What is the China Transmucosal Drug Delivery Systems Market Overview - Definition, scope, and significance?

The China Transmucosal Drug Delivery Systems (TMDD) market encompasses technologies and products that deliver pharmaceutical agents across mucosal membranes such as oral, nasal, vaginal, and urethral/rectal sites. These systems include films, sprays, gels, tablets, and patches designed to enhance bioavailability, provide rapid onset, and improve patient compliance. In China, the market’s scope extends from hospital and clinic procurement to pediatric and adult applications, addressing a broad therapeutic spectrum that includes pain management, hormone therapy, and infectious disease treatment. The significance of TMDD lies in its ability to bypass first‑pass metabolism, enable non‑invasive administration, and cater to an increasingly health‑conscious population that prefers convenient dosing forms.

What are the China Transmucosal Drug Delivery Systems Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising prevalence of chronic diseases, a growing elderly population, and heightened demand for self‑medication options. Government initiatives promoting innovative drug delivery and increased R&D funding further stimulate market growth. Restraints involve stringent regulatory pathways for novel delivery platforms and reimbursement uncertainties in public health insurance schemes. Challenges arise from limited awareness among clinicians about the comparative advantages of TMDD versus traditional oral tablets, as well as manufacturing complexities associated with maintaining drug stability in mucosal environments. Opportunities are found in expanding indications for pediatric use, leveraging digital health integration for adherence monitoring, and exploiting partnerships between multinational pharmaceutical firms and local contract development organizations.

What are the China Transmucosal Drug Delivery Systems Market Growth Trends?

Current trends feature a shift toward personalized dosage forms, such as patient‑specific oral films that can be printed on demand. Companies are also exploring multifunctional platforms that combine drug delivery with diagnostic biosensors. Biopharmaceuticals, especially peptide and protein therapeutics, are increasingly being formulated for transmucosal routes to improve convenience and reduce injection reliance. Additionally, there is a notable rise in the adoption of nasal sprays for vaccine delivery, accelerated by recent public health campaigns.

How has COVID‑19 impacted the China Transmucosal Drug Delivery Systems Market?

The COVID‑19 pandemic initially disrupted supply chains and delayed clinical trials, temporarily slowing market momentum. However, heightened awareness of respiratory health and the need for non‑invasive vaccine administration sparked increased interest in nasal and oral delivery technologies. Post‑pandemic recovery has been robust, with manufacturers accelerating the launch of COVID‑related nasal spray formulations and scaling production capacities. The market is now on an upward trajectory, reflecting renewed confidence in the resilience of TMDD platforms.

Who are the major competitors in the China Transmucosal Drug Delivery Systems Market and what is the competitive landscape?

The competitive landscape is characterized by a mix of global pharmaceutical giants and specialized niche players. Leading firms include 3M, Novartis AG, Teva Pharmaceutical Industries Ltd, and Reckitt Benckiser Group plc, each offering a portfolio of oral and nasal delivery products. Smaller innovators such as Acrux Limited, GW Pharmaceuticals plc, and West Pharmaceutical Development, LLC focus on advanced formulations for specific therapeutic areas. Market consolidation is evident through strategic alliances, joint ventures, and acquisition of technology assets, enabling firms to broaden their product pipelines and strengthen distribution networks across hospitals and clinics.

