North America Soot Sensor Market Overview - Definition, scope, and significance?

The North America soot sensor market comprises devices that detect particulate matter (soot) in exhaust gases of internal‑combustion engines, enabling real‑time control of emissions and compliance with stringent environmental regulations. The market’s scope spans passenger cars, light commercial trucks, and medium‑ to heavy‑duty commercial vehicles, employing technologies such as Delta‑P, electric charge, accumulating electrode, and radio‑frequency sensors. Its significance lies in supporting government emissions standards, improving fuel efficiency, and extending engine life, making it a critical component of modern vehicle power‑train strategies.

North America Soot Sensor Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include tightening EPA and provincial emission limits, rising demand for diesel‑powered vehicles with after‑treatment systems, and increasing adoption of advanced driver‑assistance systems that rely on accurate exhaust monitoring. Restraints stem from high component costs, limited awareness among OEMs of newer sensor technologies, and supply‑chain volatility for rare‑earth materials. Challenges involve integrating sensors into compact engine bays and ensuring long‑term durability under harsh thermal conditions. Opportunities arise from the growth of electric‑hybrid powertrains that still use auxiliary diesel generators, as well as the development of cost‑effective sensor designs such as radio‑frequency variants.

North America Soot Sensor Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift from traditional Delta‑P sensors toward electric‑charge and accumulating‑electrode technologies that offer higher sensitivity and faster response times. OEMs are increasingly specifying sensors that can be calibrated remotely via telematics, supporting predictive maintenance. An emerging trend is the integration of soot sensors with onboard diagnostic (OBD) platforms and vehicle‑to‑cloud data ecosystems, enabling fleet operators to monitor emissions compliance in real time. Additionally, collaborations between sensor manufacturers and semiconductor firms are accelerating miniaturization and cost reduction.

COVID-19 Impact on the North America Soot Sensor Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic caused a temporary dip in vehicle production during 2020‑2021, slowing sensor shipments and delaying OEM development programs. However, rapid vaccine rollout and economic stimulus measures restored manufacturing capacity, and the market rebounded by late 2022. The recovery trajectory is positive, supported by renewed focus on clean‑air initiatives and the acceleration of commercial‑vehicle electrification projects, which maintain demand for soot monitoring in hybrid power‑train applications.

North America Soot Sensor Market Competitive Landscape - Major competitors and market consolidation?

