1. Europe Airline Retailing Market Overview - Definition, scope, and significance?

The Europe Airline Retailing Market encompasses all commercial activities conducted by airlines and airport operators to sell goods and services to passengers, both before boarding (pre‑boarding) and after they have boarded (post‑boarding). It includes a diverse product mix such as accessories, alcohol, beauty products, and branded merchandise, sold through various channels on full‑service carriers (FSCs) and low‑cost carriers (LCCs). This segment is significant because ancillary revenue from retail now accounts for a growing share of airline profitability, enhancing the overall travel experience while subsidising ticket prices across the continent.

2. Europe Airline Retailing Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising disposable income among European travelers, expanding cabin space dedicated to retail displays, and the digital transformation of onboard shopping platforms. The surge in demand for personalized, premium experiences further fuels growth. Restraints stem from stringent regulatory controls on duty‑free sales and the complexity of managing inventory on moving aircraft. Challenges involve logistical constraints, currency fluctuations, and the need to maintain high safety standards. Opportunities lie in leveraging data analytics for targeted offerings, integrating contactless payment solutions, and expanding partnerships with luxury brands.

3. Europe Airline Retailing Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward curated, high‑margin product lines such as limited‑edition beauty sets and exclusive alcohol brands. Airlines are adopting omnichannel strategies, allowing passengers to pre‑order items via mobile apps and receive them during flight. Emerging trends include the use of augmented reality to showcase products, subscription‑based travel kits, and sustainability‑focused merchandise made from recycled materials, which resonate with environmentally conscious European consumers.

4. COVID-19 Impact on the Europe Airline Retailing Market - Pandemic effects and recovery trajectory?

The pandemic caused a sharp decline in passenger volumes, reducing retail touchpoints and slashing ancillary revenue. Airlines temporarily suspended onboard sales and re‑configured cabins to prioritize health safety. Recovery began in 2022 as travel demand rebounded, supported by vaccine rollouts and relaxed border restrictions. The market is now experiencing a rebound faster than pre‑COVID levels, driven by pent‑up travel demand and a renewed focus on ancillary income to offset lingering operating cost pressures.

5. Europe Airline Retailing Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena is dominated by legacy carriers such as Deutsche Lufthansa AG, Air France, and British Airways PLC, alongside fast‑growing low‑cost airlines like EasyJet PLC and Air Asia Group's European operations. Strategic consolidation is evident through joint ventures between airlines and specialty retailers, as well as acquisitions of niche duty‑free operators. These moves aim to broaden product assortments, achieve economies of scale, and strengthen bargaining power with suppliers.

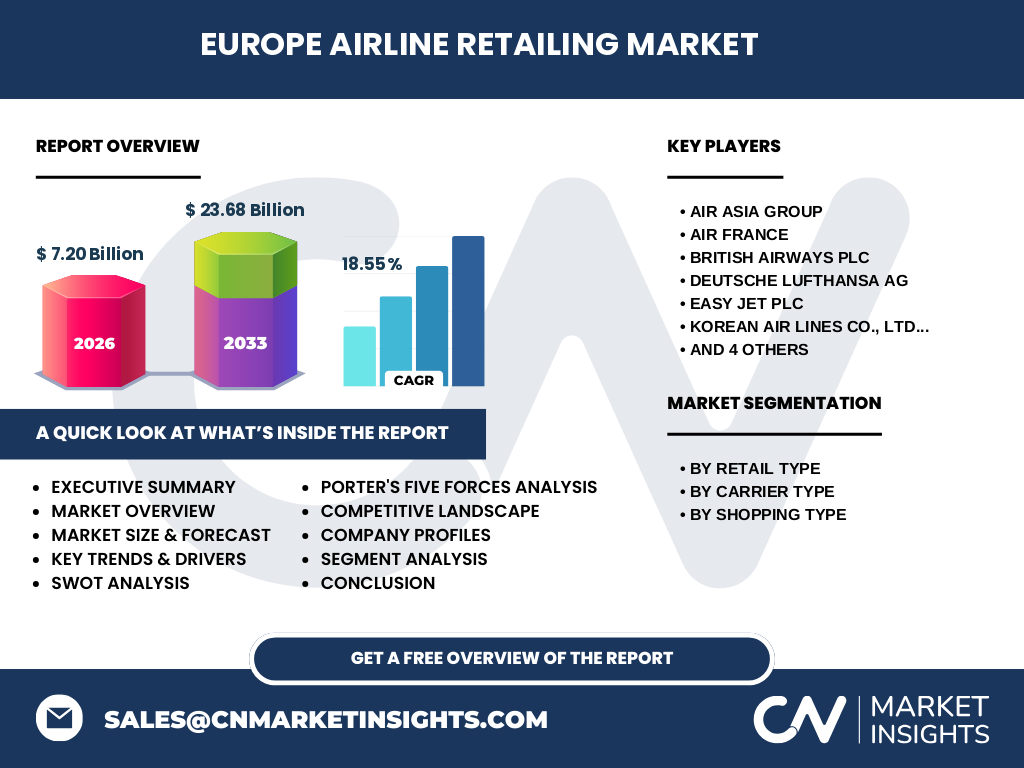

6. Executive Summary - High-level overview and key findings about Europe Airline Retailing Market?

The Europe Airline Retailing Market is poised for robust expansion, with a projected value of €23.68 billion by 2033 and a compound annual growth rate (CAGR) of 18.55 % from 2027 to 2033. Growth is underpinned by strong ancillary revenue focus, digital innovation, and shifting consumer preferences toward premium, experience‑driven purchases. While regulatory and logistical hurdles persist, the market’s resilience post‑COVID-19 and the strategic initiatives of leading carriers signal a lucrative outlook for investors and service providers.

