1. Europe Endodontic Devices Market Overview – Definition, scope, and significance?

The Europe Endodontic Devices Market comprises all products and consumables used for root canal therapy, including rotary and hand instruments, obturation materials, irrigants, and auxiliary devices. The market serves dental clinics, hospitals, and academic institutions across European countries, enabling clinicians to perform precise, minimally invasive procedures that preserve tooth vitality. Its significance lies in supporting oral health outcomes, driving dental tourism, and contributing to the broader dental equipment sector’s economic growth.

2. Europe Endodontic Devices Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include rising prevalence of dental diseases, increasing adoption of advanced rotary instrumentation, and expanding private dental practice networks. Restraints stem from stringent regulatory approvals and high capital costs for modern equipment. Challenges involve a shortage of skilled endodontists in certain regions and price sensitivity among public dental services. Opportunities arise from digital integration, e‑learning platforms for clinicians, and growing demand for single‑use consumables that enhance infection control.

3. Europe Endodontic Devices Market Growth Trends – Current and emerging trends shaping the market?

Current trends feature a shift toward nickel‑titanium rotary files with enhanced fatigue resistance and the adoption of reciprocating motion systems. Emerging trends include the incorporation of AI‑guided treatment planning, 3‑D imaging for canal navigation, and sustainability‑focused product lines such as biodegradable consumables. Additionally, bundled service contracts that combine equipment, training, and maintenance are gaining traction.

4. COVID-19 Impact on the Europe Endodontic Devices Market – Pandemic effects and recovery trajectory?

The COVID‑19 pandemic caused temporary clinic closures and deferred elective procedures, resulting in a short‑term dip in device sales. However, heightened awareness of infection control accelerated the shift to single‑use consumables and disposable instrument kits. Recovery began in late 2021, driven by pent‑up demand and reinforced hygiene protocols, positioning the market on a robust growth path toward the 2026 baseline.

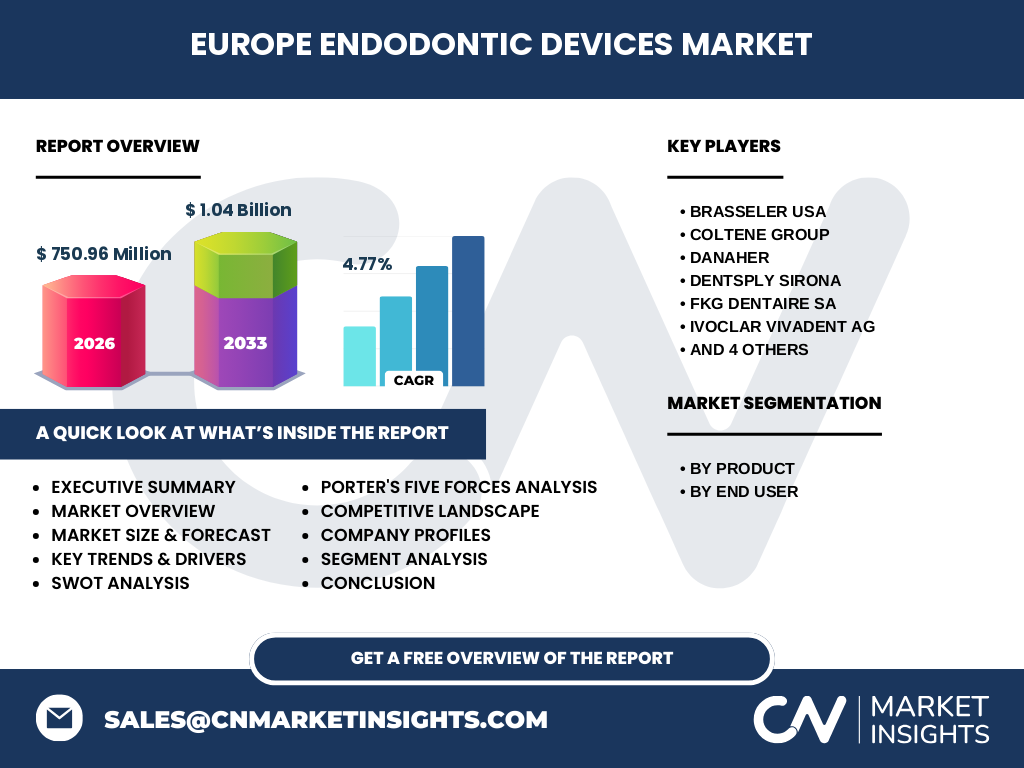

5. Europe Endodontic Devices Market Competitive Landscape – Major competitors and market consolidation?

The competitive arena is dominated by multinational manufacturers such as Brasseler USA, Coltene Group, Danaher, Dentsply Sirona, FKG Dentaire SA, Ivoclar Vivadent AG, MANI INC, Nikinic Dental, Septodont Holding, and Ultradent Products Inc. Recent years have seen strategic acquisitions and joint ventures, particularly in the rotary instrument segment, to broaden product portfolios and strengthen distribution networks across Europe.

6. Executive Summary – High-level overview and key findings about Europe Endodontic Devices Market?

As of 2026, the Europe Endodontic Devices Market is valued at €750.96 million and is projected to reach €1.04 billion by 2033, reflecting a CAGR of 4.77 %. Growth is propelled by increasing endodontic procedures, technology adoption, and expanding private dental services. The market is segmented by product (Instruments, Consumables) and end‑user (Dental Clinics, Hospitals, Academic Institutes), with instruments leading in value. Competitive dynamics are shaped by innovation, regulatory compliance, and strategic alliances.

