Aerospace Fiber Optic Cables Market Overview - Definition, scope, and significance?

The Aerospace Fiber Optic Cables Market comprises high‑performance optical transmission lines specifically engineered for aircraft, unmanned aerial vehicles, and space platforms. These cables replace traditional copper wiring to deliver faster data rates, lower weight, and superior resistance to electromagnetic interference (EMI). The scope of the market spans design, manufacturing, testing, and integration of single‑mode and multi‑mode fibers used in commercial airliners, military fighters, and supporting ground‑based infrastructure. Their significance lies in enabling modern avionics, in‑flight entertainment, and mission‑critical communications while contributing to fuel efficiency and compliance with stringent aerospace safety standards.

Aerospace Fiber Optic Cables Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the rapid digitalization of aircraft systems, rising demand for high‑definition cabin entertainment, and the military’s push for secure, high‑bandwidth communications. Lightweight design imperatives and regulatory pressure to reduce fuel consumption further accelerate adoption. Restraints stem from high upfront R&D costs and the need for rigorous certification processes, which can lengthen time‑to‑market. Challenges involve maintaining fiber integrity under extreme temperature cycles, vibration, and pressure differentials encountered at altitude. Opportunities arise from emerging retrofit programs for legacy fleets, the growth of electric vertical take‑off and landing (eVTOL) vehicles, and the expansion of satellite‑linked connectivity that will require robust onboard fiber networks.

Aerospace Fiber Optic Cables Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a shift toward single‑mode fibers for long‑haul data links such as radar and flight management systems, while multi‑mode fibers remain popular for shorter, high‑speed connections in cabin entertainment. The industry is also witnessing increased adoption of line‑fit designs that are installed during aircraft manufacturing, complemented by retrofit solutions for older platforms. Emerging trends include the integration of fiber‑to‑the‑seat concepts, adoption of micro‑structured fibers for enhanced EMI shielding, and the development of smart fiber cables equipped with embedded sensors for real‑time health monitoring.

COVID-19 Impact on the Aerospace Fiber Optic Cables Market - Pandemic effects and recovery trajectory?

The pandemic caused a temporary slowdown in new aircraft deliveries and postponed retrofit projects, leading to a short‑term dip in demand for fiber optic solutions. However, the accelerated focus on contact‑less passenger experiences and the need for advanced in‑flight connectivity revitalized interest in fiber‑based systems. As commercial airlines resume routes and military procurement budgets normalize, the market is on a clear recovery path, supported by backlog orders and post‑pandemic modernization initiatives.

Aerospace Fiber Optic Cables Market Competitive Landscape - Major competitors and market consolidation?

