North America Medical Imaging Equipment Services Market Overview - Definition, scope, and significance

The North America Medical Imaging Equipment Services Market encompasses the comprehensive range of services associated with the maintenance, repair, upgrade, and management of medical imaging equipment across the healthcare sector. This market includes critical imaging modalities such as Computed Tomography (CT), Magnetic Resonance Imaging (MRI), Ultrasound, and X-Ray systems, along with associated services like equipment repair and maintenance, refurbished systems, technical training, equipment removal and relocation, and software upgrades. The market serves two primary end-user segments: hospitals and diagnostic centers, with service delivery through Original Equipment Manufacturers (OEMs) and Independent Service Organizations (ISOs). This market plays a vital role in ensuring the operational efficiency, safety, and longevity of medical imaging equipment, which is essential for accurate diagnosis and treatment planning in modern healthcare.

North America Medical Imaging Equipment Services Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The North America Medical Imaging Equipment Services Market is driven by several key factors including the increasing adoption of advanced imaging technologies, the growing prevalence of chronic diseases requiring diagnostic imaging, and the need for cost-effective maintenance solutions. The aging medical imaging equipment fleet across healthcare facilities creates ongoing demand for repair and maintenance services. Additionally, the trend toward value-based healthcare and the emphasis on reducing equipment downtime are significant drivers. However, the market faces restraints such as high service costs, the complexity of modern imaging systems, and the shortage of skilled technicians. Challenges include the rapid technological advancements that require continuous training and the integration of software upgrades with existing systems. Opportunities exist in the growing demand for refurbished equipment, the expansion of telemedicine and remote diagnostics, and the increasing focus on preventive maintenance programs to extend equipment lifespan and improve operational efficiency.

North America Medical Imaging Equipment Services Market Growth Trends - Current and emerging trends shaping the market

The North America Medical Imaging Equipment Services Market is experiencing several notable growth trends. There is a significant shift toward predictive maintenance and remote monitoring solutions, enabled by the Internet of Things (IoT) and artificial intelligence, which allow for proactive identification of equipment issues before they cause downtime. The market is also witnessing increased adoption of service contracts that bundle multiple services for cost efficiency. Another emerging trend is the growing preference for refurbished imaging equipment, driven by budget constraints in healthcare facilities and the need for sustainable practices. The integration of advanced software solutions for image processing and data management is creating new service opportunities. Additionally, there is a trend toward specialized technical training programs to address the skills gap in servicing complex imaging systems. The market is also seeing increased collaboration between OEMs and ISOs to provide comprehensive service solutions that combine manufacturer expertise with independent flexibility.

COVID-19 Impact on the North America Medical Imaging Equipment Services Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the North America Medical Imaging Equipment Services Market, initially causing disruptions in routine diagnostic procedures and elective imaging services as healthcare resources were redirected to pandemic response. Many non-urgent equipment maintenance and upgrades were postponed, leading to a temporary decline in service demand. However, the pandemic also accelerated certain trends, including the adoption of remote monitoring and telemedicine solutions, which increased the need for software upgrades and virtual technical support services. The focus on infection control and equipment sterilization created new service requirements. As the healthcare system recovers, the market is experiencing a rebound driven by the backlog of deferred maintenance, the need to upgrade aging equipment, and the renewed emphasis on diagnostic capabilities for early disease detection. The recovery trajectory shows steady growth as healthcare facilities prioritize equipment reliability and operational efficiency in the post-pandemic era.

North America Medical Imaging Equipment Services Market Competitive Landscape - Major competitors and market consolidation

The North America Medical Imaging Equipment Services Market features a competitive landscape characterized by both established industry giants and specialized service providers. Major competitors include Siemens Healthineers AG, GENERAL ELECTRIC, Koninklijke Philips N.V., Canon Inc., and Hitachi, Ltd., which leverage their extensive product portfolios and global presence to maintain market leadership. These OEMs compete alongside Independent Service Organizations (ISOs) such as Agility Health and Althea Group, which offer cost-effective alternatives and specialized expertise. The market is experiencing consolidation through strategic partnerships, mergers, and acquisitions as companies seek to expand their service capabilities and geographic reach. For instance, Carestream (Onex Corporation) has been active in strategic acquisitions to strengthen its service offerings. The competitive dynamics are shaped by the balance between OEM service dominance and the growing influence of ISOs, with competition intensifying around service quality, response times, pricing models, and the integration of digital solutions for remote monitoring and predictive maintenance.

