What is the Aircraft Engine Forging Market Overview – definition, scope, and significance?

The Aircraft Engine Forging Market encompasses the production of precision‑forged components that are integral to modern jet propulsion systems. These forgings include rotor shafts, turbine discs, combustion‑chamber outer cases, fan casings and a variety of ancillary parts. The market’s scope covers all forging types—closed‑die and seamless rolled‑ring—used across commercial, military and general‑aviation aircraft, employing materials such as nickel‑based alloys, titanium, aluminum and others. Forged engine parts deliver superior strength‑to‑weight ratios, fatigue resistance and reliability, making them critical for safety‑critical aerospace applications and thus a cornerstone of the global aviation supply chain.

What are the primary drivers, restraints, challenges, and opportunities shaping the Aircraft Engine Forging Market?

Key drivers include rising demand for fuel‑efficient aircraft, expanding commercial air travel, and increased defense spending, all of which boost requirements for high‑performance engine components. Technological advances in additive manufacturing and advanced alloys also create opportunities for lighter, more durable forgings. Restraints stem from high capital intensity, stringent certification processes, and volatile raw‑material prices, especially for nickel and titanium. Challenges involve supply‑chain disruptions, skilled‑labor shortages, and the need to comply with ever‑tighter emissions regulations. Opportunities arise from retro‑fitting older fleets, growth in emerging markets, and collaboration between OEMs and forging specialists to develop next‑generation engine architectures.

What are the current growth trends in the Aircraft Engine Forging Market?

Current trends show a shift toward larger‑diameter, high‑pressure turbine discs and integrated rotor‑shaft assemblies that improve engine thrust while lowering weight. Manufacturers are increasingly adopting closed‑die forging for complex geometries and seamless rolled‑ring forging for high‑stress rings. Material trends favor nickel‑based superalloys for hot‑section parts and titanium alloys for fan casings, aligning with industry goals for higher temperature operation and corrosion resistance. Additionally, digital twins and predictive analytics are being used to optimize forging processes and reduce scrap rates.

How has COVID‑19 impacted the Aircraft Engine Forging Market and what is the recovery trajectory?

The pandemic caused a temporary dip in aircraft deliveries, leading to postponed orders for new engine forgings and a slowdown in production capacity utilization. However, the market demonstrated resilience as OEMs prioritized maintenance‑repair‑overhaul (MRO) activities, sustaining demand for replacement forgings. Recovery accelerated in 2022‑2023 with the resurgence of commercial flight activity and renewed defense procurement, positioning the market on a clear growth path aligned with the projected CAGR of 7.43 % through 2032.

Who are the major competitors in the Aircraft Engine Forging Market and how is the competitive landscape evolving?

