1. What is the Asia Pacific Analog-to-Digital Converter Market Overview – definition, scope, and significance?

The Asia Pacific Analog-to-Digital Converter (ADC) market comprises companies that design, manufacture, and supply ADC chips used to convert analog signals into digital data across a variety of applications. Scope includes all ADC product types—integrating, delta‑sigma, successive approximation, and ramp ADCs—served to industries such as industrial automation, consumer electronics, automotive, healthcare, and telecommunications. The region’s significance stems from its rapid digitisation, high‑tech manufacturing ecosystems in China, Japan, South Korea, and Taiwan, and the escalating demand for high‑resolution, low‑power converters that enable IoT, 5G, advanced driver‑assistance systems (ADAS), and medical imaging.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Asia Pacific ADC market?

Drivers include strong growth in consumer electronics (smartphones, wearables), expanding automotive electronics (electric vehicles and ADAS), and increasing industrial automation. Government initiatives supporting semiconductor self‑reliance in China, Japan, and South Korea further accelerate investment. Restraints involve supply‑chain volatility for silicon wafers and rising raw‑material costs. Challenges are intense price competition and the need for ultra‑low power designs for battery‑operated devices. Opportunities arise from emerging 6G and AI‑edge workloads that demand higher‑resolution (12‑bit to 16‑bit) converters, and from medical‑device growth requiring precise analog capture.

3. What are the current and emerging growth trends in the Asia Pacific ADC market?

Current trends highlight a shift toward higher‑resolution (14‑bit and 16‑bit) ADCs for automotive radar and LiDAR, and the adoption of delta‑sigma architectures for low‑noise audio and biomedical signals. Emerging trends include the integration of ADCs with digital signal processors (DSPs) on a single die to reduce latency, and the use of silicon‑photonic technologies for ultra‑high‑speed data converters targeting 5G/6G front‑ends. Companies are also exploring heterogeneous integration to combine multiple ADC types on a common substrate, catering to multi‑function IoT devices.

4. How has COVID‑19 impacted the Asia Pacific ADC market and what is the recovery trajectory?

The pandemic initially disrupted supply chains, causing short‑term shortages of silicon wafers and delaying fab expansions. However, strong demand for remote‑work devices, tele‑health equipment, and accelerated digital transformation mitigated the impact. Post‑2022, the market has shown a robust rebound, with demand outpacing pre‑pandemic levels, especially in consumer electronics and automotive infotainment. Recovery is expected to continue steadily as governments maintain stimulus for semiconductor manufacturing.

5. Who are the major competitors and what is the competitive landscape in the Asia Pacific ADC market?

The competitive landscape is dominated by a mix of global leaders and regional specialists. Key players include Analog Devices Inc., Texas Instruments Incorporated, and Maxim Integrated, Inc., which leverage extensive product portfolios and strong R&D pipelines. Regional champions such as Asahi Kasei Microdevices Corporation, Renesas Electronics Corporation, and Rohm Co., Ltd. focus on cost‑effective, high‑volume solutions. Market consolidation is modest, with strategic alliances and joint ventures—particularly between Japanese firms and Chinese foundries—aimed at securing manufacturing capacity.