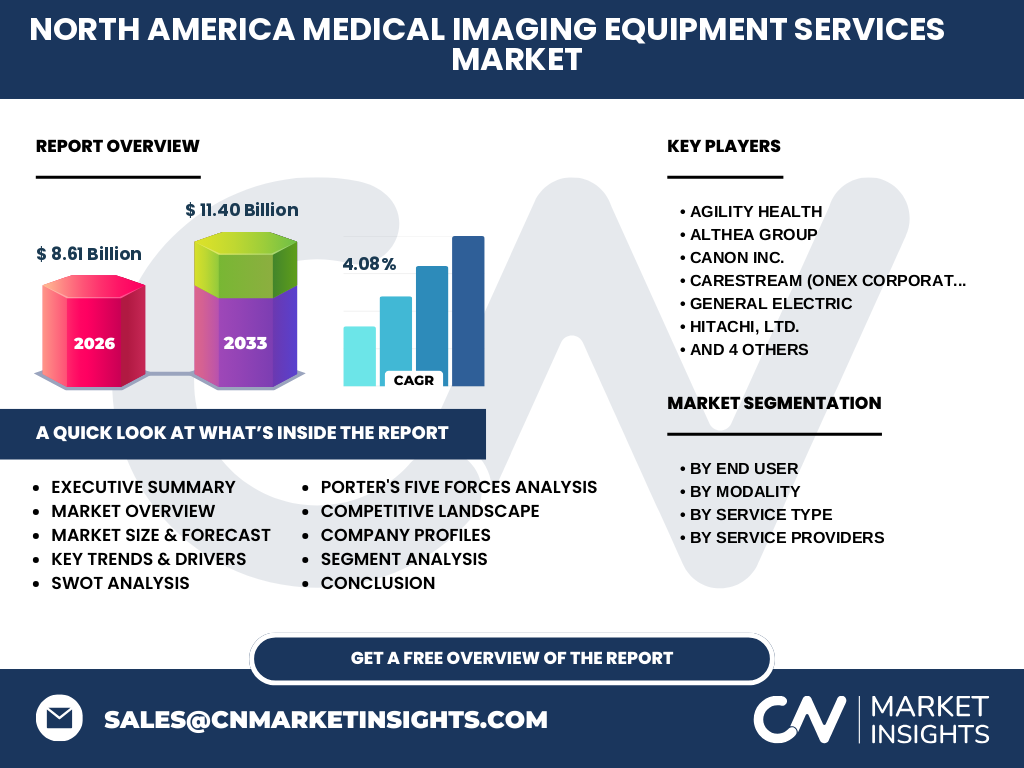

Executive Summary - High-level overview and key findings about North America Medical Imaging Equipment Services Market

The North America Medical Imaging Equipment Services Market is positioned for steady growth, with market size projected to reach $8.61 billion by 2026 and further expanding to $11.40 billion by 2033, reflecting a compound annual growth rate (CAGR) of 4.08% during the forecast period. The market is segmented by end-user (hospitals and diagnostic centers), modality (CT, MRI, Ultrasound, and X-Ray), service type (equipment repair and maintenance, refurbished systems, technical training, equipment removal and relocation, and software upgrades), and service providers (OEMs and ISOs). Key market drivers include the aging medical imaging equipment fleet, increasing demand for cost-effective maintenance solutions, and technological advancements in imaging systems. The competitive landscape features major players such as Siemens Healthineers AG, GENERAL ELECTRIC, and Koninklijke Philips N.V., alongside specialized ISOs. The market is characterized by trends toward predictive maintenance, refurbished equipment adoption, and digital service solutions, with the COVID-19 pandemic accelerating the shift toward remote monitoring and telemedicine support services.

North America Medical Imaging Equipment Services Market Forecast - Projections for 2025-2032 period

The North America Medical Imaging Equipment Services Market is forecasted to experience steady growth from 2025 to 2032, building on the projected market size of $8.61 billion in 2026 and reaching an estimated $11.40 billion by 2033. This growth trajectory represents a compound annual growth rate (CAGR) of 4.08%, indicating consistent market expansion over the forecast period. The forecast is driven by several factors including the continuous need for equipment maintenance and upgrades, the growing adoption of advanced imaging technologies, and the increasing focus on cost optimization in healthcare facilities. The service type segment, particularly equipment repair and maintenance, is expected to maintain strong demand, while the refurbished systems segment is projected to see accelerated growth due to budget constraints and sustainability initiatives. The modality segment, especially CT and MRI services, will continue to dominate due to their critical role in diagnostic procedures. The forecast also accounts for the ongoing digital transformation in healthcare, with increased demand for software upgrades and remote monitoring services shaping the market's future direction.