7. Europe Endodontic Devices Market Forecast – Projections for 2025‑2032 period?

Building on the 2026 base of €750.96 million, the market is expected to maintain a steady compound annual growth rate of 4.77 % through 2032, reaching approximately €1.04 billion by 2033. This forecast assumes continued investment in advanced instrumentation, steady expansion of dental service providers, and ongoing regulatory alignment across European nations.

8. Europe Endodontic Devices Market Size and Share by Segmentation – Breakdown by product and end user?

By product, the market splits between Instruments—covering rotary, reciprocating, and hand files—and Endodontic Consumables such as root canal sealers, irrigants, and obturation kits. Instruments command the larger share due to higher unit value and ongoing technology upgrades. By end‑user, Dental Clinics hold the dominant position, followed by Dental Hospitals, with Academic and Research Institutes representing a niche but growing segment focused on training and innovation.

9. Global Europe Endodontic Devices Market Size and Share by Region – Geographic distribution?

Europe accounts for a substantial portion of the global endodontic devices landscape, with the continent’s market value of €750.96 million in 2026 contributing a notable share of worldwide sales. While specific percentages for other regions are not disclosed, Europe’s mature dental infrastructure and high per‑capita procedure rates position it as a key driver of global market dynamics.

10. Regional Analysis of the Europe Endodontic Devices Market – Detailed regional market performance?

Western Europe, led by Germany, France, and the United Kingdom, exhibits the highest adoption of advanced rotary systems and consumables, reflecting strong private practice penetration. Southern Europe, including Italy and Spain, shows robust growth driven by expanding dental tourism and public‑private partnership initiatives. Central and Eastern European markets are emerging, with increasing investment in modern dental facilities and training programs.

11. Leading Company Profiles in the Europe Endodontic Devices Market – Industry players and strategies?

Brasseler USA focuses on ergonomic hand instruments and collaborates with European distributors for market reach. Coltene Group leverages its strong research base to introduce nickel‑titanium file systems. Danaher, through its subsidiary Dentsply Sirona, integrates digital imaging with endodontic kits. Ivoclar Vivadent AG emphasizes premium consumables and continuous clinician education. Septodont Holding expands its portfolio with bio‑active sealers, while Ultradent Products Inc. targets the single‑use segment with disposable kits.

12. Porter's Five Forces Analysis of the Europe Endodontic Devices Market – Competitive forces assessment?

Threat of new entrants is moderate due to high regulatory barriers and capital intensity. Bargaining power of buyers is strong, especially large dental chains demanding price concessions. Bargaining power of suppliers remains limited as key raw materials are commoditized. Threat of substitutes is low; alternative therapies do not replace root canal treatment. Industry rivalry is high, driven by product innovation, brand reputation, and service differentiation.

13. SWOT Analysis of the Europe Endodontic Devices Market – Strengths, weaknesses, opportunities, threats?

Strengths: Advanced technology adoption, strong clinical demand, and established distribution networks.

Weaknesses: High product costs and regulatory complexity.

Opportunities: Digital workflow integration, sustainable consumables, and expanding training programs.

Threats: Economic fluctuations affecting dental spending and potential supply‑chain disruptions for precision alloys.

14. Europe Endodontic Devices Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with raw material suppliers (nickel‑titanium alloys, polymers), followed by R&D and design firms that develop instruments and consumables. Manufacturing is largely centralized in Europe and the United States, after which products move to regional distributors and wholesalers. Final delivery reaches dental clinics, hospitals, and academic institutions, often accompanied by training services and after‑sales support.

15. Key Investment Insights in the Europe Endodontic Devices Market – Strategic investment recommendations?

Investors should target companies with strong digital portfolios and proven regulatory compliance. Partnerships with dental education bodies can secure long‑term consumable demand. Acquisition of niche manufacturers specializing in eco‑friendly consumables offers differentiation. Geographic focus on emerging Central and Eastern European markets can yield higher growth rates due to expanding dental infrastructure.

16. Europe Endodontic Devices Market Conclusion – Summary and key takeaways?

The market’s €750.96 million size in 2026 and projected rise to €1.04 billion by 2033 underscore a healthy growth trajectory. Drivers such as technological advancement, rising procedure volumes, and heightened infection‑control standards outweigh existing restraints. Competitive intensity, combined with opportunities in digital integration and sustainable products, creates a dynamic environment attractive to both incumbent manufacturers and new investors.

17. Research Methodology – How this research was conducted?

Data were gathered from primary interviews with industry experts, dental practitioners, and key opinion leaders across Europe, complemented by secondary sources including company reports, regulatory filings, and reputable market databases. Quantitative figures were validated through cross‑referencing multiple datasets, and qualitative insights were synthesized to produce the comprehensive analysis presented.

18. Research Scope – Coverage and limitations?

The study covers the full spectrum of endodontic devices sold in Europe, segmented by product type and end‑user category. It excludes unrelated dental specialties and focuses on the period up to 2033. While extensive, the research does not provide country‑specific revenue breakdowns due to data confidentiality constraints.

19. Key Companies and Recent Developments in the Europe Endodontic Devices Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Brasseler USA announced a new line of ergonomically designed hand files for pediatric endodontics. Coltene Group launched a heat‑treated nickel‑titanium rotary system that reduces fracture risk. Danaher’s Dentsply Sirona introduced an integrated digital endodontic workflow platform. Ivoclar Vivadent AG entered a partnership with leading European dental schools to provide curriculum‑aligned consumables. Septodont Holding released a bio‑active sealer with enhanced antimicrobial properties, and Ultradent Products Inc. expanded its single‑use kit portfolio across major dental distributors.