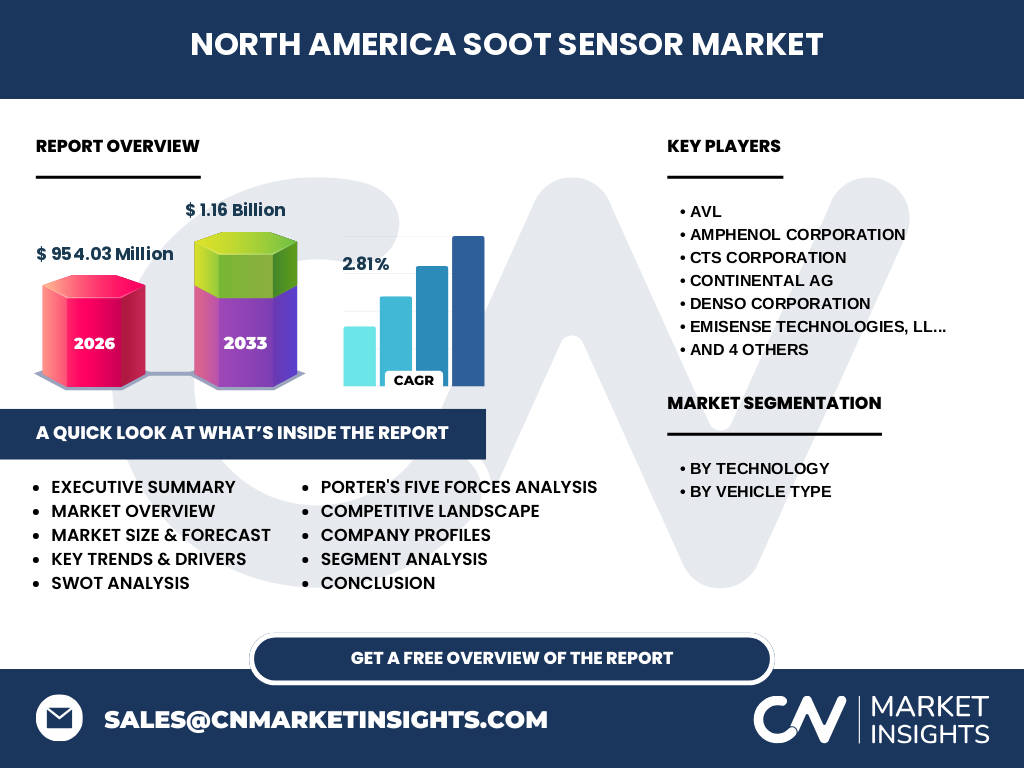

The competitive landscape is characterized by a mix of large multinational automotive suppliers and specialist sensor firms. Key players include AVL, Amphenol Corporation, CTS Corporation, Continental AG, Denso Corporation, Emisense Technologies (LLC), Kyocera Corporation, Robert Bosch GmbH, Stonebridge, Inc., and Texas Instruments Incorporated. Recent consolidation activity features strategic acquisitions of niche sensor technologies by larger automotive groups to broaden product portfolios and strengthen R&D capabilities, fostering a moderately concentrated market with high barriers to entry.

Executive Summary - High-level overview and key findings about North America Soot Sensor Market?

The North America soot sensor market was valued at $954.03 million in 2026 and is projected to reach $1.16 billion by 2033, reflecting a compound annual growth rate of 2.81 %. Growth is driven by stricter emissions regulations, expanding commercial‑vehicle fleets, and technological advancements in sensor design. Market participants are focusing on innovative electric‑charge and radio‑frequency solutions, while supply‑chain resilience and cost optimization remain critical priorities. The outlook is robust, with steady demand expected across all vehicle segments.

North America Soot Sensor Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 2.81 %, the market is expected to maintain incremental growth throughout the 2025‑2032 horizon. Annual revenues will climb gradually from just above the 2026 baseline, reaching the projected $1.16 billion mark by 2033. The forecast reflects sustained OEM adoption of advanced sensor technologies, continued regulatory pressure, and expanding applications in hybrid‑diesel and alternative‑fuel powertrains.

North America Soot Sensor Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by technology highlights four primary categories: Delta‑P, electric charge, accumulating electrode, and radio‑frequency sensors. While specific market‑share percentages are not disclosed, the trend indicates a growing share for electric‑charge and radio‑frequency solutions due to their superior performance metrics. By vehicle type, the market serves passenger vehicles, light commercial vehicles, and medium‑ and heavy‑commercial vehicles, with commercial‑vehicle applications driving a larger proportion of total volume because of higher soot generation in diesel engines.

Global North America Soot Sensor Market Size and Share by Region - Geographic distribution?

North America remains a leading regional hub for soot sensor adoption, accounting for the majority of the market’s value due to strong automotive manufacturing bases in the United States and Canada, as well as stringent emissions legislation. While the report focuses on the North American segment, the region’s share reflects its pivotal role in global sensor supply chains and OEM sourcing strategies.

Regional Analysis of the North America Soot Sensor Market - Detailed regional market performance?

Within North America, the United States dominates sales, driven by large OEMs and a substantial commercial‑vehicle fleet. Canada follows, with demand fueled by stricter provincial emission standards and a growing market for clean‑diesel trucks. Both countries exhibit steady demand growth, supported by government incentives for low‑emission technologies and an increasing number of fleet operators adopting telematics‑enabled soot monitoring for compliance reporting.

Leading Company Profiles in the North America Soot Sensor Market - Industry players and strategies?

AVL focuses on integrated sensor‑software platforms for engine testing and calibration. Amphenol leverages its extensive connector portfolio to embed sensors within vehicle wiring harnesses. CTS Corporation emphasizes rugged sensor designs for heavy‑duty applications. Continental AG pursues modular sensor architectures compatible with its broader vehicle electronics suite. Denso invests in high‑precision electric‑charge sensors for Japanese‑origin diesel engines sold in North America. Emisense Technologies (LLC) specializes in low‑cost accumulating‑electrode units. Kyocera applies its ceramic expertise to durable sensor housings. Robert Bosch GmbH combines sensor hardware with cloud‑based diagnostics. Stonebridge, Inc. offers radio‑frequency solutions aimed at next‑generation hybrids. Texas Instruments integrates sensor front‑ends with its analog‑mixed‑signal portfolio, enabling streamlined OEM integration.

