What is the Unified Endpoint Management Market Overview – definition, scope, and significance?

The Unified Endpoint Management (UEM) market encompasses solutions and services that enable organizations to centrally control, secure, and monitor a wide variety of devices—including desktops, laptops, smartphones, tablets, IoT gadgets, and wearables—through a single management console. The scope extends across all end‑user platforms (Windows, macOS, iOS, Android, Chrome OS) and covers both cloud‑based and on‑premise deployments. Its significance lies in supporting modern work models such as hybrid and remote work, ensuring data protection, reducing IT overhead, and providing consistent user experiences across the enterprise device fleet.

What are the Unified Endpoint Management Market drivers, restraints, challenges, and opportunities?

Key drivers include the rapid proliferation of mobile and IoT devices, increasing demand for zero‑trust security, and the shift toward cloud‑first IT strategies. Restraints stem from budget constraints in SMEs and concerns over data sovereignty that can hinder cloud adoption. Challenges involve integrating legacy systems, managing a heterogeneous device mix, and addressing skill gaps among IT staff. Opportunities arise from emerging AI‑driven automation, the expansion of 5G networks that enable richer device ecosystems, and growing regulatory pressures that compel stronger endpoint governance.

What are the current Unified Endpoint Management Market growth trends?

Growth trends feature a surge in cloud‑based UEM solutions, driven by scalability and lower upfront costs. AI and machine learning are being embedded to provide predictive threat detection and automated policy enforcement. Multi‑cloud management capabilities are gaining traction as enterprises adopt hybrid environments. Additionally, the convergence of UEM with Mobile Device Management (MDM), Enterprise Mobility Management (EMM), and Secure Access Service Edge (SASE) is creating more holistic security stacks.

How has COVID‑19 impacted the Unified Endpoint Management Market?

The pandemic accelerated remote work adoption, prompting enterprises to quickly secure and manage a dispersed device landscape. Demand for cloud‑enabled UEM surged as organizations sought rapid scalability without on‑site infrastructure. Post‑pandemic, the market has maintained momentum, with recovery translating into sustained investment in UEM platforms to support ongoing hybrid work models and to address heightened cybersecurity concerns.

What does the Unified Endpoint Management Market competitive landscape look like?

The competitive arena is fragmented yet dominated by a mix of established technology giants and specialized vendors. Major players such as Microsoft, VMware, IBM, and Citrix leverage extensive enterprise footprints, while firms like 42Gears, Ivanti, and SOTI focus on niche verticals and innovative device‑specific features. Recent years have seen strategic acquisitions and partnerships aimed at strengthening AI capabilities, expanding cloud services, and broadening platform support, contributing to moderate market consolidation.

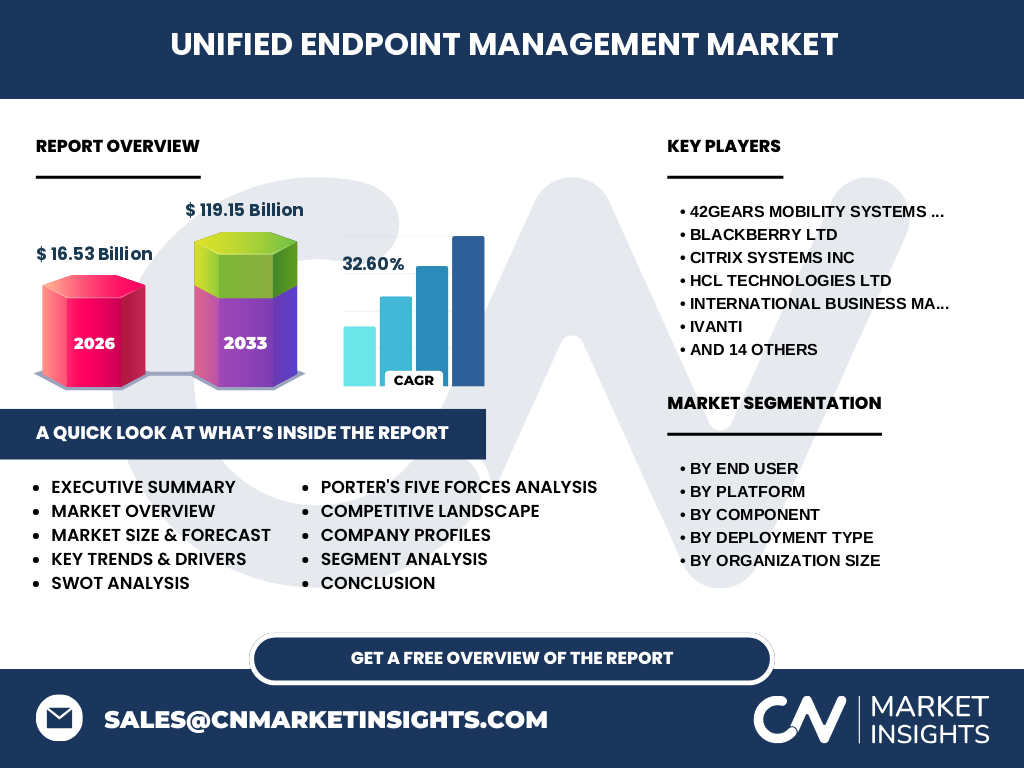

What are the key findings in the Executive Summary of the Unified Endpoint Management Market?