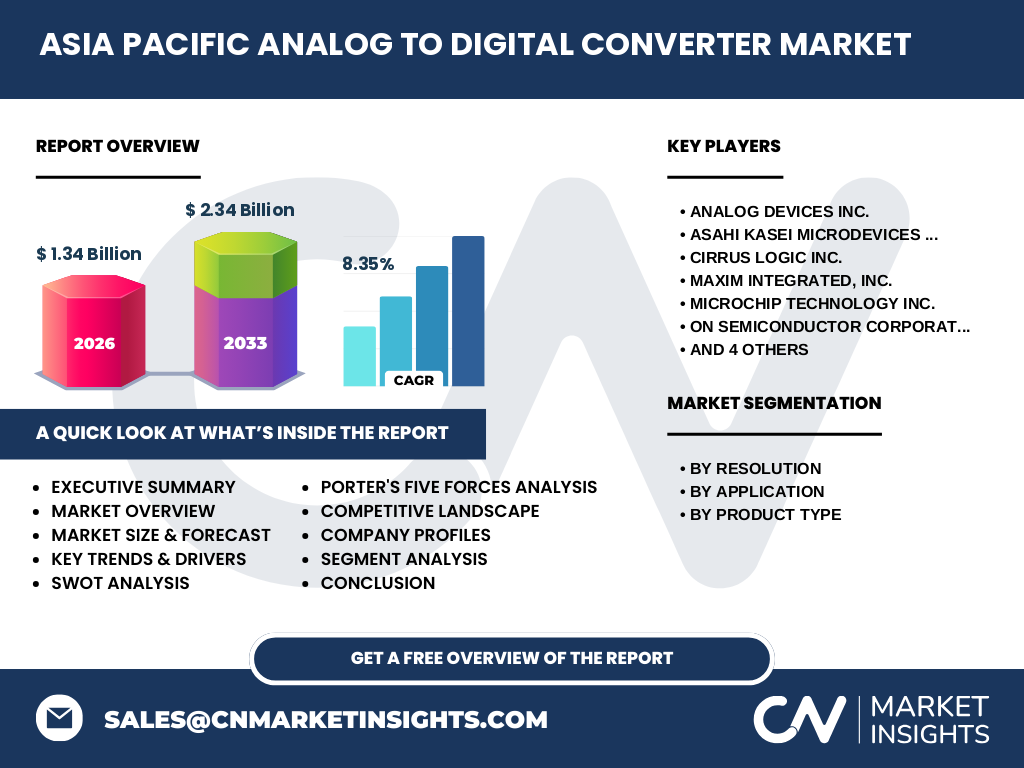

6. What are the high‑level findings in the executive summary of the Asia Pacific ADC market?

The Asia Pacific ADC market is projected to reach USD 2.34 billion by 2033, growing from USD 1.34 billion in 2026 at a CAGR of 8.35 %. Growth is propelled by expanding automotive electronics, consumer‑device proliferation, and rising industrial automation. Higher‑resolution and low‑power ADCs are gaining market share, while supply‑chain resilience and regional fab investments are critical success factors. The market remains attractive for investors seeking exposure to the broader semiconductor boom in the region.

7. What are the forecast projections for the Asia Pacific ADC market from 2025 to 2032?

Based on the provided CAGR of 8.35 %, the market is expected to expand steadily each year, crossing the USD 2 billion mark by the early 2030s and reaching USD 2.34 billion by 2033. The forecast reflects continued demand across all application segments, with the fastest growth anticipated in automotive (electric‑vehicle powertrains and ADAS) and healthcare (portable diagnostic devices). The projection also assumes successful rollout of new fab capacity and incremental technology upgrades in ADC architectures.

8. How is the market size and share segmented by resolution, application, and product type?

Resolution: The market includes 8‑bit, 10‑bit, 12‑bit, 14‑bit, and 16‑bit ADCs. Higher‑resolution (14‑bit and 16‑bit) units are gaining traction in automotive radar and medical imaging, while 8‑bit and 10‑bit devices dominate cost‑sensitive consumer electronics. Application: Industrial, consumer electronics, automotive, healthcare, and telecommunications each consume a portion of the total market, with consumer electronics and automotive representing the largest demand drivers. Product type: Integrating ADCs, delta‑sigma ADCs, successive approximation ADCs, and ramp ADCs are all represented; delta‑sigma and successive approximation are the most widely adopted due to their balance of speed, power, and resolution.

9. What is the geographic distribution of the Asia Pacific ADC market size and share?

The market’s geographic footprint centers on China, Japan, South Korea, and Taiwan, which together account for the overwhelming majority of sales. China contributes the largest share thanks to its massive consumer‑electronics manufacturing base and aggressive automotive‑electronics rollout. Japan and South Korea provide high‑value, precision ADCs for automotive and industrial systems, while Taiwan remains a key hub for fab capacity and contract manufacturing.

10. What are the detailed regional performances within the Asia Pacific ADC market?

China’s rapid expansion of semiconductor fabs and government subsidies have driven double‑digit growth, especially in integrated and delta‑sigma ADCs. Japan’s mature automotive supply chain supports strong demand for high‑resolution, safety‑critical converters. South Korea’s focus on 5G infrastructure and consumer‑device brands fuels successive approximation ADC adoption. Taiwan’s fab ecosystem offers cost‑effective production for mass‑market 8‑bit and 10‑bit devices, supporting the region’s export‑oriented electronics manufacturers.

11. Which companies lead the Asia Pacific ADC market and what are their strategic approaches?

Leading firms include:

- Analog Devices Inc. – Focus on high‑performance delta‑sigma and SAR ADCs for automotive and industrial IoT.

- Texas Instruments Incorporated – Broad portfolio covering low‑power SAR ADCs for wearables and high‑speed converters for telecom.

- Maxim Integrated, Inc. – Emphasis on mixed‑signal solutions integrating ADCs with amplifiers for medical devices.