North America Medical Imaging Equipment Services Market Size and Share by Segmentation - Breakdown by {segmentData}

The North America Medical Imaging Equipment Services Market is segmented across multiple dimensions, with each segment contributing uniquely to the overall market size and share. By end-user, hospitals represent the largest segment due to their extensive imaging equipment infrastructure and higher service requirements, followed by diagnostic centers that are experiencing growing demand for specialized imaging services. In terms of modality, Computed Tomography (CT) and Magnetic Resonance Imaging (MRI) services command the largest market share, driven by their critical diagnostic applications and complex maintenance requirements, while Ultrasound and X-Ray services represent significant but smaller segments due to their relatively simpler service needs. The service type segmentation shows that equipment repair and maintenance services account for the largest share, reflecting the ongoing need to keep imaging equipment operational, followed by software upgrades and refurbished systems. By service providers, Original Equipment Manufacturers (OEMs) currently hold the largest market share due to their comprehensive service offerings and brand trust, though Independent Service Organizations (ISOs) are gaining market share through competitive pricing and specialized expertise.

Global North America Medical Imaging Equipment Services Market Size and Share by Region - Geographic distribution

The North America Medical Imaging Equipment Services Market exhibits distinct geographic distribution patterns across the United States, Canada, and Mexico, with the United States dominating the regional market share. The U.S. market benefits from the highest concentration of advanced healthcare facilities, substantial healthcare expenditure, and the largest installed base of medical imaging equipment, driving the majority of service demand. Canada represents the second-largest market, characterized by a well-established healthcare system and increasing adoption of advanced imaging technologies, though with a smaller overall market size compared to the U.S. Mexico, while having a smaller market share, is experiencing growing demand for medical imaging services due to healthcare infrastructure development and increasing medical tourism. The regional distribution is also influenced by population density, with urban centers showing higher service demand due to the concentration of healthcare facilities. Additionally, regional variations in healthcare policies, reimbursement structures, and technological adoption rates contribute to the differentiated market dynamics across North America.

Regional Analysis of the North America Medical Imaging Equipment Services Market - Detailed regional market performance

The North America Medical Imaging Equipment Services Market demonstrates varied performance across different regions, reflecting the diverse healthcare landscapes and economic conditions within the continent. In the United States, the market is characterized by high service demand driven by the extensive network of hospitals and diagnostic centers, particularly in major metropolitan areas such as the Northeast, West Coast, and Texas regions. The U.S. market benefits from advanced healthcare infrastructure, significant R&D investments, and the presence of major industry players, resulting in higher adoption rates of sophisticated service solutions. Canada's market performance is influenced by its universal healthcare system, with strong service demand in provinces with larger populations such as Ontario, Quebec, and British Columbia. The Canadian market shows a preference for cost-effective service solutions and preventive maintenance programs. Mexico's regional market is growing, with increased service demand in major cities like Mexico City, Monterrey, and Guadalajara, driven by healthcare modernization efforts and the expansion of private healthcare facilities. Regional performance variations are also shaped by factors such as regulatory environments, economic development levels, and the availability of skilled service technicians.

Leading Company Profiles in the North America Medical Imaging Equipment Services Market - Industry players and strategies

The North America Medical Imaging Equipment Services Market is led by several prominent companies, each employing distinct strategies to maintain and expand their market positions. Siemens Healthineers AG leverages its comprehensive portfolio of imaging equipment and integrated service solutions, focusing on digital transformation and predictive maintenance capabilities. GENERAL ELECTRIC emphasizes its extensive service network and innovative remote monitoring solutions, while Koninklijke Philips N.V. differentiates through its focus on value-based healthcare and integrated diagnostic solutions. Canon Inc. has strengthened its market presence through strategic acquisitions and a focus on advanced imaging technologies. Hitachi, Ltd. emphasizes its expertise in both equipment manufacturing and service delivery, offering comprehensive lifecycle management solutions. Hologic Inc. specializes in women's health imaging services, providing targeted expertise in mammography and other diagnostic modalities. Shimadzu Corporation focuses on precision engineering and high-quality service delivery, while Carestream (Onex Corporation) leverages its global presence and diverse service offerings. These companies employ strategies including strategic partnerships, service portfolio expansion, digital innovation, and geographic expansion to maintain competitive advantages in the market.

