North America Cancer Tissue Diagnostics Market Overview - Definition, scope, and significance?

The North America Cancer Tissue Diagnostics market encompasses the development, production, and distribution of diagnostic tests that analyze cancerous tissue specimens to provide critical information on tumor type, grade, and molecular characteristics. The scope includes immunohistochemical (IHC) tests and in‑situ hybridization (ISH) assays used by pathology labs, hospitals, and research institutions to guide personalized treatment decisions, assess prognosis, and support clinical trial enrollment. This market is significant because accurate tissue diagnostics enable targeted therapies, improve patient outcomes, and reduce unnecessary treatment costs, positioning the region as a global leader in precision oncology.

North America Cancer Tissue Diagnostics Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising cancer incidence, expanding use of targeted therapies, and increasing reimbursement for molecular testing. Strong academic‑clinical networks and high adoption of advanced IHC and ISH platforms further accelerate growth. Restraints stem from high test costs, complex regulatory pathways, and limited awareness in smaller community hospitals. Challenges involve integrating diagnostic data with electronic health records and managing reimbursement variability across payers. Opportunities arise from emerging biomarkers, AI‑enabled image analysis, and partnerships that expand access to next‑generation tissue assays.

North America Cancer Tissue Diagnostics Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a shift from conventional histopathology toward multiplexed IHC panels that assess multiple proteins simultaneously, improving diagnostic efficiency. There is also rapid adoption of RNA‑based ISH technologies for detecting gene fusions and transcripts. Emerging trends include digital pathology platforms coupled with machine‑learning algorithms that automate slide interpretation, and the development of companion diagnostics linked to newly approved oncology drugs. Investment in automation and high‑throughput platforms is reshaping laboratory workflows across the region.

COVID-19 Impact on the North America Cancer Tissue Diagnostics Market - Pandemic effects and recovery trajectory?

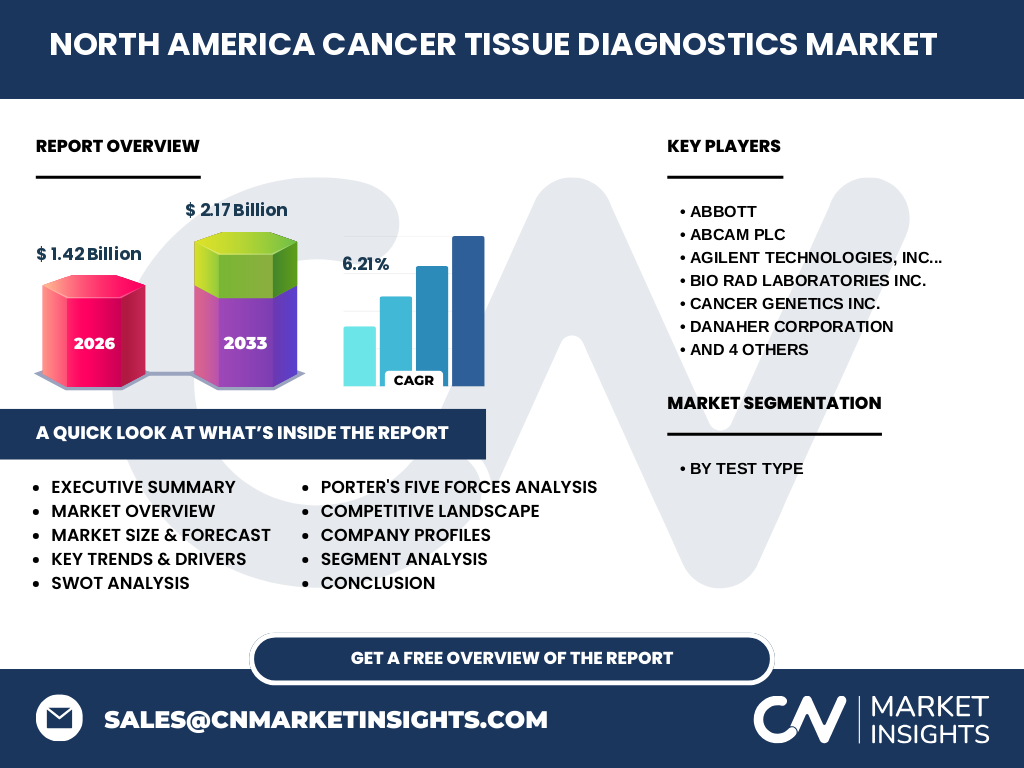

The COVID‑19 pandemic initially disrupted elective procedures and reduced biopsy volumes, causing a temporary dip in test volumes. However, the subsequent acceleration of tele‑health and remote pathology services helped mitigate the impact. Laboratories quickly adopted digital slide sharing, preserving continuity of cancer diagnostics. As oncology care normalized in 2021, demand rebounded strongly, contributing to the market’s projected CAGR of 6.21% and a forecasted size of $2.17 billion by 2033.

