What is the Flight Inspection Market overview – definition, scope, and significance?

The Flight Inspection Market encompasses the design, manufacture, integration, and support of systems and services used to verify the accuracy and safety of aviation navigation aids, instrument procedures, and airspace configurations. It serves both defense and commercial airports, covering hardware such as radar calibrators, GPS/ GNSS flight inspection aircraft, and software platforms that process flight‑test data. The market is significant because it underpins the compliance of air navigation services with international standards, directly influencing flight safety, operational efficiency, and regulatory certification worldwide.

What are the main drivers, restraints, challenges, and opportunities in the Flight Inspection Market?

Key drivers include rising air traffic volumes, modernization of air navigation systems (e.g., transition to satellite‑based navigation), and stringent safety regulations that demand frequent calibration of navaids. Opportunities arise from emerging technologies such as unmanned aerial systems for inspection and AI‑enabled data analytics, which can reduce cost and turnaround time. Restraints involve high capital expenditure for specialized aircraft and equipment, and lengthy certification processes. Challenges include limited skilled personnel and the need to integrate legacy infrastructure with next‑generation solutions.

Which growth trends are currently shaping the Flight Inspection Market?

Current trends feature a shift toward integrated “system‑as‑a‑service” models, where providers bundle hardware, software, and ongoing maintenance. There is growing adoption of GNSS‑based inspection techniques that supplement traditional radar calibration. Digital twins and real‑time data streaming are being piloted to enhance predictive maintenance of navigation aids. Additionally, collaborative programs between civil aviation authorities and defense agencies are accelerating the deployment of multi‑role inspection platforms.

How did COVID‑19 impact the Flight Inspection Market and what is the recovery trajectory?

The pandemic caused a temporary slowdown in flight‑test activities due to reduced air traffic and travel restrictions, leading to deferred inspection contracts. However, the market demonstrated resilience as airlines and airports prioritized safety, prompting a swift rebound in demand for calibration services. Recovery is now well underway, with a renewed focus on modernizing navigation infrastructure to support post‑pandemic traffic growth, positioning the market for sustained expansion.