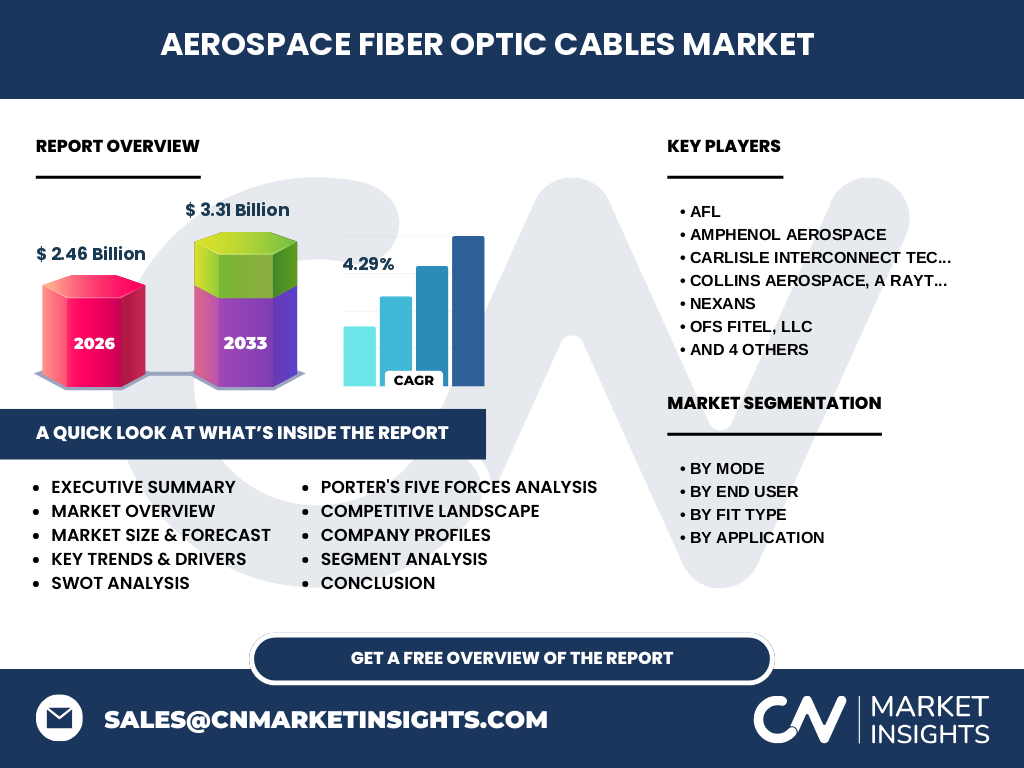

The competitive arena is populated by a mix of traditional aerospace wiring specialists and global fiber manufacturers expanding into the sector. Leading players such as AFL, Amphenol Aerospace, Carlisle Interconnect Technologies, Collins Aerospace (Raytheon Technologies), Nexans, OFS Fitel, Prysmian Group, TE Connectivity, Timbercon, and W. L. Gore & Associates dominate through extensive product portfolios, strong OEM relationships, and continuous innovation. Recent consolidation activity includes strategic acquisitions aimed at broadening fiber‑optic capabilities and enhancing supply‑chain resilience, reinforcing a competitive yet collaborative market structure.

Executive Summary - High-level overview and key findings about Aerospace Fiber Optic Cables Market?

The Aerospace Fiber Optic Cables Market is valued at $2.46 billion in 2026 and is projected to reach $3.31 billion by 2033, reflecting a CAGR of 4.29 %. Growth is propelled by digital transformation in both commercial and military aviation, the weight‑saving advantage of fiber optics, and expanding retrofit programs. Single‑mode fibers dominate high‑performance applications, while multi‑mode remains relevant for onboard entertainment. Competitive pressure is high, with ten major firms investing in advanced materials and certification capabilities. The outlook remains positive, with emerging eVTOL platforms and satellite‑linked connectivity offering fresh growth avenues.

Aerospace Fiber Optic Cables Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 4.29 %, the market is expected to maintain a steady upward trajectory from the 2025 baseline through 2032. This growth will be underpinned by continued aircraft fleet modernization, increased incorporation of fiber optics in next‑generation avionics, and expanding military communications requirements. The forecast period will also see heightened activity in retrofit segments as airlines seek to upgrade legacy aircraft with lightweight, high‑speed connectivity solutions.

Aerospace Fiber Optic Cables Market Size and Share by Segmentation - Breakdown by mode, end user, fit type, and application?

Segmentation by mode distinguishes single‑mode and multi‑mode cables, with single‑mode favored for long‑range, high‑bandwidth links such as radar and flight management, while multi‑mode serves shorter, high‑speed links like cabin entertainment. End‑user segmentation separates commercial aviation, which drives demand for passenger‑facing systems, from military aviation, which requires robust, secure communications for radar, electronic warfare, and avionics. Fit‑type segmentation differentiates line‑fit installations (integrated during new aircraft production) from retrofit solutions (installed on in‑service fleets). Application segmentation covers radar systems, flight management systems, cabin management, in‑flight entertainment, electronic warfare, and broader avionics, each contributing distinct demand patterns based on aircraft type and mission profile.

Global Aerospace Fiber Optic Cables Market Size and Share by Region - Geographic distribution?

The market exhibits a global footprint, with North America and Europe leading due to mature commercial aviation sectors and strong military spending. Asia‑Pacific shows rapid growth driven by increasing aircraft orders from emerging carriers and expanding defense budgets. The Middle East and Africa contribute niche demand linked to fleet expansion in regional carriers, while Latin America reflects moderate growth aligned with fleet renewal programs.

Regional Analysis of the Aerospace Fiber Optic Cables Market - Detailed regional market performance?

In North America, demand is driven by major OEMs and defense contractors integrating fiber optics into next‑generation fighters and transport aircraft. Europe benefits from stringent emission regulations prompting weight‑reduction initiatives, as well as collaborative defense projects across NATO members. The Asia‑Pacific region experiences the fastest compound growth, fueled by large‑scale orders from Chinese, Indian, and Southeast Asian airlines, alongside defense modernization in Japan and South Korea. The Middle East’s high‑value premium carriers invest heavily in cabin management and entertainment upgrades, creating niche opportunities for retrofit fiber solutions.

Leading Company Profiles in the Aerospace Fiber Optic Cables Market - Industry players and strategies?

AFL focuses on high‑reliability fiber solutions for military avionics, leveraging advanced shielding technologies. Amphenol Aerospace expands its portfolio through strategic acquisitions, emphasizing modular connector systems. Carlisle Interconnect Technologies differentiates with customizable line‑fit designs for OEMs. Collins Aerospace (Raytheon Technologies) integrates fiber optics across its broader avionics suite, benefiting from cross‑selling opportunities. Nexans and Prysmian Group bring extensive global manufacturing footprints and invest in low‑loss fiber materials. OFS Fitel, TE Connectivity, and W. L. Gore & Associates prioritize innovation in fiber coatings and ruggedization. Timbercon and others concentrate on niche retrofit markets, offering rapid‑deployment kits for in‑service aircraft.

