What is the Pet Food Market Overview – definition, scope, and significance?

The Pet Food Market comprises all processed and formulated foods designed specifically for companion animals, primarily dogs and cats. It spans a broad product spectrum that includes dry kibble, wet meals, snacks, and treats, offered through various channels such as supermarkets, specialty stores, veterinary clinics, convenience outlets, and online platforms. This market is significant because pet ownership is on the rise globally, driving consistent demand for nutritionally balanced, convenient, and specialty pet foods that support animal health and owner lifestyles.

What are the main drivers, restraints, challenges, and opportunities in the Pet Food Market?

Key drivers include increasing pet humanization, rising disposable income, and growing awareness of pet nutrition, which boost premium and functional food demand. Restraints stem from raw material price volatility and stringent regulatory requirements that can delay product launches. Challenges involve supply‑chain disruptions and intense competition across price points. Opportunities arise from the emergence of plant‑based formulas, personalized nutrition, and expansion of e‑commerce channels that enable direct‑to‑consumer engagement.

Which growth trends are currently shaping the Pet Food Market?

Current trends feature a shift toward natural, clean‑label ingredients and functional additives such as probiotics and joint‑support compounds. There is a notable rise in plant‑based and alternative protein offerings, catering to eco‑conscious owners. Hybrid sales models that blend offline retail with robust online platforms are accelerating, while subscription services for regular deliveries are gaining traction. Moreover, data‑driven customization, using pet DNA testing to tailor diets, is emerging as a niche yet fast‑growing segment.

How did COVID‑19 impact the Pet Food Market and what is the recovery trajectory?

The pandemic spurred a surge in pet adoption and increased spending on pet care, resulting in a temporary boost in sales, especially for online channels. Supply chain bottlenecks led to short‑term stockouts of certain SKUs, prompting manufacturers to diversify sourcing. As economies normalize, growth remains resilient, supported by sustained pet‑owner spending and the continued expansion of digital retail, indicating a steady recovery and a long‑term upward trajectory.

Who are the major competitors and what is the level of market consolidation in the Pet Food Market?

