What is the US Dairy Free Creamer Market Overview – definition, scope, and significance?

The US Dairy Free Creamer Market comprises non‑dairy coffee and tea creamer products that are formulated without milk‑derived ingredients. The market includes both powder and liquid formats, a variety of flavors such as Original, French Vanilla, Chocolate, Coconut, and Hazelnut, and caters to organic as well as conventional consumer preferences. Its significance stems from the growing demand for plant‑based alternatives driven by health consciousness, lactose intolerance, vegan lifestyles, and sustainability concerns, positioning the sector as a key pillar of the broader non‑dairy beverage industry.

What are the main drivers, restraints, challenges, and opportunities in the US Dairy Free Creamer Market?

Key drivers include rising consumer awareness of dairy‑related allergens, an expanding vegan population, and the premium placed on clean‑label and organic products. Restraints involve higher production costs for specialty ingredients and occasional supply chain disruptions for raw materials like almonds and coconuts. Challenges revolve around intense competition from traditional dairy creamer brands launching plant‑based lines and the need for consistent taste profiles. Opportunities arise from product innovation (e.g., functional additives, high‑protein blends), expansion into food‑service channels, and leveraging e‑commerce platforms for direct‑to‑consumer growth.

What are the current growth trends shaping the US Dairy Free Creamer Market?

Trend analysis shows a steady shift toward liquid formulations, which are perceived as more convenient for on‑the‑go consumption. Flavor diversification, especially the introduction of exotic options like Hazelnut and Coconut, is attracting adventurous consumers. The organic segment is gaining momentum, reflecting a broader clean‑label movement. Additionally, co‑branding with coffee chains and the emergence of “ready‑to‑drink” (RTD) creamer beverages are creating new consumption occasions beyond the traditional kitchen setting.

How did COVID‑19 impact the US Dairy Free Creamer Market and what is the recovery trajectory?

The pandemic accelerated home‑brewing habits, leading to a surge in demand for dairy‑free creamer powders as consumers stocked pantry items. Supply chain resilience was tested, yet most manufacturers adapted by increasing production capacity. As the economy rebounds, the market is transitioning from pandemic‑driven pantry buying to sustained growth fueled by lifestyle choices, with a projected CAGR of 3.76% indicating a robust post‑COVID recovery.