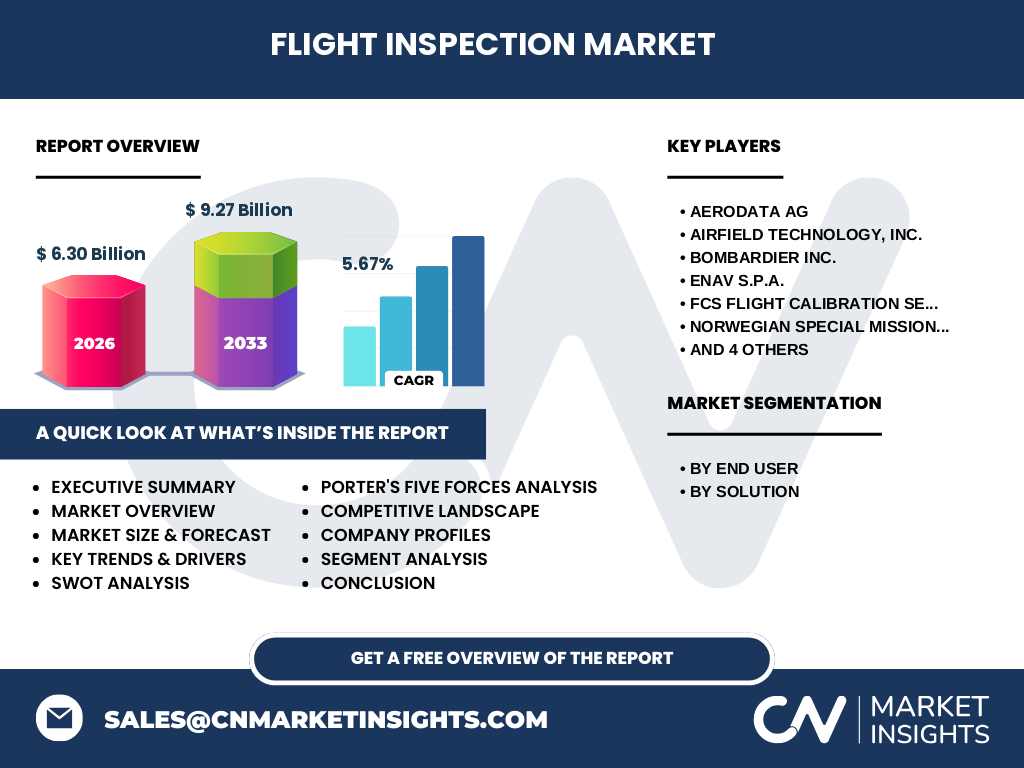

Who are the major competitors in the Flight Inspection Market and what is the state of market consolidation?

Leading players include Aerodata AG, Airfield Technology Inc., Bombardier Inc., ENAV S.p.A., FCS Flight Calibration Services GmbH, Norwegian Special Mission AS, Radiola Limited, Rohde & Schwarz GmbH & Co. KG, Safran S.A., and Textron Inc. The competitive landscape is moderately consolidated, with a few large firms offering end‑to‑end solutions and several specialized niche providers focusing on either system hardware or service contracts. Recent mergers and strategic alliances have modestly increased concentration, yet ample room remains for new entrants leveraging innovative technologies.

What are the key findings highlighted in the executive summary of the Flight Inspection Market?

The executive summary underscores a robust market valued at USD 6.30 billion in 2026, projected to reach USD 9.27 billion by 2033, reflecting a CAGR of 5.67 % over the forecast horizon. Growth is driven by expanding air traffic, regulatory pressure for frequent navaid calibration, and adoption of advanced GNSS‑based inspection tools. The report identifies defense airports and commercial airports as primary end‑user segments, with system sales outpacing services due to technology refresh cycles. Competitive dynamics favor firms with integrated hardware‑software‑service portfolios.

What are the forecast projections for the Flight Inspection Market from 2025 to 2032?

Based on the provided CAGR of 5.67 %, the market is expected to maintain steady growth throughout the 2025‑2032 period. By 2027, the market size will be approaching the mid‑point of the forecast range, and by 2032 it will be nearing the upper bound of the USD 9.27 billion projection for 2033. This trajectory indicates consistent demand from both defense and commercial sectors, supported by ongoing airspace modernization programs worldwide.

How is the Flight Inspection Market sized and shared by segmentation?

The market is segmented by end‑user and solution type. End‑user segmentation divides the market into Defense Airport and Commercial Airport, each requiring tailored inspection solutions for military and civilian navigation infrastructure. By solution, the market splits into System (hardware, aircraft, sensors) and Services (calibration, data analysis, maintenance). While precise monetary shares are not disclosed, system sales typically dominate due to periodic equipment upgrades, whereas services generate recurring revenue through contract renewals.

What is the global Flight Inspection Market size and share by region?

The global market totals USD 6.30 billion in 2026, expanding to USD 9.27 billion by 2033. Although regional breakdowns are not numerically specified, the market is globally distributed, with strong demand in regions investing heavily in air navigation modernization, such as North America, Europe, and the Asia‑Pacific. These regions collectively account for the majority of market revenue, while emerging markets contribute incremental growth through new airport developments.

What does the regional analysis reveal about Flight Inspection Market performance?

North America benefits from mature aviation infrastructure and significant defense spending, driving frequent system upgrades. Europe’s emphasis on SESAR (Single European Sky ATM Research) programs fuels demand for advanced inspection services. The Asia‑Pacific region experiences rapid airport construction and air traffic growth, creating opportunities for both system sales and service contracts. Latin America and the Middle East show moderate growth, primarily linked to airport expansions and defense modernization initiatives.

Which leading companies operate in the Flight Inspection Market and what are their strategies?