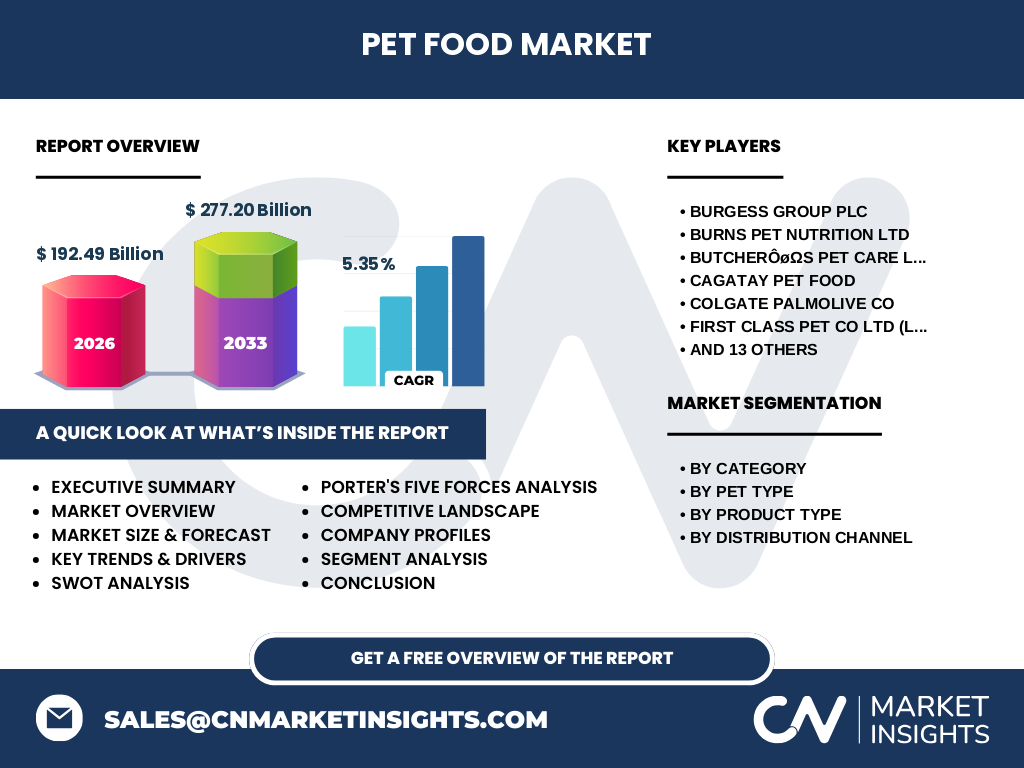

The competitive landscape is fragmented, with multinational giants such as Mars Inc., Nestlé SA, and J M Smucker Co. alongside specialized firms like Burgess Group PLC, Burns Pet Nutrition Ltd, and General Mills Inc. Recent consolidation activity includes strategic acquisitions and joint ventures aimed at expanding product portfolios and geographic reach. Despite this, the market retains a high degree of competition across all segments, fostering innovation and price competition.

What are the key findings presented in the Executive Summary of the Pet Food Market report?

The Executive Summary highlights a market valued at $192.49 billion in 2026, projected to reach $277.20 billion by 2033, reflecting a 5.35 % CAGR. Growth is driven by pet humanization, premiumization, and digital distribution. Plant‑based and functional foods are emerging hotspots, while e‑commerce continues to outpace traditional retail. The report underscores strategic opportunities for companies to invest in sustainable sourcing, innovate product formats, and leverage data‑rich consumer insights.

What are the forecast expectations for the Pet Food Market from 2025 to 2032?

Forecasts anticipate a steady increase in market size, maintaining the 5.35 % compound annual growth rate through 2032. The expansion is expected across all product types, with premium dry and wet foods leading the growth curve. Distribution channels will see a continued shift toward online retail, while specialty stores retain strength in high‑margin segments. Geographic expansion, particularly in emerging economies, will contribute significantly to overall market uplift.

How is the Pet Food Market sized and shared by segmentation?

Segmentation by category divides the market into animal‑based and plant‑based formulations, reflecting the growing demand for alternative proteins. By pet type, dogs command the largest share, followed by cats, each driving distinct product lines. Product type segmentation includes dry food, wet food, and snacks & treats, with dry food traditionally holding the largest volume due to convenience and shelf stability. Distribution channels are split among supermarkets & hypermarkets, pet specialty stores, veterinary clinics, convenience stores, and online retail, each catering to different consumer purchasing behaviors.

What is the global distribution of the Pet Food Market size and share by region?

The market exhibits a broad geographic footprint, with North America and Europe historically holding the largest shares due to high pet ownership rates and mature retail infrastructures. Asia‑Pacific is emerging rapidly, driven by rising middle‑class income and increasing pet adoption. Latin America and the Middle East & Africa show incremental growth, propelled by urbanization and expanding retail networks. Regional dynamics influence product preferences, regulatory environments, and channel strategies.

What detailed insights are provided in the Regional Analysis of the Pet Food Market?

Regional analysis examines market performance, growth drivers, and consumer trends within each major geography. In North America, premium and functional foods dominate, while Europe emphasizes sustainability and organic formulations. Asia‑Pacific markets focus on affordability coupled with growing interest in premiumization, especially in urban centers. Latin America showcases a blend of value‑priced products and gradual adoption of specialty lines. The Middle East & Africa highlight opportunities linked to expanding veterinary services and e‑commerce penetration.

Which companies are profiled as leading players in the Pet Food Market, and what are their strategic approaches?

Leading profiles cover Burgess Group PLC, Burns Pet Nutrition Ltd, Butcher’s Pet Care Limited, Cagatay Pet Food, Colgate Palmolive Co, First Class Pet Co Ltd (Little BigPaw), Forthglade Foods Ltd, Furchild Nutrition LLC, General Mills Inc, Inspired Pet Nutrition Ltd, J M Smucker Co, MPM Products Ltd, Mars Inc., Nestlé SA, Monge & C SpA, Schell & Kampeter Inc, Symply Pet Food Ltd, United Petfood Group BV, VAFO Group AS, and Wunderdog Animal Feed Manufacturing LLC. Strategies range from product innovation and portfolio diversification to strategic acquisitions, sustainability initiatives, and accelerated digital sales channels.

