automotive Parts Packaging Market reveals a complex ecosystem of interconnected activities that create and deliver value to end customers. The chain begins with raw material suppliers who provide plastics, paper, metals, and specialty materials that form the foundation of packaging solutions. These materials flow to packaging manufacturers who transform them into finished products through processes including injection molding, thermoforming, and converting operations. The manufacturers then distribute these packaging solutions through various channels, including direct sales to large automotive OEMs, distribution partnerships for smaller customers, and aftermarket channels. Value is added at multiple stages, including through design and engineering services that create customized packaging solutions, quality control processes that ensure protection capabilities, and logistics services that manage the movement of packaging throughout the supply chain. The value chain also encompasses reverse logistics operations for reusable packaging systems, including collection, inspection, cleaning, and redistribution of packaging assets. Supporting activities such as research and development, marketing, and customer service play crucial roles in differentiating offerings and creating competitive advantages. The value chain is characterized by increasing integration and collaboration among participants, with packaging companies working closely with automotive manufacturers to develop solutions that optimize total supply chain costs rather than focusing solely on packaging unit costs.

Key Investment Insights in the Asia Pacific Automotive Parts Packaging Market - Strategic investment recommendations

The Asia Pacific Automotive Parts Packaging Market presents compelling investment opportunities for both strategic and financial investors, with several key areas warranting particular attention. Investments in automation and digitalization technologies offer significant potential returns, as packaging companies seek to enhance productivity, reduce labor costs, and improve quality consistency in response to rising labor costs and increasing quality demands from automotive manufacturers. The growing emphasis on sustainability creates investment opportunities in innovative packaging materials and designs that reduce environmental impact while maintaining protection performance, particularly solutions that address the specific challenges of automotive component packaging. Geographic expansion into emerging automotive manufacturing hubs in Southeast Asia represents another attractive investment thesis, as countries like Vietnam, Thailand, and Indonesia experience rapid growth in automotive production and associated packaging demand. Strategic acquisitions of specialized packaging companies can provide access to proprietary technologies, regional market presence, or capabilities in emerging automotive segments such as electric vehicles. Investments in smart packaging technologies, including IoT-enabled tracking and monitoring systems, offer potential for creating differentiated solutions that address automotive manufacturers' increasing focus on supply chain visibility and efficiency. Additionally, investments in reverse logistics capabilities and packaging asset management systems can capture value in the growing reusable packaging segment, where effective management of packaging assets throughout their lifecycle is critical to economic viability.

Asia Pacific Automotive Parts Packaging Market Conclusion - Summary and key takeaways

The Asia Pacific Automotive Parts Packaging Market represents a vital component of the region's automotive manufacturing ecosystem, characterized by steady growth, technological innovation, and evolving sustainability requirements. With the market projected to grow from 1.36 billion in 2026 to 1.92 billion by 2033 at a CAGR of 5.02%, the sector demonstrates resilience and adaptability in the face of changing automotive industry dynamics. The market's segmentation across components, product types, and packaging types reflects the diverse and specialized nature of automotive packaging requirements, while the competitive landscape features a mix of global leaders and regional specialists competing on innovation, sustainability, and total cost of ownership. Key trends shaping the market include the shift toward reusable packaging systems, the integration of smart technologies, and the increasing focus on sustainable materials and designs. While the market faces challenges including regulatory pressures, raw material volatility, and complex supply chain requirements, significant opportunities exist in emerging automotive technologies, particularly electric vehicles, and in expanding geographic markets. The value chain analysis reveals a complex ecosystem where collaboration and integration are increasingly important for creating competitive advantages. Overall, the Asia Pacific Automotive Parts Packaging Market presents a compelling growth story supported by the region's automotive manufacturing strength and the essential nature of effective packaging in modern automotive supply chains.