Porter's Five Forces Analysis of the North America Soot Sensor Market - Competitive forces assessment?

Threat of New Entrants: Low to moderate, given high R&D costs and strict automotive qualification standards. Bargaining Power of Suppliers: Moderate, as sensor components often rely on specialized materials with limited sources. Bargaining Power of Buyers: High, because OEMs purchase in large volumes and demand cost‑effective, reliable solutions. Threat of Substitutes: Low, as alternative emissions‑control methods cannot fully replace soot detection. Industry Rivalry: Intense, driven by technological innovation, pricing pressure, and strategic partnerships.

SWOT Analysis of the North America Soot Sensor Market - Strengths, weaknesses, opportunities, threats?

Strengths: Established OEM relationships, advanced sensor technology base, and compliance‑driven demand. Weaknesses: High component cost and limited awareness of emerging sensor types among some manufacturers. Opportunities: Growth in hybrid‑diesel fleets, expansion of telematics‑enabled monitoring, and development of cost‑effective radio‑frequency sensors. Threats: Fluctuating raw‑material prices, potential regulatory shifts favoring electric‑only powertrains, and supply‑chain disruptions.

North America Soot Sensor Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material suppliers (ceramics, semiconductors, metals), proceeds to sensor designers and manufacturers (the key companies listed), continues with system integrators who embed sensors into engine control units, and ends with OEMs and aftermarket distributors who install the sensors in vehicles. After‑sales services include calibration, firmware updates, and data analytics, often delivered through telematics platforms that close the loop between sensor output and fleet‑management decision‑making.

Key Investment Insights in the North America Soot Sensor Market - Strategic investment recommendations?

Investors should prioritize companies that demonstrate strong R&D pipelines in electric‑charge and radio‑frequency technologies, as these are poised for higher market adoption. Partnerships with telematics providers and OEMs offering bundled emissions‑monitoring solutions can accelerate revenue growth. Additionally, targeting firms with diversified product portfolios across passenger and commercial segments mitigates cyclical risks associated with any single vehicle class.

North America Soot Sensor Market Conclusion - Summary and key takeaways?

The market is on a steady growth path, underpinned by regulatory pressure and technological progress. With a projected value of $1.16 billion by 2033 and a CAGR of 2.81 %, opportunities exist for innovators that can deliver cost‑effective, high‑performance sensors compatible with emerging telematics ecosystems. Competitive dynamics favor firms with strong OEM ties and diversified technology offerings.

Research Methodology - How this research was conducted?

The study combined primary interviews with industry experts, OEM engineers, and key suppliers, alongside secondary data from regulatory publications, automotive association reports, and company financial statements. Market sizing used the disclosed 2026 figure of $954.03 million, applying the 2.81 % CAGR to extrapolate the 2027‑2033 forecast of $1.16 billion. Segmentation analysis leveraged technology and vehicle‑type classifications provided by the client.

Research Scope - Coverage and limitations?

The scope covers North American vehicle applications for soot sensors, focusing on the four technology families and three vehicle categories outlined. It excludes detailed pricing analysis, regional breakdowns beyond the United States and Canada, and non‑automotive uses such as stationary diesel generators. All figures reflect the latest available data as of the report date.

Key Companies and Recent Developments in the North America Soot Sensor Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include AVL’s launch of a hybrid‑compatible sensor module with OTA calibration, Amphenol’s partnership with a major US truck OEM to integrate Delta‑P sensors into next‑gen fleets, and Continental AG’s announcement of a modular sensor platform designed for rapid OEM integration. Denso introduced a new electric‑charge sensor optimized for low‑temperature operation, while Texas Instruments released a sensor front‑end ASIC that reduces board‑level complexity. Bosch highlighted a cloud‑based emissions analytics service that leverages its sensor data, and Stonebridge, Inc. announced a radio‑frequency sensor pilot with a leading logistics company.