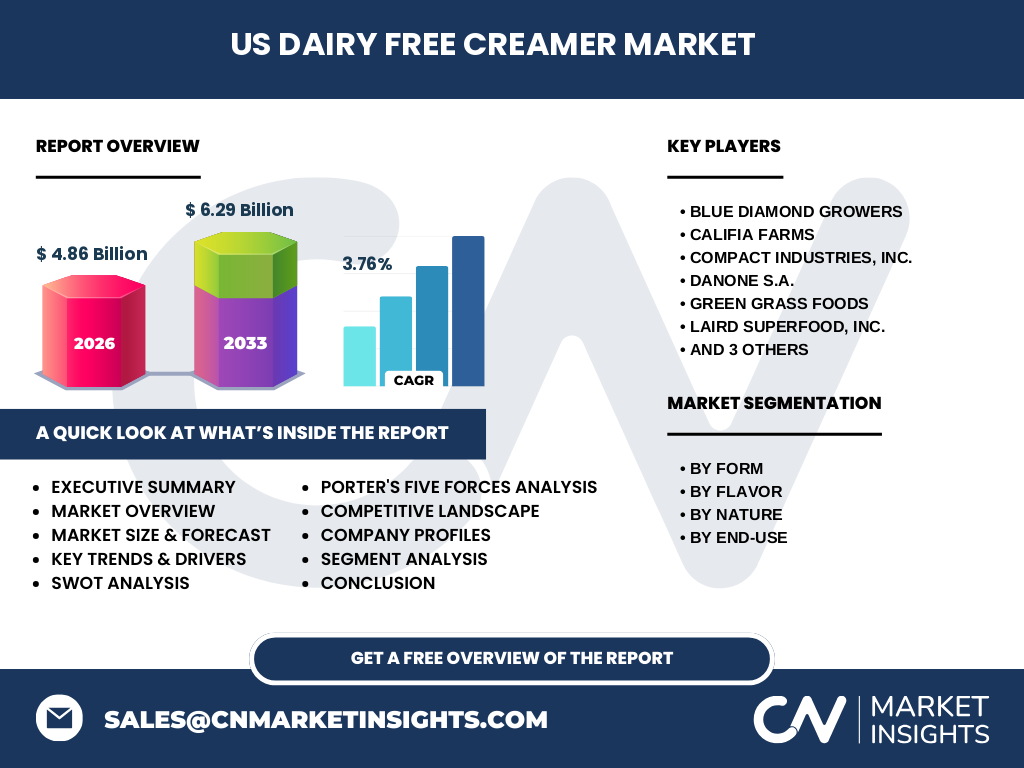

Who are the major competitors and what is the level of market consolidation in the US Dairy Free Creamer Market?

The competitive landscape is characterized by a mix of established dairy giants entering the plant‑based space and dedicated non‑dairy innovators. Leading players include Blue Diamond Growers, Califia Farms, Compact Industries, Danone S.A., Green Grass Foods, Laird Superfood, Inc., Mooala Brands, LLC., Nestlé, and milkadamia. While the market remains fragmented, recent strategic partnerships and acquisitions suggest a moderate consolidation trend, as larger firms seek to broaden their plant‑based portfolios.

What are the key takeaways in the Executive Summary of the US Dairy Free Creamer Market?

The US Dairy Free Creamer Market is valued at $4.86 billion in 2026 and is forecast to reach $6.29 billion by 2033, reflecting a 3.76% CAGR. Growth is underpinned by health‑centric consumer preferences, flavor innovation, and expanding distribution channels. Organic and liquid formats present the highest upside, while competitive pressure is intensifying. Investment in product differentiation and supply‑chain robustness will be critical for market leaders.

What are the forecast projections for the US Dairy Free Creamer Market from 2025 to 2032?

Based on the provided CAGR of 3.76%, the market is expected to continue expanding steadily throughout 2025‑2032. By 2027 the market size will approximate $5.27 billion, reaching the forecasted $6.29 billion by 2033. The upward trajectory indicates consistent consumer adoption and the success of emerging product lines, particularly within the organic and liquid segments.

How is the US Dairy Free Creamer Market sized and shared by segmentation?

Segmentation by form shows powder and liquid formats competing for market share, with liquid gaining traction due to convenience. Flavor segmentation highlights Original and French Vanilla as core favorites, while niche flavors such as Coconut and Hazelnut are capturing premium segments. The nature segment distinguishes between organic (driven by clean‑label demand) and conventional products. End‑use categories demonstrate that Food and Beverage Processing, Bakery Products and Ice Creams, RTD Beverages, and Infant Food Prepared and Packaged Food each contribute to the overall market, with food‑service applications experiencing the fastest growth.

What is the geographic distribution of the US Dairy Free Creamer Market by region?

The market is primarily United States‑centric, with regional performance driven by varying consumer attitudes toward plant‑based nutrition. Coastal states exhibit higher per‑capita consumption due to stronger vegan communities, while the Midwest shows steady adoption thanks to growing awareness of lactose intolerance. Overall, the US market dominates the global landscape for dairy‑free creamer products.

What does the regional analysis reveal about performance within the US Dairy Free Creamer Market?

In the Northeast, premium organic and flavored variants command a larger share, reflecting higher disposable income. The South demonstrates strong growth in powder formats, aligning with price‑sensitive purchasing behavior. The West leads in liquid and functional formulations, supported by tech‑savvy consumers and a dense network of specialty retailers. These regional nuances guide targeted marketing and distribution strategies.

Which companies lead the US Dairy Free Creamer Market and what are their core strategies?