Research Methodology - How this research was conducted

The research methodology for this Asia Pacific Automotive Parts Packaging Market analysis employed a comprehensive, multi-faceted approach to ensure accuracy, reliability, and depth of insight. Primary research formed the foundation of the study, involving extensive interviews with key industry stakeholders including packaging manufacturers, automotive OEMs, Tier 1 suppliers, raw material providers, and industry experts across the Asia Pacific region. These interviews provided firsthand insights into market dynamics, growth drivers, challenges, and emerging trends. Secondary research complemented the primary data through analysis of industry reports, company financial statements, trade publications, government statistics, and proprietary databases covering automotive production and packaging industry performance. The market size and forecast projections were developed using a combination of top-down and bottom-up approaches, triangulating data from multiple sources to validate estimates. Segmentation analysis was conducted based on component categories, product types, and packaging types, with market shares derived from both quantitative data and qualitative assessments of industry structure. Geographic analysis incorporated country-level economic data, automotive production statistics, and regional packaging industry trends to develop comprehensive regional insights. The competitive landscape assessment involved detailed company profiling, analysis of strategic initiatives, and evaluation of market positioning based on product portfolios, technological capabilities, and geographic presence. Throughout the research process, data quality was ensured through cross-verification across multiple sources and expert validation of key findings and projections.

Research Scope - Coverage and limitations

The research scope for this Asia Pacific Automotive Parts Packaging Market analysis encompasses the comprehensive examination of packaging solutions specifically designed for automotive components across the Asia Pacific region, with coverage extending from 2020 to the forecast period through 2033. The study includes detailed analysis of packaging for various automotive components including batteries, cooling systems, lighting components, engine components, and electrical systems, examining both reusable and disposable packaging types across product categories such as pallets, crates, cartons, bags & pouches, and trays. Geographic coverage includes major automotive manufacturing countries in the Asia Pacific region, with particular focus on China, Japan, South Korea, India, and emerging markets in Southeast Asia. The research examines market dynamics including drivers, restraints, opportunities, and challenges, along with competitive landscape analysis of key industry players. However, certain limitations exist within the research scope, including the exclusion of packaging for finished vehicles (which represents a distinct market segment), limited coverage of aftermarket packaging beyond original equipment applications, and the inherent challenges in obtaining precise market share data for certain regional and product-specific segments due to the fragmented nature of the industry and limited public disclosure of packaging-specific financial information by many companies. Additionally, while the research provides comprehensive qualitative insights, certain quantitative data points particularly at the regional and country level may be subject to estimation based on available industry information and expert judgment.

Key Companies and Recent Developments in the Asia Pacific Automotive Parts Packaging Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Asia Pacific Automotive Parts Packaging Market features several key companies that have recently announced significant developments shaping the industry landscape. CMTP Packaging Pty Ltd. has expanded its operations in Australia with the launch of new sustainable packaging solutions specifically designed for electric vehicle components, including specialized battery packaging systems that address safety and thermal management requirements. Ckdpack Packaging Inc. recently announced a strategic partnership with a major Chinese automotive manufacturer to develop custom reusable packaging systems for complex engine components, incorporating RFID tracking technology to enhance supply chain visibility. DS Smith Plc unveiled its latest innovation in paper-based protective packaging, introducing a new corrugated solution with enhanced cushioning properties that reduces material usage while improving protection for sensitive electronic components. Mondi Group has made significant investments in its Asian manufacturing facilities, with a new production line in Vietnam dedicated to producing recyclable packaging solutions for automotive lighting components, responding to increasing sustainability demands from automotive customers. Schoeller Allibert launched an advanced pallet pooling service tailored for the automotive industry, offering real-time tracking and condition monitoring to optimize asset utilization and reduce total cost of ownership for automotive manufacturers. Sealed Air Corp. introduced its next-generation protective packaging material that combines superior cushioning with improved recyclability, targeting the growing market for packaging sensitive electric vehicle components. Smurfit Kappa announced the expansion of its regional design center in Thailand, focusing on developing innovative packaging solutions for the rapidly growing automotive manufacturing sector in Southeast Asia. Sonoco Products