North America Cancer Tissue Diagnostics Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena is dominated by established life‑science giants and specialist diagnostics firms. Major players include Abbott, Abcam plc, Agilent Technologies, Bio‑Rad Laboratories, Cancer Genetics Inc., Danaher Corporation, Enzo Life Sciences, F. Hoffmann‑La Roche Ltd, Merck KGaA (Sigma‑Aldrich), and Thermo Fisher Scientific. Recent years have seen strategic acquisitions—such as Danaher’s purchase of a niche IHC developer—and collaborative agreements that broaden product portfolios, reflecting a moderate level of consolidation aimed at enhancing assay breadth and distribution reach.

Executive Summary - High-level overview and key findings about North America Cancer Tissue Diagnostics Market?

The North America Cancer Tissue Diagnostics market was valued at $1.42 billion in 2026 and is projected to reach $2.17 billion by 2033, growing at a CAGR of 6.21%. Growth is driven by rising cancer prevalence, increasing reliance on precision medicine, and robust reimbursement frameworks. IHC and ISH tests together form the core segment, with digital pathology and AI emerging as transformative forces. Competitive dynamics are shaped by a mix of large multinationals and niche innovators, with consolidation through acquisitions and partnerships intensifying. Despite cost and regulatory hurdles, the market presents strong upside for investors focusing on innovative assay technologies.

North America Cancer Tissue Diagnostics Market Forecast - Projections for 2025-2032 period?

Building on the 2026 baseline of $1.42 billion, the market is expected to expand steadily, reaching approximately $2.00 billion by 2029 and $2.17 billion by 2033. The compound annual growth rate of 6.21% reflects continued adoption of multiplexed IHC panels, RNA‑ISH assays, and digital pathology solutions. Growth will be supported by expanding indications for companion diagnostics and increasing coverage from public and private insurers across the United States and Canada.

North America Cancer Tissue Diagnostics Market Size and Share by Segmentation - Breakdown by Test Type?

The market is segmented primarily by test type: Immunohistochemical (IHC) Tests and In‑Situ Hybridization (ISH) Tests. IHC tests account for the larger share due to their broad application in protein expression profiling and routine pathology workflows. ISH tests, while smaller in volume, are gaining traction for detecting gene rearrangements and copy‑number variations, especially as targeted therapies become more prevalent. Both segments are expected to grow in line with overall market momentum, with IHC maintaining dominance and ISH accelerating faster due to emerging biomarker demands.

Global North America Cancer Tissue Diagnostics Market Size and Share by Region - Geographic distribution?

Within the global landscape, North America holds a leading position, contributing the majority of worldwide revenue for cancer tissue diagnostics. The United States, as the largest healthcare market, drives most of the $1.42 billion valuation, while Canada adds a notable but smaller share. The region’s advanced healthcare infrastructure, high R&D investment, and strong payer support underpin its dominant share relative to other continents.

Regional Analysis of the North America Cancer Tissue Diagnostics Market - Detailed regional market performance?

The United States accounts for the bulk of market activity, powered by a large network of academic medical centers, commercial pathology labs, and an extensive oncology drug pipeline. Strong reimbursement policies from Medicare and private insurers encourage test utilization. Canada, while smaller, benefits from a publicly funded system that increasingly reimburses advanced tissue diagnostics, especially for guideline‑directed therapies. Both countries exhibit steady growth, though the U.S. market shows faster uptake of digital pathology and AI solutions due to higher capital availability.

Leading Company Profiles in the North America Cancer Tissue Diagnostics Market - Industry players and strategies?

Abbott focuses on expanding its IHC reagent portfolio and leveraging its diagnostics distribution network. Abcam plc emphasizes high‑quality antibodies for research‑to‑clinical translation. Agilent Technologies invests in multiplexed ISH platforms and automation. Bio‑Rad Laboratories offers integrated IHC‑ISH workflows targeting academic labs. Cancer Genetics Inc. specializes in rare‑cancer biomarker panels. Danaher’s strategy centers on acquiring niche assay developers to broaden its diagnostic suite. Enzo Life Sciences provides specialty reagents for emerging targets. Roche and Merck KGaA (Sigma‑Aldrich) leverage global drug pipelines to create companion diagnostics. Thermo Fisher Scientific integrates high‑throughput staining instruments with reagent kits, promoting end‑to‑end solutions.

Porter's Five Forces Analysis of the North America Cancer Tissue Diagnostics Market - Competitive forces assessment?

Threat of New Entrants: Moderate. High R&D costs, stringent FDA regulations, and established distribution channels create barriers, but niche biotech startups can enter with innovative biomarker assays. Bargaining Power of Suppliers: Low to moderate; raw material suppliers are numerous, though specialty antibodies can be scarce, giving some power to key reagent manufacturers. Bargaining Power of Buyers: High. Large hospital systems and pathology groups negotiate pricing, and reimbursement pressures drive cost sensitivity. Threat of Substitutes: Low. Alternative diagnostic modalities (e.g., liquid biopsies) complement rather than replace tissue testing. Competitive Rivalry: High. Numerous global players compete on assay sensitivity, automation, and companion‑diagnostic alignment, leading to frequent product launches and strategic partnerships.

