Virtual Reality and Augmented Reality in Retail Market Overview - Definition, scope, and significance?

Virtual Reality (VR) and Augmented Reality (AR) in retail refer to immersive technologies that enable customers to experience products and store environments digitally. VR creates a fully simulated environment, while AR overlays digital information onto the physical world. The scope of this market spans hardware devices (headsets, smart glasses), software platforms (3‑D modeling, interactive apps), and services (implementation, maintenance, analytics). Their significance lies in transforming traditional shopping into interactive, personalized experiences, reducing return rates, and opening new channels for advertising and brand storytelling.

Virtual Reality and Augmented Reality in Retail Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising consumer demand for immersive experiences, increasing smartphone penetration, and retailers’ need to differentiate in a crowded digital marketplace. The strong CAGR of 32.53% reflects confidence in technology adoption. Restraints involve high upfront costs for hardware, limited broadband bandwidth in some regions, and concerns over data privacy. Challenges center on integration with legacy e‑commerce platforms and the requirement for skilled talent. Opportunities arise from expanding applications such as try‑on solutions for apparel and beauty, AR‑enabled advertising, and the emergence of platform‑as‑a‑service models that lower entry barriers.

Virtual Reality and Augmented Reality in Retail Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature the convergence of AI with AR/VR to deliver real‑time product recommendations and hyper‑personalized ads. Retailers are increasingly adopting “virtual try‑on” solutions for jewellery and cosmetics, driven by consumer desire for contact‑less shopping. Spatial planning tools that use AR to visualize furniture in a home setting are gaining traction, supporting the furniture segment. Emerging trends include the rollout of 5G networks, which enhance streaming quality for VR experiences, and the growth of cloud‑based rendering services that reduce hardware dependency.

COVID-19 Impact on the Virtual Reality and Augmented Reality in Retail Market - Pandemic effects and recovery trajectory?

The pandemic accelerated the shift toward digital interaction as physical stores closed temporarily. Retailers sought AR tools for virtual product demos and VR showrooms to maintain engagement, leading to a surge in short‑term demand for software solutions. Although the immediate shock caused supply chain disruptions for hardware components, the recovery trajectory is strong, reflected in the robust forecast of $76.33 billion by 2033. Post‑COVID, consumers have retained an appetite for contact‑less, immersive shopping, reinforcing long‑term market momentum.

Virtual Reality and Augmented Reality in Retail Market Competitive Landscape - Major competitors and market consolidation?