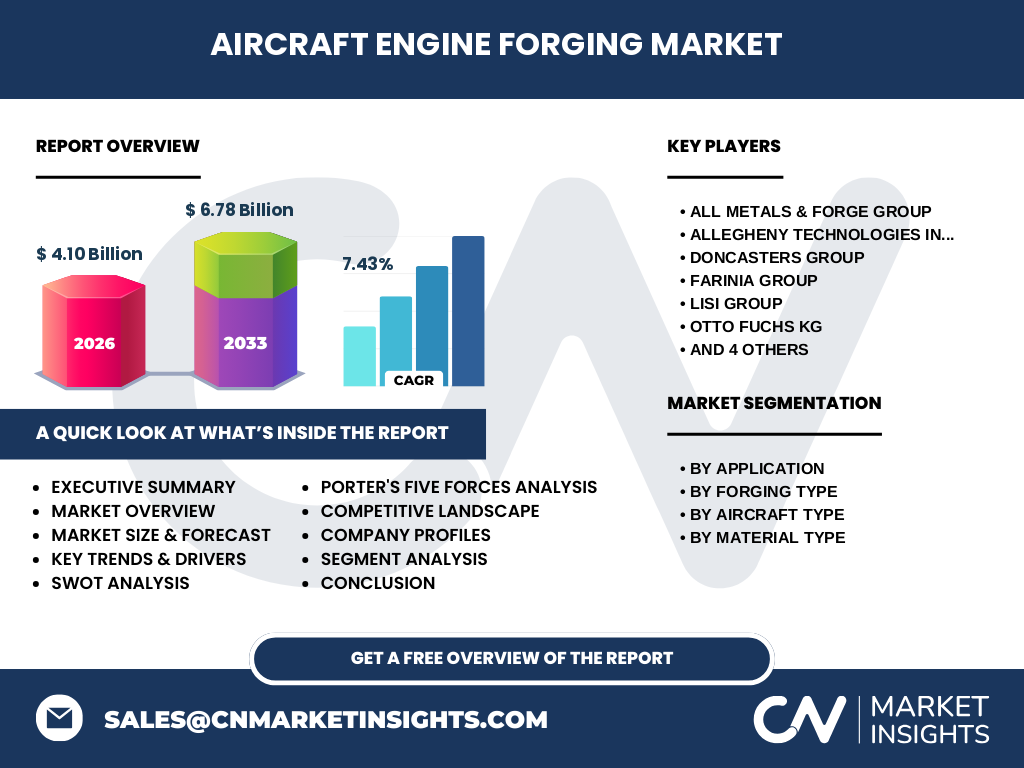

Leading players include All Metals & Forge Group, Allegheny Technologies Inc., Doncasters Group, Farinia Group, LISI GROUP, OTTO FUCHS KG, Pacific Forge Incorporated, Precision Castparts Corp., Safran SA and VSMPO‑AVISMA Corp. The competitive landscape is characterized by strategic alliances, joint ventures and selective acquisitions aimed at expanding capability portfolios and geographic reach. Consolidation is moderate, with firms focusing on enhancing high‑temperature alloy expertise and expanding service offerings such as heat‑treatment, testing and certification support.

What are the key findings presented in the Executive Summary of this market report?

The Executive Summary highlights a market size of USD 4.10 billion in 2026, with a forecast reaching USD 6.78 billion by 2033, reflecting a robust 7.43 % CAGR. Growth is driven by increased demand for fuel‑efficient engines, military modernization programs, and the adoption of advanced forging technologies. The report underscores regional expansion in Asia‑Pacific, the pivotal role of nickel‑based alloys, and the importance of strategic partnerships for sustaining competitive advantage.

What is the forecast outlook for the Aircraft Engine Forging Market from 2025 to 2032?

Based on the provided CAGR of 7.43 %, the market is expected to expand from the 2026 baseline of USD 4.10 billion to approximately USD 6.78 billion by 2033. This trajectory suggests steady demand across all application segments, with the most pronounced growth in turbine‑disc and rotor forgings for next‑generation commercial engines. Military aircraft programs will contribute a stable, high‑value niche, while general‑aviation remains a modest but consistent contributor.

How is the Aircraft Engine Forging Market sized and shared by segment?

Segmentation by application divides the market into rotor, turbine disc, combustion‑chamber outer case, fan case and others. By forging type, the market splits between closed‑die forging and seamless rolled‑ring forging. Aircraft type segmentation includes commercial, military and general aviation, while material segmentation covers nickel alloys, titanium alloys, aluminum and other materials. Each segment aligns with specific performance requirements—e.g., nickel alloys dominate turbine‑disc and rotor segments, whereas titanium is prevalent in fan‑case applications.

What is the geographic distribution of the global Aircraft Engine Forging Market?

The market exhibits a worldwide footprint, with major demand centers in North America, Europe and the Asia‑Pacific region. North America and Europe host a concentration of OEMs and forging facilities, driving significant market share. The Asia‑Pacific region is emerging rapidly due to expanding commercial fleets, increasing defense budgets and the establishment of new forging plants, positioning it as a key growth frontier.

What are the detailed regional performances in the Aircraft Engine Forging Market?

In North America, robust defense spending and legacy commercial aircraft programs sustain high demand for turbine‑disc and rotor forgings. Europe benefits from a dense network of aerospace manufacturers and a strong focus on lightweight titanium fan‑case production. Asia‑Pacific shows the fastest growth, propelled by rising passenger traffic, new aircraft orders from carriers such as China Southern and IndiGo, and government‑backed military modernization, leading to expanded forging capacity and higher material consumption.

Which leading companies are profiled and what are their strategic approaches?