Porter's Five Forces Analysis of the North America Medical Imaging Equipment Services Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the North America Medical Imaging Equipment Services Market. The threat of new entrants is moderate due to the high capital requirements, need for specialized technical expertise, and established relationships between OEMs and healthcare facilities. However, ISOs continue to enter the market by offering cost-effective alternatives. The bargaining power of buyers (healthcare facilities) is significant, as they can choose between OEM and ISO services, negotiate service contracts, and demand high service quality and response times. The bargaining power of suppliers (equipment manufacturers) remains strong, particularly for OEMs who control proprietary technology and spare parts, though this is somewhat mitigated by the growing presence of ISOs who can source alternative components. The threat of substitute products or services is low, as medical imaging equipment requires specialized maintenance that cannot be easily replaced. Competitive rivalry is intense, characterized by price competition, service quality differentiation, and the battle for market share between OEMs and ISOs. The market also experiences pressure from technological advancements that can disrupt traditional service models and create new competitive dynamics.

SWOT Analysis of the North America Medical Imaging Equipment Services Market - Strengths, weaknesses, opportunities, threats

The North America Medical Imaging Equipment Services Market exhibits distinct strengths, weaknesses, opportunities, and threats that shape its competitive landscape. Strengths include the advanced healthcare infrastructure in North America, the presence of major industry players with extensive service networks, and the high adoption rate of sophisticated imaging technologies. The market also benefits from strong regulatory frameworks that ensure service quality and patient safety. However, weaknesses exist in the form of high service costs, the shortage of skilled technicians, and the complexity of modern imaging systems that require specialized expertise. Opportunities abound in the growing demand for predictive maintenance and remote monitoring solutions, the expansion of refurbished equipment services, and the increasing focus on preventive maintenance programs. The market can also capitalize on the digital transformation of healthcare services and the integration of artificial intelligence for service optimization. Threats include intense price competition, the rapid pace of technological change that can render service capabilities obsolete, potential economic downturns affecting healthcare budgets, and the risk of cybersecurity vulnerabilities in connected imaging systems. Additionally, regulatory changes and reimbursement challenges pose ongoing threats to market stability.

North America Medical Imaging Equipment Services Market Value Chain Analysis - Industry structure and value flow

The North America Medical Imaging Equipment Services Market value chain encompasses multiple interconnected stages that create and deliver value to end-users. The chain begins with equipment manufacturers who design and produce imaging systems, followed by distributors and suppliers who facilitate the flow of equipment and spare parts to healthcare facilities. Service providers, including both OEMs and ISOs, form the core of the value chain by offering maintenance, repair, and upgrade services. Technical training providers contribute by developing skilled technicians capable of servicing complex imaging equipment. Software developers create diagnostic and monitoring solutions that enhance service capabilities. Healthcare facilities, including hospitals and diagnostic centers, represent the primary customers who consume these services to maintain operational imaging equipment. The value chain also includes regulatory bodies that ensure service quality and safety standards, as well as insurance companies that influence service adoption through reimbursement policies. Value flows through this chain via service contracts, maintenance agreements, and technology transfers, with each participant adding value through specialized expertise, technological innovation, or operational efficiency. The integration of digital technologies is increasingly connecting different value chain participants, enabling more efficient service delivery and enhanced customer experiences.

Key Investment Insights in the North America Medical Imaging Equipment Services Market - Strategic investment recommendations

The North America Medical Imaging Equipment Services Market presents several compelling investment opportunities for stakeholders seeking to capitalize on market growth. Strategic investments in digital transformation technologies, particularly predictive maintenance platforms and remote monitoring solutions, offer significant potential as healthcare facilities increasingly demand proactive service approaches. Investments in training and development programs to address the skilled technician shortage represent another strategic opportunity, as the complexity of modern imaging systems requires specialized expertise. The growing refurbished equipment market presents investment potential in refurbishment facilities, quality certification processes, and distribution networks. Investors should also consider opportunities in software development for imaging system optimization, cybersecurity solutions for connected medical devices, and integrated service platforms that combine multiple service offerings. Strategic partnerships between OEMs and ISOs represent another investment avenue, as collaboration can create comprehensive service solutions that leverage both manufacturer expertise and independent flexibility. Additionally, investments in geographic expansion, particularly in underserved regions, and the development of specialized service offerings for emerging imaging modalities can provide competitive advantages. The market's steady growth trajectory and the essential nature of medical imaging services make it an attractive long-term investment opportunity with multiple entry points for strategic capital deployment.