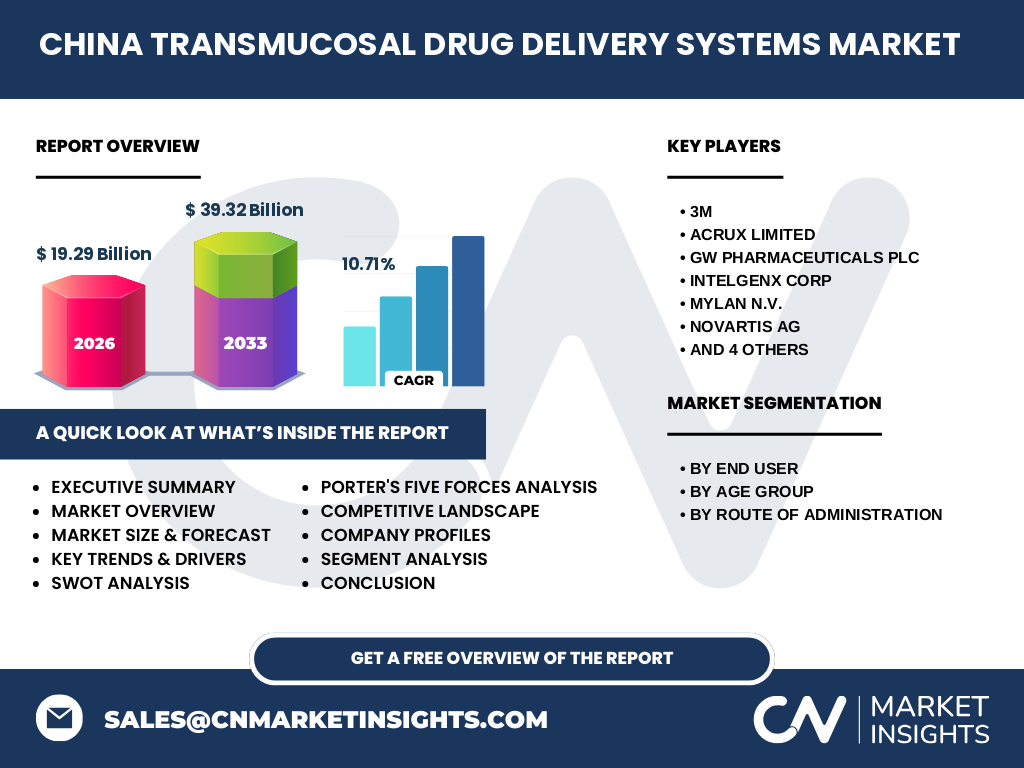

What does the Executive Summary reveal about the China Transmucosal Drug Delivery Systems Market?

The executive summary highlights that the China TMDD market is valued at 19.29 billion CNY in 2026 and is projected to reach 39.32 billion CNY by 2033, reflecting a robust compound annual growth rate of 10.71 %. Growth is driven by expanding end‑user segments, notably hospitals and clinics, and by rising adoption across adult and pediatric populations. The market’s diversification across oral, nasal, vaginal, and urethral/rectal routes positions it for sustained expansion, while innovation and regulatory support underpin long‑term profitability.

What are the forecast expectations for the China Transmucosal Drug Delivery Systems Market from 2025 to 2032?

Based on the provided CAGR of 10.71 %, the market is expected to maintain a steady upward trajectory throughout the forecast horizon. By 2032, the market size is anticipated to approach the upper end of the 2027‑2033 projection range, underscoring strong demand for advanced delivery formats. The forecast accounts for continued investment in R&D, increased clinical adoption of TMDD products, and expanding reimbursement coverage for high‑value therapies.

How is the China Transmucosal Drug Delivery Systems Market sized and shared by segmentation?

Segmentation by end‑user shows hospitals as the primary purchasers, reflecting the need for rapid‑acting formulations in acute care settings, while clinics represent a growing secondary channel for chronic disease management. Age‑group segmentation reveals a balanced demand between adults and pediatrics, with pediatric formulations gaining traction due to ease of administration. Route‑of‑administration segmentation indicates oral and nasal systems dominate the market, driven by convenience and suitability for both systemic and localized therapy. Vaginal and urethral/rectal routes, though smaller, are experiencing niche growth linked to hormonal and urogenital indications.

What is the global China Transmucosal Drug Delivery Systems market size and share by region?

While the focus of this report is China, the market contributes a substantial portion of the global TMDD landscape. China’s valuation of 19.29 billion CNY in 2026 represents a significant share of worldwide demand, positioning the country as a leading hub for both production and consumption of transmucosal technologies. The robust growth forecast further indicates China’s expanding influence on global market dynamics.

What does the regional analysis reveal about the China Transmucosal Drug Delivery Systems market?

Regional analysis shows strong concentration of market activity in Tier‑1 and Tier‑2 cities where major hospitals and specialty clinics are located. These urban centers benefit from higher healthcare spending, greater physician awareness, and faster adoption of innovative therapies. Peripheral regions are gradually increasing their market participation as distribution networks expand and local healthcare facilities upgrade their formulary offerings. The regional spread aligns with China’s broader healthcare reform aimed at equitable access to advanced drug delivery options.

Which companies lead the China Transmucosal Drug Delivery Systems market and what are their strategies?

Industry leaders such as 3M leverage extensive material science capabilities to develop high‑performance film and patch technologies. Novartis focuses on integrating TMDD into its specialty drug portfolio, emphasizing clinical validation. Teva pursues cost‑effective generic transmucosal products to capture price‑sensitive segments. Reckitt Benckiser employs strong consumer‑brand leverage for over‑the‑counter oral sprays. Emerging players like Acrux Limited and GW Pharmaceuticals concentrate on niche therapeutic areas, using strategic partnerships with Chinese contract manufacturing organizations to accelerate market entry.