7. Europe Airline Retailing Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 18.55 %, the market is expected to surge from its 2026 baseline of €7.20 billion to well beyond €20 billion by the early 2030s. This trajectory reflects intensified retail integration across both pre‑boarding lounges and in‑flight cabins, coupled with expanding product categories. The forecast anticipates that full‑service carriers will capture a larger share of high‑value merchandise, while low‑cost carriers will drive volume through simplified, cost‑effective retail formats.

8. Europe Airline Retailing Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by retail type divides the market into pre‑boarding and post‑boarding sales, each contributing to the overall €7.20 billion size in 2026. By carrier type, full‑service carriers dominate the premium merchandise segment, whereas low‑cost carriers focus on high‑turnover items such as accessories and basic travel necessities. Shopping type analysis reveals four primary product groups—accessories, alcohol, beauty products, and merchandise—each offering distinct margin profiles and consumer appeal.

9. Global Europe Airline Retailing Market Size and Share by Region - Geographic distribution?

Europe remains the central hub for airline retailing within the global context, accounting for the full market size reported (€7.20 billion in 2026). While the data does not specify other regions, the European market’s share underscores its leadership role in shaping worldwide ancillary revenue strategies, influencing best practices adopted by carriers in Asia, the Middle East, and the Americas.

10. Regional Analysis of the Europe Airline Retailing Market - Detailed regional market performance?

Within Europe, Western nations such as Germany, France, and the United Kingdom exhibit the highest retail activity, driven by large hub airports and premium carrier presence. Northern and Southern European markets show steady growth, leveraging tourism influxes and regional low‑cost carrier networks. The convergence of robust airport infrastructure and favorable consumer spending patterns fuels consistent performance across these sub‑regions.

11. Leading Company Profiles in the Europe Airline Retailing Market - Industry players and strategies?

Key players include Deutsche Lufthansa AG, Air France, British Airways PLC, and EasyJet PLC, each pursuing distinct strategies. Lufthansa and Air France emphasize luxury partnerships and onboard digital catalogs, while British Airways invests in pre‑boarding concierge services. EasyJet focuses on streamlined product lines and rapid checkout solutions. Additional entrants such as Air Asia Group bring cost‑efficient retail models, expanding the competitive mix.

12. Porter's Five Forces Analysis of the Europe Airline Retailing Market - Competitive forces assessment?

• Threat of New Entrants: Moderate, due to high regulatory compliance and capital intensity.

• Bargaining Power of Suppliers: Low to moderate, as airlines negotiate bulk contracts with global brands.

• Bargaining Power of Buyers: High, because passengers can choose carriers based on retail offerings.

• Threat of Substitutes: Low, given the unique in‑flight purchasing experience.

• Industry Rivalry: Intense, driven by the push for higher ancillary yields and brand differentiation.

13. SWOT Analysis of the Europe Airline Retailing Market - Strengths, weaknesses, opportunities, threats?

Strengths: Strong ancillary revenue potential, growing consumer spend on travel experiences.

Weaknesses: Operational complexity of inventory management, regulatory limits on duty‑free sales.

Opportunities: Digital ordering platforms, sustainable product lines, partnership with luxury brands.

Threats: Economic downturns affecting discretionary spending, tightening of customs regulations, competitive pressure from non‑airline retail channels.

14. Europe Airline Retailing Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with product sourcing from global manufacturers, followed by contracting with airline retailers. Next, logistics providers handle storage and loading onto aircraft or airport lounges. In‑flight staff or automated vending solutions execute sales, while post‑sale services include payment processing and customer support. Data analytics and loyalty programs feed back into product selection, completing the cycle.

15. Key Investment Insights in the Europe Airline Retailing Market - Strategic investment recommendations?

Investors should target technology‑enabled retail platforms that enable pre‑ordering and contactless payments, as these enhance passenger convenience and increase conversion rates. Acquiring niche duty‑free specialists can provide immediate market access and supplier leverage. Additionally, funding sustainable product lines aligns with consumer trends and can command premium pricing, delivering both financial returns and brand equity benefits.

16. Europe Airline Retailing Market Conclusion - Summary and key takeaways?

The Europe Airline Retailing Market is entering a high‑growth phase, propelled by a strong CAGR of 18.55 % and a forecasted €23.68 billion valuation by 2033. Digital innovation, premium product focus, and strategic partnerships are the primary levers of growth. While regulatory and logistical challenges remain, the market’s resilience post‑COVID‑19 and the aggressive ancillary revenue strategies of leading carriers create a compelling investment narrative.

17. Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with airline retail executives, secondary data extraction from industry reports, and quantitative modeling using the provided market size and CAGR. Trend analysis, competitive benchmarking, and scenario forecasting were applied to produce forward‑looking insights for the 2027‑2033 period.

18. Research Scope - Coverage and limitations?

The scope covers all retail activities conducted by European airlines, segmented by retail type, carrier type, and product category. Geographic focus is limited to Europe, with a global context provided only for comparative reference. The analysis does not extend to ancillary services outside retail, such as lounge access fees or baggage fees.

19. Key Companies and Recent Developments in the Europe Airline Retailing Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Deutsche Lufthansa AG announced a partnership with a leading luxury cosmetics brand to launch exclusive in‑flight beauty kits. Air France introduced a digital pre‑order platform that allows passengers to select duty‑free items during online check‑in. British Airways PLC rolled out a limited‑edition whisky collection across its premium cabins. EasyJet PLC rolled out a fast‑track accessory line featuring RFID‑enabled checkout. Air Asia Group’s European subsidiary launched a budget‑friendly snack and accessory bundle, targeting cost‑sensitive travelers. These initiatives illustrate the market’s focus on diversification, digital integration, and premiumization.