North America Medical Imaging Equipment Services Market Conclusion - Summary and key takeaways

The North America Medical Imaging Equipment Services Market represents a critical and growing segment of the healthcare industry, driven by the essential need to maintain and optimize medical imaging equipment across hospitals and diagnostic centers. With a projected market size of $8.61 billion by 2026 and $11.40 billion by 2033, growing at a CAGR of 4.08%, the market demonstrates steady expansion fueled by technological advancements, aging equipment fleets, and the increasing complexity of imaging systems. The market is characterized by a diverse service landscape encompassing equipment repair and maintenance, refurbished systems, technical training, equipment removal and relocation, and software upgrades, delivered through both OEM and ISO service providers. Key trends include the shift toward predictive maintenance, the growing adoption of refurbished equipment, and the integration of digital solutions for remote monitoring and service optimization. While facing challenges such as high service costs and skilled technician shortages, the market presents significant opportunities in digital transformation, preventive maintenance programs, and strategic partnerships. The COVID-19 pandemic has accelerated certain trends while highlighting the essential nature of reliable imaging services in healthcare delivery. Overall, the market's essential role in healthcare infrastructure, combined with its steady growth trajectory, positions it as a resilient and strategically important segment within the broader healthcare services industry.

Research Methodology - How this research was conducted

The research for the North America Medical Imaging Equipment Services Market was conducted using a comprehensive and rigorous methodology that combines multiple data collection and analysis approaches. Primary research involved interviews with key industry stakeholders including service providers, healthcare facility administrators, equipment manufacturers, and industry experts to gather firsthand insights on market dynamics, service trends, and competitive strategies. Secondary research encompassed extensive review of industry reports, company financial statements, regulatory filings, trade publications, and market databases to validate and supplement primary findings. The research methodology employed both top-down and bottom-up approaches to estimate market size and forecast growth, triangulating data from multiple sources to ensure accuracy. Market segmentation analysis was conducted based on end-user categories, imaging modalities, service types, and service provider classifications, with each segment analyzed for growth potential and market share. Competitive landscape analysis included detailed profiling of major market players, assessment of their service portfolios, strategic initiatives, and market positioning. The research also incorporated Porter's Five Forces analysis and SWOT analysis to provide comprehensive market insights. Data validation processes included cross-referencing with industry benchmarks and expert consultations to ensure the reliability of market projections and trend analyses.

Research Scope - Coverage and limitations

The research scope for the North America Medical Imaging Equipment Services Market encompasses a comprehensive analysis of the market across the United States, Canada, and Mexico, focusing on the period from 2025 to 2033 with historical context provided for trend analysis. The scope includes detailed coverage of all major imaging modalities (CT, MRI, Ultrasound, and X-Ray), service types (equipment repair and maintenance, refurbished systems, technical training, equipment removal and relocation, and software upgrades), and service provider categories (OEMs and ISOs). The research examines market dynamics including drivers, restraints, challenges, and opportunities, along with competitive landscape analysis featuring key industry players. The scope also includes regional analysis, value chain assessment, and strategic investment insights. However, the research has certain limitations, including the exclusion of certain emerging imaging technologies that are still in early adoption phases, limited granular data availability for certain sub-segments, and the inherent challenges in forecasting long-term market trends in a rapidly evolving technological landscape. Additionally, the research focuses primarily on commercial service aspects and does not extensively cover in-house service operations within large healthcare systems or academic medical centers. Currency fluctuations, regulatory changes, and unexpected market disruptions (such as future pandemics) are also factors that could impact actual market performance beyond the scope of this research.

Key Companies and Recent Developments in the North America Medical Imaging Equipment Services Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The North America Medical Imaging Equipment Services Market features several key companies that have recently announced significant developments shaping the industry landscape. Siemens Healthineers AG has expanded its remote monitoring capabilities through strategic partnerships with cloud service providers, enhancing its predictive maintenance offerings. GENERAL ELECTRIC has launched new integrated service platforms that combine equipment monitoring with AI-driven diagnostics, while also announcing strategic acquisitions to strengthen its service network in underserved regions. Koninklijke Philips N.V. has introduced innovative service contracts that bundle multiple imaging modalities under unified maintenance agreements, along with partnerships with healthcare IT companies to enhance digital service delivery. Canon Inc. has announced the expansion of its refurbished equipment program with enhanced quality certification processes, targeting cost-conscious healthcare facilities. Hitachi, Ltd. has launched new technical training programs in collaboration with educational institutions to address the skilled technician shortage, while also introducing advanced remote support tools. Hologic Inc. has expanded its women's health imaging service portfolio through strategic partnerships with diagnostic centers, enhancing its specialized service offerings. Shimadzu Corporation has announced new software upgrade packages for its imaging systems, focusing on enhanced image processing capabilities. Carestream (Onex Corporation) has strengthened its market position through strategic acquisitions of regional service providers, expanding its geographic coverage and service capabilities across North America.