How does Porter’s Five Forces analysis evaluate the Pet Food Market?

Threat of new entrants is moderate due to high capital requirements and regulatory barriers, yet niche players can enter via online platforms. Bargaining power of suppliers is moderate; reliance on specific protein sources can increase leverage, but diversified sourcing mitigates risk. Bargaining power of buyers is high, as retailers and pet owners demand quality, price transparency, and brand differentiation. Threat of substitutes is low, given the essential nature of pet nutrition, though homemade diets pose a minor challenge. Industry rivalry is intense, driven by numerous global and regional brands competing on price, innovation, and distribution.

What are the SWOT analysis findings for the Pet Food Market?

Strengths: Strong and growing demand, high brand loyalty, and diversified product portfolios.

Weaknesses: Sensitivity to raw material cost fluctuations and complex regulatory compliance.

Opportunities: Expansion of plant‑based lines, personalized nutrition, and e‑commerce growth.

Threats: Supply chain disruptions, intensifying price competition, and potential regulatory tightening on ingredient claims.

How is the value chain of the Pet Food Market structured?

The value chain starts with raw material procurement (animal proteins, plant proteins, vitamins, and minerals), proceeds to formulation and manufacturing (mixing, extrusion, canning, packaging), followed by distribution through wholesale, retail, and direct‑to‑consumer channels. Marketing and brand management add value, while after‑sales services such as nutritional counseling and subscription support enhance customer retention. Technology integration at each stage—particularly in traceability and supply‑chain optimization—creates competitive advantage.

What key investment insights are recommended for stakeholders in the Pet Food Market?

Investors should target companies with strong R&D pipelines focused on functional and plant‑based products, as these segments promise higher margins. Portfolio diversification across geographic regions reduces exposure to localized regulatory or economic shocks. Emphasis on digital transformation—especially direct‑to‑consumer platforms and data analytics—will capture shifting consumer purchasing patterns. Sustainable sourcing and transparent labeling are becoming critical differentiators, attracting both consumers and ESG‑focused capital.

What conclusions can be drawn from the Pet Food Market analysis?

The Pet Food Market is on a robust growth trajectory, underpinned by changing consumer attitudes toward pets, premiumization, and digital retail expansion. While raw material volatility and regulatory complexities pose challenges, opportunities in sustainable, functional, and personalized nutrition provide clear pathways for differentiation. Companies that innovate, embrace e‑commerce, and align with sustainability trends are positioned to capture the expanding market value projected to reach $277.20 billion by 2033.

What research methodology was employed to compile this Pet Food Market report?

The study combined primary interviews with industry experts, senior executives, and veterinarians, alongside secondary data collection from company filings, market databases, trade journals, and reputable statistical agencies. Quantitative analysis applied time‑series forecasting to derive the 5.35 % CAGR, while qualitative insights were synthesized through thematic coding of expert opinions. Cross‑validation ensured consistency between primary insights and secondary sources.

What is the scope of the research, and what limitations, if any, exist?

The research scope covers global market size, segmentation by category, pet type, product type, and distribution channel, as well as regional breakdowns, competitive landscape, and forward‑looking forecasts through 2033. Limitations include reliance on publicly available financial disclosures and the absence of proprietary sales data for some private firms, which may affect granularity of segment‑level market share estimations.

Which key companies and recent developments are highlighted in the Pet Food Market?

Highlighted firms include Mars Inc. and Nestlé SA, which have launched new high‑protein dry lines; J M Smucker Co. expanding its organic wet food portfolio; General Mills Inc. entering the pet snack segment via a strategic acquisition; and Colgate Palmolive Co. introducing a dental‑care treat range. Recent partnerships feature Burgess Group PLC collaborating with veterinary clinics for customized nutrition programs, and Wunderdog Animal Feed Manufacturing LLC leveraging blockchain for supply‑chain transparency.