Asia Pacific Data Center Construction Market Overview - Definition, scope, and significance

The Asia Pacific Data Center Construction Market encompasses the design, development, and building of data center facilities across the Asia Pacific region. This market includes all aspects of data center construction, from site selection and architectural design to mechanical and electrical systems installation. The significance of this market lies in its critical role in supporting the region's rapidly growing digital economy, cloud computing infrastructure, and increasing demand for data storage and processing capabilities. As businesses and consumers generate unprecedented volumes of data, the construction of robust and efficient data centers has become essential for economic growth, technological advancement, and digital transformation across various industries in the Asia Pacific region.

Asia Pacific Data Center Construction Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Asia Pacific Data Center Construction Market is primarily driven by the exponential growth of digital data, increasing adoption of cloud computing services, and the proliferation of Internet of Things (IoT) devices across the region. Government initiatives to promote digital infrastructure and the rise of artificial intelligence and big data analytics further fuel market growth. However, the market faces restraints such as high initial capital investment requirements, complex regulatory environments, and challenges in securing suitable land for data center construction. Additionally, the need for skilled labor and the increasing focus on energy efficiency and sustainability present both challenges and opportunities for market players. Opportunities lie in the development of edge computing facilities, the integration of renewable energy sources, and the adoption of modular and prefabricated construction techniques to accelerate deployment and reduce costs.

Asia Pacific Data Center Construction Market Growth Trends - Current and emerging trends shaping the market

The Asia Pacific Data Center Construction Market is experiencing several notable growth trends that are shaping its evolution. One significant trend is the shift towards hyperscale data centers to accommodate the massive data processing needs of major cloud service providers and technology companies. Another emerging trend is the increasing adoption of modular and prefabricated data center construction methods, which offer faster deployment times and greater flexibility. The market is also witnessing a growing emphasis on energy efficiency and sustainability, with many new data center projects incorporating renewable energy sources and innovative cooling technologies. Additionally, there is a rising demand for edge data centers to support low-latency applications and the growing Internet of Things (IoT) ecosystem. The integration of artificial intelligence and machine learning in data center operations and management is another trend that is gaining traction in the Asia Pacific region.

COVID-19 Impact on the Asia Pacific Data Center Construction Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the Asia Pacific Data Center Construction Market, initially causing disruptions in supply chains, labor availability, and project timelines. However, the pandemic also accelerated the demand for digital services and remote work capabilities, leading to increased urgency for data center expansion and construction. As businesses rapidly shifted to digital operations, the need for robust data infrastructure became more critical than ever. This surge in demand has driven many companies to expedite their data center construction plans, contributing to a strong recovery trajectory for the market. The pandemic has also highlighted the importance of resilient and scalable data center infrastructure, potentially leading to long-term changes in how data centers are designed and constructed in the region.

Asia Pacific Data Center Construction Market Competitive Landscape - Major competitors and market consolidation

The Asia Pacific Data Center Construction Market features a diverse competitive landscape with a mix of global and regional players. Major international companies such as AECOM, DPR Construction, and Turner Construction compete alongside regional specialists like Fujitsu Limited and Hitachi Vantara Corporation. The market also includes niche players focusing on specific aspects of data center construction, such as electrical design (Schneider Electric SE) and mechanical systems (Rittal Gmbh & Co. KG). While there has been some consolidation in the market through mergers and acquisitions, the competitive landscape remains relatively fragmented. Companies are increasingly forming strategic partnerships and alliances to leverage complementary strengths and expand their market presence. The competitive dynamics are further influenced by the growing involvement of technology giants like Google, Amazon, and Microsoft, who are investing heavily in building their own data center facilities across the region.