Blue Diamond Growers leverages its almond expertise to expand almond‑based liquid creamer lines. Califia Farms focuses on brand storytelling around sustainability and offers a broad flavor portfolio. Danone S.A. integrates dairy‑free creamer offerings into its broader plant‑based product ecosystem. Laird Superfood, Inc. emphasizes functional ingredients like MCT oil. Nestlé utilizes its extensive distribution network to introduce dairy‑free versions of legacy creamer brands. Each leader invests in product innovation, strategic partnerships, and channel diversification.

How does Porter’s Five Forces analysis apply to the US Dairy Free Creamer Market?

Threat of new entrants remains moderate due to capital requirements for ingredient sourcing and brand building. Supplier power is relatively high, as specialty nuts and plant oils are concentrated among few growers. Buyer power is growing, with retailers demanding diverse SKUs and competitive pricing. Substitutes include traditional dairy creamers and other plant‑based milks, intensifying competition. Rivalry among existing firms is strong, driven by rapid product launches and marketing spend.

What are the SWOT insights for the US Dairy Free Creamer Market?

Strengths: Strong consumer trend toward plant‑based diets, diverse flavor options, and expanding retail presence.

Weaknesses: Higher raw‑material costs and occasional supply volatility.

Opportunities: Expansion into institutional food‑service, functional ingredient blends, and sustained growth of organic segments.

Threats: Intensifying competition from both dairy and non‑dairy players, and potential regulatory scrutiny over labeling claims.

What does the value chain of the US Dairy Free Creamer Market look like?

The value chain begins with raw‑material sourcing (almonds, coconuts, soy, oat, hazelnuts), followed by processing (grinding, emulsification, flavor addition), formulation (powder vs. liquid), packaging, distribution to retail and food‑service channels, and finally end‑consumer purchase. Key value‑adding steps include proprietary blending technology and flavor development, which differentiate premium brands.

What key investment insights can be drawn for stakeholders in the US Dairy Free Creamer Market?

Investors should prioritize companies with strong organic portfolios and scalable liquid production lines. Strategic acquisition of niche flavor innovators can accelerate market share gains. Funding supply‑chain resilience—especially in almond and coconut sourcing—will safeguard margins. Finally, allocating capital to e‑commerce and direct‑to‑consumer initiatives can capture growth from digitally native consumers.

What conclusions can be drawn about the US Dairy Free Creamer Market?

The market is on a clear growth path, supported by health, ethical, and convenience drivers. While competition is fierce, differentiation through flavor, organic certification, and functional benefits provides clear pathways to capture market share. The forecasted increase to $6.29 billion by 2033 underscores a resilient and expanding opportunity landscape for both incumbents and new entrants.

How was the research for this report conducted?

The methodology combined primary interviews with industry executives, secondary data analysis from company filings, market databases, and trade publications. Trend extrapolation employed the provided CAGR of 3.76% to model future market size. Segmentation insights were derived from product catalogs and retailer assortments, while competitive mapping used public announcements and partnership disclosures.

What is the scope of the research and its limitations?

The scope covers the US Dairy Free Creamer Market from 2025 to 2033, focusing on product form, flavor, nature, and end‑use segments. It includes major manufacturers and regional performance within the United States. Limitations are confined to the data provided; the analysis does not incorporate external financial figures, market share percentages, or regional breakdowns beyond what was supplied.

Which key companies have recent developments in the US Dairy Free Creamer Market?

Blue Diamond Growers launched a new almond‑based liquid creamer with added calcium. Califia Farms introduced a limited‑edition Hazelnut flavor targeting the premium segment. Danone S.A. announced a partnership with a plant‑protein supplier to enhance protein content in its dairy‑free creamer line. Laird Superfood, Inc. released a functional MCT‑enriched coconut creamer. Nestlé expanded its distribution of dairy‑free creamer pods across major US retailers. These developments illustrate active innovation and market expansion.