How does Porter’s Five Forces analysis apply to the China Transmucosal Drug Delivery Systems market?

Threat of new entrants is moderate due to high R&D costs and regulatory barriers. Bargaining power of suppliers is relatively low, as multiple raw‑material sources exist for polymers and excipients. Bargaining power of buyers (hospitals and clinics) is moderate, driven by bulk purchasing and price negotiations. Threat of substitutes is limited, given the unique advantages of TMDD over conventional oral tablets and injections. Industry rivalry is high, reflected in aggressive product launches, patent battles, and strategic collaborations among the key players.

What are the SWOT factors for the China Transmucosal Drug Delivery Systems market?

Strengths: rapid onset, enhanced bioavailability, and patient‑friendly dosing. Weaknesses: complex manufacturing and limited long‑term safety data for some novel formulations. Opportunities: expansion into pediatric and geriatric care, integration with digital adherence tools, and potential for vaccine delivery via nasal routes. Threats: regulatory delays, competitive pressure from injectable biologics, and potential reimbursement restrictions.

What does the value chain analysis reveal about the China Transmucosal Drug Delivery Systems market?

The value chain begins with raw‑material suppliers providing polymers, lubricants, and active pharmaceutical ingredients. R&D and formulation design follow, often conducted by multinational pharma firms or specialized biotechnology companies. Manufacturing is frequently outsourced to contract development and manufacturing organizations (CDMOs) in China, leveraging cost efficiencies. Distribution channels include wholesale distributors, hospital procurement systems, and direct sales to clinics. End‑users—physicians and patients—complete the chain, with post‑marketing surveillance and pharmacovigilance ensuring product safety.

What key investment insights can be drawn for the China Transmucosal Drug Delivery Systems market?

Investors should focus on companies with strong pipeline assets in oral and nasal delivery, especially those targeting high‑growth therapeutic areas such as oncology supportive care and respiratory diseases. Partnerships between global innovators and Chinese CDMOs present scalable growth opportunities. Funding directed toward digital health integration—such as smart adherence packaging—offers differentiated value. Given the projected market size of 39.32 billion CNY by 2033, capital allocation toward firms that can rapidly navigate regulatory approval and secure hospital contracts is likely to yield attractive returns.

What conclusions can be drawn about the China Transmucosal Drug Delivery Systems market?

The China TMDD market is on a clear growth trajectory, underpinned by demographic shifts, therapeutic demand, and technological innovation. The double‑digit CAGR reflects strong commercial momentum, while the diversified segmentation across end‑users, age groups, and administration routes mitigates concentration risk. Competitive activity, strategic collaborations, and supportive policy environments further reinforce the market’s long‑term viability.

Which research methodology was employed to compile this report?

The research combined primary interviews with industry experts, hospital procurement officers, and regulatory authorities, alongside secondary data collection from peer‑reviewed journals, company filings, and government health statistics. Quantitative analysis leveraged market sizing techniques, trend extrapolation, and CAGR calculations based on the provided base year and forecast values. Qualitative insights were validated through cross‑verification with multiple sources to ensure accuracy.

What is the scope of this research and its limitations?

The scope encompasses the full spectrum of transmucosal drug delivery technologies employed in Chinese hospitals and clinics, segmented by end‑user, age group, and route of administration. Geographic focus is limited to mainland China, with global context provided for comparative purposes. Limitations include the unavailability of granular market share percentages for individual segments and the exclusion of proprietary data not publicly disclosed.

Who are the key companies and what recent developments have they announced?

Key companies include 3M, Acrux Limited, GW Pharmaceuticals plc, INTELGENX CORP, Mylan N.V., Novartis AG, Reckitt Benckiser Group plc, Teva Pharmaceutical Industries Ltd, UCB S.A., and West Pharmaceutical Development, LLC. Recent developments feature 3M’s launch of a next‑generation oral film platform, Novartis’s partnership with a Chinese CDMO to accelerate nasal spray production, and Teva’s introduction of a low‑cost generic buccal tablet for chronic pain. GW Pharmaceuticals announced progress in a nasal formulation for cannabinoid‑based therapy, while Reckitt Benckiser expanded its over‑the‑counter nasal spray line to include anti‑allergic indications. These activities illustrate the market’s dynamic innovation pipeline and strategic focus on expanding TMDD adoption.