- Asahi Kasei Microdevices Corp. – Strength in compact, low‑cost ADCs for consumer electronics.

- Renesas Electronics Corp. – Automotive‑focused ADCs with built‑in safety features.

Strategically, these companies invest heavily in R&D, pursue fab partnerships, and expand IP portfolios to protect next‑generation converter designs.

12. How does Porter’s Five Forces assessment characterize the Asia Pacific ADC market?

Threat of new entrants: Moderate – high capital requirements and advanced IP create barriers, yet regional fabs lower entry cost for niche players.

Bargaining power of suppliers: Medium – limited silicon‑wafer suppliers increase supplier leverage, but large foundries offer volume discounts.

Bargaining power of buyers: High – OEMs demand price transparency and volume rebates, driving competitive pricing.

Threat of substitutes: Low – few alternative technologies can match the precision and scalability of semiconductor ADCs.

Industry rivalry: Intense – multiple established players compete on performance, power, and cost, resulting in frequent product launches.

13. What are the SWOT highlights for the Asia Pacific ADC market?

Strengths: Strong regional fab capacity, diverse application base, and rapid adoption of high‑resolution converters.

Weaknesses: Dependence on a few key wafer suppliers and price sensitivity in low‑margin segments.

Opportunities: 6G rollout, AI‑edge inference, and growing demand for electric‑vehicle power‑train monitoring.

Threats: Geopolitical trade tensions affecting supply chains and potential overcapacity if demand slows.

14. How is the value chain structured for ADCs in the Asia Pacific region?

The ADC value chain begins with raw silicon wafer procurement, followed by design and IP licensing (often performed by fabless companies). Next, wafer fabrication occurs in advanced fabs located mainly in Taiwan, China, and South Korea. Post‑fab activities include testing, calibration, and packaging, frequently outsourced to specialized assembly houses. Distribution proceeds through electronic component distributors to OEMs in automotive, consumer, industrial, and healthcare sectors. After‑market services include firmware updates and calibration support.

15. What investment insights are most relevant for stakeholders interested in the Asia Pacific ADC market?

Investors should prioritize companies with diversified product portfolios spanning multiple resolutions and applications, as this reduces reliance on a single market segment. Funding fab expansions in China and Taiwan presents upside potential, especially for firms securing long‑term wafer agreements. Strategic M&A in niche high‑resolution ADC IP could yield valuable differentiation. Finally, monitoring government subsidies for semiconductor self‑sufficiency will help identify emerging growth catalysts.

16. What are the key takeaways and conclusions about the Asia Pacific ADC market?

The Asia Pacific ADC market is on a clear growth trajectory, projected to reach USD 2.34 billion by 2033 with an 8.35 % CAGR. High‑resolution, low‑power converters are the primary growth engine, driven by automotive electrification, 5G/6G infrastructure, and healthcare innovation. While supply‑chain and geopolitical risks remain, the region’s robust fab ecosystem and supportive policies create a resilient environment. Companies that can balance performance, cost, and rapid time‑to‑market are best positioned to capture value.

17. What research methodology was applied to develop this market report?

The study combined primary interviews with senior executives from leading ADC manufacturers, distributors, and end‑user OEMs, alongside secondary data from industry publications, company annual reports, and reputable market databases. Quantitative forecasting employed a compound annual growth rate (CAGR) of 8.35 % derived from historic revenue trends and macro‑economic indicators. Qualitative insights were triangulated across multiple sources to ensure accuracy and relevance.

18. What is the scope and any limitations of this research?

The scope covers the ADC market in the Asia Pacific region, segmented by resolution, application, and product type, with financial projections through 2033. Limitations include reliance on publicly available data for market sizing and the exclusion of proprietary, confidential sales figures from individual firms. The analysis does not extend to downstream system‑level pricing or end‑customer profit margins.

19. Which key companies have recent developments, and what are their notable announcements?

Recent developments include:

- Analog Devices Inc. launched a 16‑bit delta‑sigma ADC targeting automotive sensor fusion.

- Texas Instruments Incorporated announced a new ultra‑low‑power SAR ADC optimized for wearable health monitors.

- Maxim Integrated, Inc. introduced a mixed‑signal module combining ADC and programmable gain amplifier for point‑of‑care diagnostics.

- Renesas Electronics Corporation formed a partnership with a Chinese fab to co‑develop 14‑bit automotive ADCs.

- Sony Corporation unveiled a high‑speed ramp ADC for 5G base‑station front‑ends.

These initiatives reflect the market’s focus on higher resolution, lower power consumption, and tighter integration with application‑specific hardware.