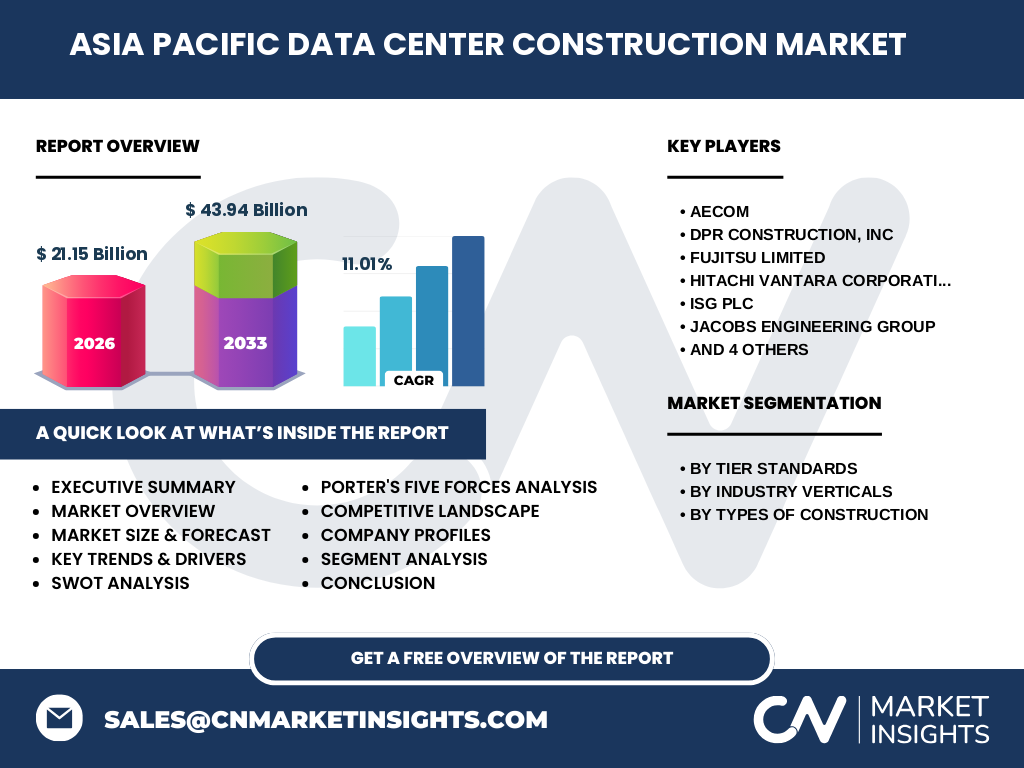

Executive Summary - High-level overview and key findings about Asia Pacific Data Center Construction Market

The Asia Pacific Data Center Construction Market is experiencing robust growth, driven by the region's rapid digital transformation and increasing demand for data processing capabilities. With a market size of 21.15 Billion in 2026 and a projected growth to 43.94 Billion by 2033, the market is expected to grow at a CAGR of 11.01% during the forecast period. This growth is fueled by factors such as the proliferation of cloud computing, the rise of big data analytics, and the increasing adoption of Internet of Things (IoT) devices across various industries. The market is segmented by tier standards, industry verticals, and types of construction, offering diverse opportunities for stakeholders. Key players in the market are focusing on innovative construction techniques, energy efficiency, and sustainability to gain a competitive edge. The COVID-19 pandemic has further accelerated the demand for data center infrastructure, highlighting its critical role in supporting digital economies.

Asia Pacific Data Center Construction Market Forecast - Projections for 2025-2032 period

The Asia Pacific Data Center Construction Market is poised for significant growth over the forecast period of 2025-2032. Starting from a market size of 21.15 Billion in 2026, the market is expected to reach 43.94 Billion by 2033, representing a compound annual growth rate (CAGR) of 11.01%. This robust growth trajectory is driven by several factors, including the increasing demand for cloud services, the proliferation of data-intensive technologies, and the region's expanding digital economy. The forecast period is likely to see continued investment in hyperscale data centers, with a particular focus on edge computing facilities to support low-latency applications. Additionally, the market is expected to witness a surge in sustainable and energy-efficient data center construction projects, driven by both regulatory pressures and corporate sustainability goals. The forecast also suggests a growing trend towards modular and prefabricated construction methods to accelerate deployment and reduce costs.

Asia Pacific Data Center Construction Market Size and Share by Segmentation - Breakdown by {segmentData}

The Asia Pacific Data Center Construction Market is segmented by tier standards, industry verticals, and types of construction, each contributing differently to the overall market size and share. In terms of tier standards, Tier 3 data centers are expected to hold a significant share due to their balance of redundancy and cost-effectiveness, making them popular among a wide range of industries. The BFSI (Banking, Financial Services, and Insurance) sector is likely to dominate the industry verticals segment, driven by the need for secure and reliable data storage and processing capabilities. Among the types of construction, general construction is expected to account for the largest share, encompassing the overall building structure and basic infrastructure. However, electrical design and mechanical design segments are also crucial, as they ensure the proper functioning and efficiency of data center operations. The market share distribution may vary across different countries in the Asia Pacific region, reflecting local economic conditions, technological adoption rates, and regulatory environments.

Global Asia Pacific Data Center Construction Market Size and Share by Region - Geographic distribution

The Asia Pacific Data Center Construction Market exhibits diverse growth patterns across different regions within the Asia Pacific area. While specific regional market share data is not provided, it is evident that countries like China, Japan, India, and Singapore are likely to be major contributors to the market's overall size and growth. China, with its large population and rapidly growing digital economy, is expected to hold a significant share of the market. Japan, known for its technological advancements and high data consumption, is another key market. India, with its booming IT sector and increasing digitalization efforts, presents substantial growth opportunities. Singapore, as a regional hub for data center operations, also plays a crucial role in the market's geographic distribution. Other countries in Southeast Asia, such as Indonesia, Malaysia, and Thailand, are emerging as important markets due to their growing digital economies and increasing demand for data center infrastructure.