Company profiles examine All Metals & Forge Group’s focus on high‑temperature nickel superalloys, Allegheny Technologies’ integrated material‑to‑part capabilities, Doncasters Group’s specialization in seamless rolled‑ring forgings, Farinia Group’s expansion into turbine‑disc production, LISI GROUP’s diversified aerospace portfolio, OTTO FUCHS KG’s precision closed‑die processes, Pacific Forge’s strategic MRO partnerships, Precision Castparts Corp.’s broad component range, Safran SA’s OEM collaborations, and VSMPO‑AVISMA Corp.’s dominance in titanium supply. Strategies commonly involve technology investment, capacity expansion and collaborative R&D with engine manufacturers.

How do Porter’s Five Forces affect the Aircraft Engine Forging Market?

Threat of new entrants is moderate due to high capital and certification barriers. Bargaining power of suppliers is relatively high, especially for specialty nickel and titanium alloys, which are limited to few producers. Bargaining power of buyers (airframe OEMs) is strong, as they demand strict quality and cost standards. Threat of substitutes remains low; alternative manufacturing such as additive printing is still emerging for high‑stress forgings. Industry rivalry is intense, with firms competing on technology, lead times and material expertise.

What are the SWOT insights for the Aircraft Engine Forging Market?

Strengths include essential role in safety‑critical engine components and advanced material expertise. Weaknesses involve high production costs and reliance on limited alloy suppliers. Opportunities arise from emerging ultra‑efficient engines, retro‑fit programs and expansion into fast‑growing Asian markets. Threats encompass supply‑chain volatility, regulatory changes regarding emissions and potential disruptive technologies that could alter traditional forging demand.

What does the value chain of the Aircraft Engine Forging Market look like?

The value chain begins with raw‑material sourcing (nickel, titanium, aluminum), followed by alloy melting and casting. Next are precision forging processes—closed‑die or seamless rolled‑ring—then heat‑treatment, machining, non‑destructive testing and coating. Final stages include certification, logistics and after‑sales support for MRO. Value‑added services such as design‑for‑forging, digital twins and predictive maintenance are increasingly integrated to enhance customer value.

What investment insights can be drawn from the Aircraft Engine Forging Market?

Investors should target companies with diversified material portfolios, strong OEM relationships and proven capabilities in both closed‑die and rolled‑ring forging. Capital allocation toward advanced metallurgy, automation and digital process monitoring yields higher margins. Geographic diversification, especially into Asia‑Pacific, offers growth upside. Partnerships with engine manufacturers for next‑generation programs provide a strategic foothold, while monitoring raw‑material contracts can mitigate cost risk.

What conclusions can be drawn about the Aircraft Engine Forging Market?

The market is on a clear upward trajectory, driven by demand for more efficient, higher‑thrust engines across commercial and military sectors. Technological innovation in forging processes and material science will sustain competitive advantage. While raw‑material supply and regulatory pressures pose challenges, strategic investments and regional expansion—particularly in Asia‑Pacific—position the market for robust growth through 2032.

How was the research for this report conducted?

Research methodology combined primary interviews with industry experts, OEMs and forging specialists, alongside secondary data from company reports, aerospace databases, and government publications. Trend analysis employed historical market performance, macro‑economic indicators and the provided financial figures (USD 4.10 billion in 2026, USD 6.78 billion forecast, 7.43 % CAGR). Findings were validated through triangulation across multiple sources to ensure reliability.

What is the scope of this research and its limitations?

The scope covers global aircraft engine forging activities, segmented by application, forging type, aircraft type and material. It includes competitive profiling of the ten listed key companies and regional analysis of major markets. Limitations arise from the reliance on publicly available data and the exclusion of confidential contract values; however, the core market size and growth projections are grounded in the supplied figures.

Which key companies and recent developments are highlighted in the Aircraft Engine Forging Market?

Key players include All Metals & Forge Group, Allegheny Technologies, Doncasters Group, Farinia Group, LISI GROUP, OTTO FUCHS KG, Pacific Forge, Precision Castparts Corp., Safran SA and VSMPO‑AVISMA Corp. Recent developments feature All Metals’ expansion of a nickel‑superalloy line, Allegheny’s acquisition of a titanium‑processing facility, Doncasters’ partnership with a European OEM for rolled‑ring turbine discs, Farinia’s entry into the fan‑case market, LISI’s launch of a digital forging monitoring platform, OTTO FUCHS’s investment in high‑speed closed‑die equipment, Pacific Forge’s MRO service agreement, Precision Castparts’ supply contract for next‑gen commercial engines, Safran’s collaborative R&D on lightweight turbine components, and VSMPO‑AVISMA’s increased titanium output for aerospace applications.