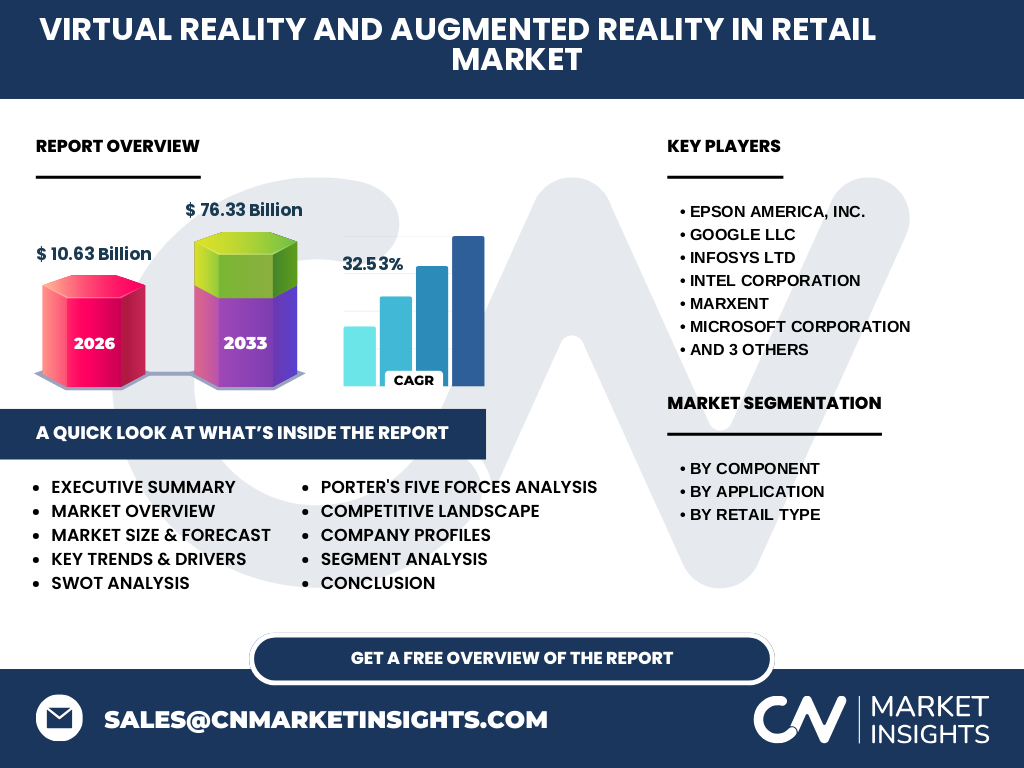

The competitive landscape features technology giants and specialized firms. Major players include Google LLC and Microsoft Corporation, which provide cloud infrastructure and mixed‑reality platforms, and Intel Corporation and Qualcomm Technologies, Inc., which supply processors for headsets. Companies such as Epson America, Inc., Marxent, and PTC Inc. focus on hardware and 3‑D content solutions, while Infosys Ltd. and Retail VR deliver implementation services. Recent consolidation trends involve strategic partnerships—e.g., hardware manufacturers integrating Qualcomm chips—to accelerate product rollout and broaden ecosystem reach.

Executive Summary - High-level overview and key findings about Virtual Reality and Augmented Reality in Retail Market?

The Virtual Reality and Augmented Reality in Retail market is poised for rapid expansion, with a 2026 valuation of $10.63 billion and a projected increase to $76.33 billion by 2033, driven by a 32.53% CAGR. Growth is powered by consumer demand for immersive shopping, advancements in AI and 5G, and expanding applications across advertising, try‑on solutions, and spatial planning. While hardware costs and integration complexities pose challenges, opportunities abound in service models and sector‑specific solutions. Leading technology providers and service integrators are forming alliances that are reshaping the competitive arena.

Virtual Reality and Augmented Reality in Retail Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 32.53%, the market is expected to maintain high‑velocity growth throughout 2025‑2032. The forecasted size of $76.33 billion for 2033 underscores a multi‑fold increase from the 2026 base. This trajectory suggests that each successive year will see a substantial uplift in both hardware shipments and software subscriptions, with services—particularly implementation and analytics— capturing an expanding share of total spend as retailers deepen their immersive capabilities.

Virtual Reality and Augmented Reality in Retail Market Size and Share by Segmentation - Breakdown by component, application, and retail type?

Segmentation analysis divides the market into three primary components: hardware, software, and services. Hardware includes headsets and smart glasses, software encompasses platform development and content creation, while services cover integration, maintenance, and consulting. Application segments comprise advertising and marketing, try‑on solutions, and planning and designing. Retail type segmentation identifies jewellery, apparel, beauty & cosmetics, and furniture as key verticals. Each segment contributes to the overall market size, with software and services expected to capture the fastest growth due to recurring revenue models.

Global Virtual Reality and Augmented Reality in Retail Market Size and Share by Region - Geographic distribution?

The market exhibits a worldwide footprint, with strong adoption in North America and Europe driven by advanced retail ecosystems and high disposable income. Asia‑Pacific is emerging rapidly, fueled by mobile penetration and aggressive retail innovation in countries such as China, Japan, and South Korea. While specific regional monetary values are not disclosed, the global outlook reflects balanced growth across these key territories, supported by regional investments in 5G infrastructure and digital commerce initiatives.

Regional Analysis of the Virtual Reality and Augmented Reality in Retail Market - Detailed regional market performance?

In North America, enterprises lead in piloting VR showrooms and AR advertising campaigns, leveraging mature cloud services from Microsoft and Google. Europe shows a strong focus on sustainability, using AR for virtual product visualization to reduce physical sampling. Asia‑Pacific demonstrates the fastest adoption rate, with retailers deploying AR try‑on apps for apparel and beauty, capitalizing on high smartphone usage. Latin America and the Middle East & Africa are in early adoption phases, but increasing internet penetration signals future growth potential.

Leading Company Profiles in the Virtual Reality and Augmented Reality in Retail Market - Industry players and strategies?

Epson America, Inc. specializes in high‑resolution projection and AR glasses for in‑store experiences. Google LLC offers ARCore and cloud‑based AI tools that enable retailers to build custom overlays. Infosys Ltd. provides end‑to‑end implementation services, integrating VR platforms with legacy ERP systems. Intel Corporation supplies processing chips that power low‑latency headsets. Marxent delivers 3‑D product modeling for furniture and apparel. Microsoft Corporation’s Mesh platform supports collaborative VR environments. PTC Inc. combines IoT data with AR to enhance product lifecycle management. Qualcomm Technologies, Inc. focuses on mobile‑first VR/AR chipsets, while Retail VR offers turnkey VR store simulations. These firms pursue strategies ranging from platform expansion and strategic alliances to vertical‑specific solutions.