Regional Analysis of the Asia Pacific Data Center Construction Market - Detailed regional market performance

The Asia Pacific Data Center Construction Market shows varied performance across different regions, reflecting the diverse economic landscapes and technological adoption rates in the area. In East Asia, countries like China and Japan are experiencing robust growth in data center construction, driven by their large populations, advanced technological infrastructure, and high data consumption rates. China, in particular, is witnessing significant investments in hyperscale data centers to support its rapidly growing digital economy and cloud services market. Japan's market is characterized by a focus on energy-efficient and earthquake-resistant data center designs, reflecting the country's technological prowess and geographical considerations. In Southeast Asia, markets such as Singapore, Indonesia, and Malaysia are emerging as key players, with Singapore serving as a major regional hub for data center operations. India's data center construction market is experiencing rapid growth, fueled by its expanding IT sector and increasing digitalization efforts across various industries. Australia and New Zealand are also contributing to the regional market, with a focus on sustainable and energy-efficient data center designs to address environmental concerns.

Leading Company Profiles in the Asia Pacific Data Center Construction Market - Industry players and strategies

The Asia Pacific Data Center Construction Market features a mix of global and regional players, each employing distinct strategies to gain a competitive edge. AECOM, a global infrastructure firm, leverages its extensive experience in large-scale construction projects to offer comprehensive data center construction services. DPR Construction, known for its technical expertise, focuses on delivering complex data center projects with innovative solutions. Fujitsu Limited and Hitachi Vantara Corporation, both Japanese companies, bring their technological prowess to the market, offering integrated data center solutions that combine construction with advanced IT infrastructure. ISG PLC, a global technology research and advisory firm, provides strategic consulting services to guide data center construction projects. Jacobs Engineering Group offers a wide range of engineering and construction services, catering to the diverse needs of the data center industry. Schneider Electric SE specializes in energy management and automation solutions, crucial for efficient data center operations. These companies are increasingly focusing on sustainable construction practices, energy efficiency, and the integration of smart technologies to differentiate themselves in the competitive market landscape.

Porter's Five Forces Analysis of the Asia Pacific Data Center Construction Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the Asia Pacific Data Center Construction Market. The threat of new entrants is moderate, as the market requires significant capital investment and technical expertise, creating barriers to entry. However, the growing demand for data center infrastructure may attract new players, especially those with strong financial backing. The bargaining power of buyers is increasing, as large technology companies and cloud service providers have substantial influence over project specifications and pricing. The bargaining power of suppliers is moderate, with a mix of specialized equipment manufacturers and general construction material suppliers. The threat of substitute products or services is relatively low, as data centers remain essential for digital infrastructure. However, advancements in edge computing and modular data centers may present alternative solutions. The intensity of competitive rivalry is high, with numerous global and regional players competing for market share. This competition is driving innovation in construction techniques, energy efficiency, and sustainability practices among market participants.

SWOT Analysis of the Asia Pacific Data Center Construction Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Asia Pacific Data Center Construction Market reveals several key factors influencing its growth and development. Strengths of the market include the region's rapid digital transformation, increasing demand for cloud services, and the presence of major technology hubs. The market also benefits from the availability of skilled labor and advanced construction technologies in many Asia Pacific countries. However, weaknesses such as high initial capital investment requirements, complex regulatory environments, and challenges in securing suitable land for data center construction pose significant hurdles. Opportunities in the market are abundant, including the growing demand for edge computing facilities, the integration of renewable energy sources, and the adoption of modular construction techniques. Threats to the market include potential economic slowdowns, geopolitical tensions affecting cross-border data flows, and increasing competition for skilled labor and resources. Additionally, the market faces challenges related to energy consumption and environmental sustainability, which may lead to stricter regulations and higher operational costs.

Asia Pacific Data Center Construction Market Value Chain Analysis - Industry structure and value flow

The value chain of the Asia Pacific Data Center Construction Market encompasses a complex network of activities and stakeholders involved in bringing data center projects from conception to operation. The chain begins with land acquisition and site selection, followed by architectural and engineering design phases. This is succeeded by the procurement of specialized equipment and materials, including servers, cooling systems, and power distribution units. The construction phase involves general construction, electrical design, and mechanical design, each contributing unique value to the project. After construction, the focus shifts to commissioning and testing to ensure optimal performance. Finally, ongoing maintenance and upgrades form the last link in the value chain. Throughout this process, various stakeholders, including construction companies, equipment manufacturers, technology providers, and facility management firms, contribute their expertise to create value. The integration of advanced technologies, such as Building Information Modeling (BIM) and Internet of Things (IoT) sensors, is increasingly enhancing the efficiency and effectiveness of the value chain, enabling better project management and operational optimization.