Aerodata AG focuses on high‑precision GNSS‑based calibration platforms and strategic partnerships with air navigation service providers. Airfield Technology Inc. emphasizes turnkey solutions combining aircraft, sensors, and data‑processing software. Bombardier Inc. leverages its existing aircraft portfolio to offer customized inspection kits. ENAV S.p.A. and Safran S.A. pursue vertical integration, coupling system manufacturing with long‑term service agreements. Rohde & Schwarz and Textron prioritize technology innovation, investing in next‑generation radar and satellite simulators.

How does Porter’s Five Forces analysis apply to the Flight Inspection Market?

Threat of new entrants is moderate due to high capital requirements and regulatory barriers. Bargaining power of suppliers is relatively low; key components such as avionics are widely sourced. Bargaining power of buyers is moderate, as airports and defense agencies can negotiate long‑term contracts but depend on specialized providers. Threat of substitutes remains low because alternative inspection methods lack the accuracy of dedicated flight‑test platforms. Competitive rivalry is strong, driven by a handful of firms competing on technology, service quality, and lifecycle support.

What are the SWOT highlights for the Flight Inspection Market?

Strengths: Critical safety function, high entry barriers, and growing regulatory demand. Weaknesses: Capital‑intensive nature and limited pool of qualified personnel. Opportunities: Integration of AI, unmanned inspection drones, and data‑analytics services. Threats: Economic cycles affecting defense budgets and potential delays in government procurement processes.

What does the value chain analysis reveal about the Flight Inspection Market?

The value chain starts with R&D and design of inspection aircraft and sensor suites, followed by manufacturing of hardware components. Next, system integration combines aircraft, avionics, and software. After delivery, providers offer training, calibration services, data processing, and ongoing maintenance. The final stage involves post‑flight analysis and reporting to aviation authorities, creating a recurring revenue stream through service contracts and upgrades.

What key investment insights can be drawn for the Flight Inspection Market?

Investors should target companies with diversified portfolios that include both system hardware and recurring services, as the latter ensures steady cash flow. Firms that are early adopters of emerging technologies—such as UAV‑based inspection and AI‑driven analytics—are positioned for higher growth. Strategic partnerships with civil aviation authorities or defense ministries can provide long‑term contracts, reducing revenue volatility.

What conclusions can be drawn about the Flight Inspection Market?

The Flight Inspection Market is poised for continued expansion, driven by mandatory safety regulations, air traffic growth, and technological advancements. While capital intensity and skilled‑labor scarcity present challenges, the sector’s essential role in aviation safety ensures stable demand. Companies that blend innovative systems with robust service models are likely to capture the greatest market share.

What research methodology was employed to compile this market report?

The analysis combined primary interviews with industry experts, secondary data from government aviation authorities, and financial filings of key players. Trend extrapolation used the provided CAGR of 5.67 % to forecast future market size. Segmentation was derived from the defined end‑user and solution categories, and competitive assessment incorporated market‑share observations, product portfolios, and recent strategic moves.

What is the scope of this research and its limitations?

The scope covers global market size, segmentation by end‑user and solution, regional distribution, and competitive dynamics for the period 2025‑2033. It excludes granular regional revenue figures and specific market‑share percentages beyond the aggregate data supplied. The study focuses on the listed key companies and does not assess smaller niche providers that may operate in limited locales.

Which key companies are notable and what recent developments have they announced?

Aerodata AG recently launched an upgraded GNSS calibration suite with real‑time data streaming. Airfield Technology Inc. secured a multi‑year contract with a major European defense agency for fleet inspection services. Bombardier Inc. introduced a retrofit kit for its Learjet platform enabling cost‑effective flight inspection. ENAV S.p.A. partnered with a leading satellite provider to enhance GNSS‑based verification. Safran S.A. announced a joint venture with a data‑analytics firm to deliver predictive maintenance insights for navaids. These initiatives reflect a market trend toward integrated hardware‑software‑service ecosystems.