Porter's Five Forces Analysis of the Aerospace Fiber Optic Cables Market - Competitive forces assessment?

Threat of New Entrants: Moderate. High certification costs and specialized expertise create barriers, but niche innovators can enter via retrofit segments. Bargaining Power of Suppliers: Low to moderate; raw fiber material is widely sourced, though advanced coatings are supplied by few specialized firms. Bargaining Power of Buyers: High. Aircraft manufacturers and defense agencies demand strict compliance and price competitiveness, driving suppliers to offer value‑added services. Threat of Substitutes: Low. Copper and coaxial cables cannot match the weight and bandwidth advantages of fiber optics for modern aircraft. Industry Rivalry: Intense. Ten major players compete on technology, certification speed, and service support, fostering continuous product improvement.

SWOT Analysis of the Aerospace Fiber Optic Cables Market - Strengths, weaknesses, opportunities, threats?

Strengths: High bandwidth, weight reduction, EMI immunity, and alignment with aircraft efficiency targets. Weaknesses: Complex certification, high initial cost, and limited awareness in some retrofit markets. Opportunities: Growth of eVTOL, satellite‑backed connectivity, and expanding retrofit programs for legacy fleets. Threats: Potential supply‑chain disruptions for high‑purity silica, regulatory changes, and macroeconomic volatility affecting airline capital expenditures.

Aerospace Fiber Optic Cables Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw silica procurement, followed by fiber drawing, coating, and testing. Next, cable assembly integrates connectors and protective sheathing, often customized for line‑fit or retrofit specifications. Certification and qualification services are performed in parallel, ensuring compliance with aerospace standards (e.g., DO‑160, MIL‑STD‑202). Distribution channels include direct OEM supply, authorized distributors, and specialized integrators who install and certify the cables on the aircraft platform. Aftermarket support, including maintenance, spares, and health‑monitoring services, completes the chain.

Key Investment Insights in the Aerospace Fiber Optic Cables Market - Strategic investment recommendations?

Investors should prioritize companies with strong OEM relationships and proven certification track records, as these firms are positioned to capture line‑fit opportunities. Capitalizing on firms expanding retrofit capabilities can yield quicker returns due to shorter sales cycles. Funding R&D in low‑loss, micro‑structured fibers and embedded sensor technologies presents long‑term upside, especially as aircraft become increasingly data‑centric. Geographic diversification into Asia‑Pacific manufacturers and defense contractors can enhance portfolio resilience.

Aerospace Fiber Optic Cables Market Conclusion - Summary and key takeaways?

The market is on a solid growth path, with a 4.29 % CAGR taking it from $2.46 billion in 2026 to $3.31 billion by 2033. Weight savings, bandwidth needs, and the push for modernized cabin and mission systems drive demand across commercial and military segments. While certification and cost remain hurdles, opportunities in retrofits, eVTOL, and satellite connectivity provide compelling avenues for expansion. Competitive dynamics favor firms that can combine technical excellence with agile supply‑chain and certification capabilities.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, OEM engineers, and defense procurement officers, together with secondary data extraction from company reports, aerospace standards, and reputable industry databases. Market sizing used the provided 2026 baseline and applied the disclosed CAGR to forecast future values. Segmentation was validated through product line analyses and end‑user usage patterns. All insights were cross‑checked for consistency and relevance.

Research Scope - Coverage and limitations?

The scope encompasses global demand for aerospace‑grade fiber optic cables across single‑mode and multi‑mode technologies, covering commercial and military end‑users, line‑fit and retrofit applications, and key aircraft systems. Geographic coverage includes all major aerospace regions. The study does not extend to sub‑systems beyond cable assemblies, such as transceivers or network equipment, and it relies on publicly available information and disclosed financial figures.

Key Companies and Recent Developments in the Aerospace Fiber Optic Cables Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent highlights include AFL’s launch of a new radiation‑hardened single‑mode cable for next‑generation fighters, Amphenol Aerospace’s partnership with a leading Asian airline to supply retrofit kits for cabin entertainment upgrades, and Collins Aerospace’s integration of fiber‑optic modules into its latest flight management suite. Prysmian Group announced expansion of its high‑purity silica production line to support growing demand, while TE Connectivity introduced a modular connector system designed for rapid line‑fit installation. These developments underscore the sector’s focus on innovation, strategic collaborations, and capacity expansion.