Porter's Five Forces Analysis of the Virtual Reality and Augmented Reality in Retail Market - Competitive forces assessment?

• Threat of new entrants: Moderate. High capital requirements for hardware development deter many newcomers, but cloud‑based software services lower entry barriers. • Bargaining power of suppliers: High for semiconductor components, as few suppliers dominate the market. • Bargaining power of buyers: Growing, as large retailers demand customized solutions and competitive pricing. • Threat of substitutes: Low to moderate; traditional e‑commerce and 2‑D product images remain alternatives but lack immersive impact. • Rivalry among existing competitors: Intense, driven by rapid innovation cycles, strategic partnerships, and the race to secure flagship retail contracts.

SWOT Analysis of the Virtual Reality and Augmented Reality in Retail Market - Strengths, weaknesses, opportunities, threats?

Strengths: High consumer engagement, ability to reduce returns, and strong growth momentum. Weaknesses: High upfront hardware costs and limited standardization across platforms. Opportunities: Expansion into new retail verticals, AI‑driven personalization, and service‑based revenue models. Threats: Data privacy regulations, potential supply chain constraints for critical components, and rapid technology obsolescence.

Virtual Reality and Augmented Reality in Retail Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with component manufacturers (sensors, processors) supplying hardware OEMs. Next, software developers create AR/VR platforms and content libraries. System integrators and consulting firms then customize solutions for retailers, handling installation, training, and ongoing support. Finally, retailers deploy the solutions to end‑consumers, generating data that feeds back to improve AI algorithms and content updates, completing a cyclical value loop.

Key Investment Insights in the Virtual Reality and Augmented Reality in Retail Market - Strategic investment recommendations?

Investors should target companies that combine hardware expertise with scalable software platforms, as recurring revenue from services drives long‑term profitability. Partnerships between chipset providers (e.g., Qualcomm) and software firms accelerate time‑to‑market and mitigate supply risk. Early‑stage funding in AI‑enhanced AR applications for try‑on solutions offers high upside, especially within the apparel and beauty segments. Monitoring regulatory developments around data privacy will be essential for risk management.

Virtual Reality and Augmented Reality in Retail Market Conclusion - Summary and key takeaways?

The VR/AR retail market is entering a period of accelerated expansion, underpinned by a 32.53% CAGR and a forecasted rise to $76.33 billion by 2033. Consumer appetite for immersive experiences, combined with technological enablers like 5G and AI, creates a compelling growth narrative. While hardware costs and integration complexities remain, service‑centric models and sector‑specific applications provide clear pathways to overcome these barriers. Stakeholders across the ecosystem—hardware producers, software innovators, and retail adopters—stand to gain from strategic collaborations.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, integrating primary interviews with industry executives, technology partners, and retail decision‑makers, alongside secondary data from company reports, market databases, and scholarly publications. Quantitative forecasts were derived using compound annual growth rate (CAGR) calculations based on the 2026 market size of $10.63 billion and the 2027‑2033 projection of $76.33 billion. Qualitative insights were validated through triangulation across multiple sources.

Research Scope - Coverage and limitations?

The research covers global VR and AR adoption in retail, segmented by component, application, and retail type. Geographic coverage includes major regions such as North America, Europe, and Asia‑Pacific. Limitations stem from the proprietary nature of some financial disclosures, which constrains the granularity of regional revenue breakdowns. Nonetheless, the analysis captures the primary market drivers, trends, and competitive dynamics relevant to stakeholders.

Key Companies and Recent Developments in the Virtual Reality and Augmented Reality in Retail Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Epson America, Inc. recently launched a next‑generation AR glasses line aimed at in‑store navigation. Google LLC announced an expansion of its ARCore SDK to support retail‑specific spatial mapping. Infosys Ltd. secured a multi‑year contract to implement VR training simulators for a global apparel retailer. Intel Corporation introduced low‑power processors optimized for standalone VR headsets. Marxent unveiled a cloud‑based 3‑D product visualization platform for furniture retailers. Microsoft Corporation integrated its Mesh collaboration suite with retail CRM systems. PTC Inc. rolled out an AR-enabled IoT dashboard for beauty product lifecycle tracking. Qualcomm Technologies, Inc. released a new Snapdragon chipset designed for high‑resolution AR experiences on mobile devices. Retail VR announced a partnership with a leading jewellery chain to create virtual storefronts accessible via consumer smartphones.