SWOT Analysis of the North America Cancer Tissue Diagnostics Market - Strengths, weaknesses, opportunities, threats?

Strengths: Robust healthcare spending, advanced R&D ecosystem, and strong payer support for precision diagnostics. Weaknesses: High per‑test cost, complex regulatory submissions, and fragmented adoption across smaller labs. Opportunities: Expansion of multiplexed IHC/ISH panels, integration of AI‑driven digital pathology, and growth of companion diagnostics linked to emerging oncology drugs. Threats: Potential reimbursement cuts, competitive pressure from liquid biopsy technologies, and supply chain vulnerabilities for specialty antibodies.

North America Cancer Tissue Diagnostics Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with research & development, where biotech firms discover biomarkers and design assay formats. Next, raw material suppliers provide antibodies, probes, and reagents. Manufacturing converts these inputs into kits and automated instruments. Distribution channels—wholesale distributors and direct sales teams—deliver products to hospitals, reference labs, and research institutions. End‑users (pathologists, oncologists) perform testing, generate diagnostic reports, and feed data back to drug developers and payers, completing a feedback loop that informs further assay refinement.

Key Investment Insights in the North America Cancer Tissue Diagnostics Market - Strategic investment recommendations?

Investors should target companies that combine robust IHC/ISH portfolios with digital pathology capabilities, as integration accelerates workflow efficiency and data analytics value. Partnerships with pharmaceutical firms developing targeted therapies provide a pipeline of companion‑diagnostic opportunities. Additionally, firms that secure reimbursement codes for emerging multiplexed assays are well‑positioned for sustainable revenue growth. Given the 6.21% CAGR, allocating capital to innovators in AI‑enabled image analysis and to niche players acquiring specialty biomarkers can yield attractive returns.

North America Cancer Tissue Diagnostics Market Conclusion - Summary and key takeaways?

The North America Cancer Tissue Diagnostics market is on a clear growth trajectory, moving from $1.42 billion in 2026 to an anticipated $2.17 billion by 2033. Core drivers include rising cancer prevalence, the expanding role of precision medicine, and supportive reimbursement environments. IHC remains the dominant test type, while ISH is rapidly gaining relevance. Competitive activity centers on large life‑science corporations and specialized assay developers, with consolidation through acquisitions and alliances sharpening the landscape. Digital transformation and AI represent the next wave of differentiation, offering investors and stakeholders clear pathways for value creation.

Research Methodology - How this research was conducted?

The study combined primary interviews with key opinion leaders in pathology, oncology, and health‑technology procurement, alongside secondary analysis of regulatory filings, payer policy documents, and corporate financial reports. Market sizing employed a top‑down approach using known North American healthcare expenditure on oncology diagnostics, refined by bottom‑up validation through vendor shipment data. Forecasting applied a compound annual growth rate of 6.21% derived from historical trends and forward‑looking adoption rates of IHC and ISH technologies.

Research Scope - Coverage and limitations?

The scope covers the North American region (United States and Canada) and focuses exclusively on tissue‑based diagnostic tests—specifically immunohistochemical and in‑situ hybridization assays. The analysis excludes liquid biopsy, imaging diagnostics, and non‑tissue molecular testing. While the study leverages the latest available data up to 2026, rapid regulatory changes or unforeseen payer policy shifts may affect future market dynamics.

Key Companies and Recent Developments in the North America Cancer Tissue Diagnostics Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Abbott announced the launch of a next‑generation IHC staining system that reduces turnaround time by 30 %. Abcam plc introduced a new line of validated antibodies targeting rare oncogenic drivers, positioning them for companion‑diagnostic use. Agilent Technologies partnered with a leading digital pathology firm to integrate AI‑based image analysis with its ISH platforms. Bio‑Rad released an automated IHC‑ISH workflow that consolidates staining and scanning in a single instrument. Cancer Genetics Inc. secured FDA clearance for a multiplexed gene‑fusion panel focused on pediatric sarcomas. Danaher completed the acquisition of a boutique ISH reagent company, expanding its biomarker portfolio. Enzo Life Sciences entered a licensing agreement with a biotech startup to co‑develop antibody reagents for novel checkpoint inhibitors. Roche announced a co‑development deal with a pharma partner to align its IHC assays with an upcoming tyrosine‑kinase inhibitor. Merck KGaA (Sigma‑Aldrich) launched a set of high‑affinity probes for RNA‑ISH applications. Thermo Fisher introduced a high‑throughput IHC automation platform designed for large reference laboratories, emphasizing integration with its cloud‑based data management suite.