Key Investment Insights in the Asia Pacific Data Center Construction Market - Strategic investment recommendations

The Asia Pacific Data Center Construction Market presents numerous investment opportunities for stakeholders looking to capitalize on the region's growing digital infrastructure needs. Investors should consider focusing on markets with high growth potential, such as emerging economies in Southeast Asia and India, where digitalization efforts are accelerating. Investments in sustainable and energy-efficient data center technologies are likely to yield significant returns, given the increasing emphasis on environmental responsibility and operational cost reduction. The adoption of modular and prefabricated construction methods offers opportunities for investors to support faster deployment and scalability of data center facilities. Additionally, investments in edge computing infrastructure to support low-latency applications and the Internet of Things (IoT) ecosystem are expected to be lucrative. Strategic partnerships between construction firms and technology companies can also provide valuable investment prospects, combining expertise in physical infrastructure with cutting-edge digital solutions. However, investors should be mindful of potential risks, including regulatory challenges, land acquisition issues, and the need for continuous technological upgrades to remain competitive in this rapidly evolving market.

Asia Pacific Data Center Construction Market Conclusion - Summary and key takeaways

The Asia Pacific Data Center Construction Market is poised for substantial growth, driven by the region's rapid digital transformation and increasing demand for data processing capabilities. With a projected CAGR of 11.01% from 2026 to 2033, the market is expected to nearly double in size, reaching 43.94 Billion by 2033. Key factors fueling this growth include the proliferation of cloud computing, the rise of big data analytics, and the increasing adoption of Internet of Things (IoT) devices across various industries. The market is characterized by a diverse competitive landscape, with both global and regional players vying for market share through innovative construction techniques and sustainable practices. While challenges such as high initial capital investment and complex regulatory environments exist, the market presents numerous opportunities for stakeholders, including investments in edge computing, renewable energy integration, and modular construction methods. As the region continues to embrace digital technologies, the Asia Pacific Data Center Construction Market will play a crucial role in supporting the digital economy and driving technological advancement across various sectors.

Research Methodology - How this research was conducted

The research methodology for this Asia Pacific Data Center Construction Market analysis involved a comprehensive approach to gather and analyze data from multiple sources. Primary research was conducted through interviews with industry experts, data center operators, and key stakeholders in the construction and technology sectors. Secondary research included an extensive review of industry reports, company annual reports, press releases, and relevant publications. Market size and growth projections were derived using a combination of top-down and bottom-up approaches, considering factors such as regional economic indicators, technology adoption rates, and industry trends. The segmentation analysis was based on data from various industry sources and expert opinions. Competitive landscape assessment involved analyzing company profiles, market positioning, and recent developments. The research also incorporated insights from Porter's Five Forces analysis and SWOT analysis to provide a comprehensive understanding of the market dynamics. It's important to note that while this methodology aims to provide accurate and reliable information, the rapidly evolving nature of the data center industry may lead to changes in market conditions between the time of research and publication.

Research Scope - Coverage and limitations

The research scope for this Asia Pacific Data Center Construction Market analysis encompasses the entire Asia Pacific region, including major economies such as China, Japan, India, Australia, and Southeast Asian countries. The study covers various aspects of data center construction, including market size, growth trends, competitive landscape, and key industry segments. The analysis includes different tier standards of data centers, various industry verticals that utilize data center services, and the types of construction involved in data center development. However, it's important to note that the research has certain limitations. The study may not capture every minor market player or niche segment within the data center construction industry. Additionally, the rapidly evolving nature of technology and regulatory environments in the Asia Pacific region may lead to changes in market dynamics that are not immediately reflected in the research. The study also focuses primarily on the construction aspect of data centers and may not delve deeply into operational aspects or long-term performance metrics of completed facilities.

Key Companies and Recent Developments in the Asia Pacific Data Center Construction Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Asia Pacific Data Center Construction Market features several key players driving innovation and growth in the industry. AECOM, a global infrastructure firm, has been focusing on sustainable construction practices and has recently announced partnerships to develop energy-efficient data center projects in the region. DPR Construction, known for its technical expertise, has launched new modular data center solutions to accelerate deployment times. Fujitsu Limited has introduced advanced cooling technologies for data centers, aiming to improve energy efficiency and reduce operational costs. Hitachi Vantara Corporation has announced strategic collaborations with cloud service providers to expand its data center construction capabilities. ISG PLC has recently published research on the impact of edge computing on data center design and construction trends in Asia Pacific. Jacobs Engineering Group has secured major contracts for hyperscale data center projects in emerging markets. Schneider Electric SE has launched new integrated data center infrastructure management solutions to optimize operations. These companies, along with others like Rittal Gmbh & Co. KG, Tripp Lite, and Turner Construction, are continuously innovating and forming strategic partnerships to address the evolving needs of the Asia Pacific data center market.