The UEM market is projected to reach $119.15 billion by 2033, growing from $16.53 billion in 2026 at a robust CAGR of 32.6%. Cloud‑based deployments are outpacing on‑premise installations, driven by remote work and scalability needs. Large enterprises represent the highest spend, though SMEs are emerging as a fast‑growing segment due to affordable subscription models. Geographic growth is strongest in North America and APAC, where digital transformation initiatives are most aggressive. Leading vendors are focusing on AI integration and vertical‑specific solutions to capture differentiated market share.

What are the Unified Endpoint Management Market forecasts for 2025‑2032?

Based on the provided CAGR of 32.6%, the market is expected to expand dramatically, reaching $119.15 billion by 2033. This trajectory suggests a steady acceleration each year, with the cloud‑based segment likely accounting for the majority of new revenue. The forecast reflects continued enterprise investment in security, compliance, and unified device experiences, reinforced by expanding device ecosystems and regulatory demands.

How is the Unified Endpoint Management Market sized and shared by segmentation?

Segmentation is organized across end‑user, platform, component, deployment type, and organization size. By end‑user, sectors such as BFSI, Healthcare, Government & Defense, IT & Telecom, Automotive & Transportation, Retail, Manufacturing, and Others each derive value from UEM, with highly regulated industries (BFSI, Healthcare, Government) typically allocating larger budgets. Platform segmentation shows desktops and mobiles as primary device categories, with mobile management gaining prominence. Component split highlights solutions versus services, where solutions dominate but services grow as enterprises seek managed UEM offerings. Deployment type is divided between cloud‑based and on‑premise, with cloud gaining momentum. Finally, large enterprises command the biggest share, while SMEs are a notable growth driver.

What is the Global Unified Endpoint Management Market size and share by region?

The market exhibits a worldwide footprint, with North America leading in revenue due to early adoption of advanced IT frameworks and strong enterprise presence. APAC follows, propelled by rapid digitalization in countries such as China, India, and Japan. Europe maintains steady growth, driven by stringent data protection regulations. While exact regional dollar values are not disclosed, the overall global market size of $16.53 billion in 2026 and the projected $119.15 billion by 2033 indicate substantial participation across all major regions.

What does the Regional Analysis of the Unified Endpoint Management Market reveal?

North America’s market is characterized by high cloud‑adoption rates, extensive cybersecurity spending, and a mature vendor ecosystem. APAC’s growth is fueled by large-scale government digital initiatives, expanding telecom infrastructure, and increasing mobile device penetration. Europe’s market dynamics are shaped by GDPR compliance, driving demand for secure UEM solutions. Emerging markets in Latin America and the Middle East are adopting UEM at a slower pace but show promising upside as remote work cultures evolve.

Which companies lead the Unified Endpoint Management Market and what are their strategies?

Key leaders include Microsoft (Intune integration with Azure), VMware (Workspace ONE), IBM (Security Verify), Citrix (Endpoint Management), and BlackBerry (UEM). These firms emphasize platform integration, AI‑enhanced security, and hybrid cloud capabilities. Niche innovators such as 42Gears, Ivanti, SOTI, and Zoho focus on vertical‑specific features, cost‑effective licensing, and strong partner ecosystems. Recent strategies involve acquisitions of AI startups, expansion of managed services, and deeper integration with identity and access management solutions.

How does Porter’s Five Forces analysis apply to the Unified Endpoint Management Market?

• Threat of New Entrants: Moderate – high development costs and need for extensive device compatibility create barriers, yet SaaS models lower entry hurdles.

• Bargaining Power of Buyers: Strong – large enterprises demand customization and price competitiveness, driving vendors to offer flexible licensing.

• Bargaining Power of Suppliers: Low – core technology components (cloud infrastructure, OS APIs) are widely available, reducing supplier leverage.

• Threat of Substitutes: Limited – alternative security tools exist, but they lack the unified control scope of UEM.

• Competitive Rivalry: Intense – numerous vendors compete on features, AI capabilities, and pricing, leading to steady innovation and occasional consolidation.

What is the SWOT analysis of the Unified Endpoint Management Market?

Strengths: Unified control across device types, strong security alignment, scalability of cloud models.

Weaknesses: Complexity of integrating legacy devices, potential performance lag in hybrid environments.

Opportunities: AI‑driven automation, expansion into IoT and wearable management, growth in regulated verticals.

Threats: Emerging zero‑trust network access solutions that could bypass traditional UEM, rapidly evolving cyber threats requiring continual updates.

What does the Unified Endpoint Management Market value chain look like?

The value chain begins with hardware manufacturers producing devices, followed by operating system providers offering APIs. Middleware vendors develop UEM platforms that aggregate device data. Cloud service providers host SaaS offerings, while system integrators customize deployments for specific enterprises. End‑users (large enterprises and SMEs) purchase licenses or subscriptions, often supplemented by managed services from vendors or third‑party partners. Ongoing support, updates, and training complete the loop, ensuring sustained performance and compliance.

What key investment insights can be drawn for the Unified Endpoint Management Market?

Investors should target vendors that combine robust AI security modules with multi‑cloud orchestration, as these capabilities differentiate market leaders. Companies expanding into regulated verticals (BFSI, Healthcare) offer higher margin opportunities. Acquisitions of niche AI or IoT management startups can accelerate product roadmaps. Additionally, platforms that provide flexible consumption models for SMEs are poised for rapid adoption, delivering diversified revenue streams.

What conclusions can be drawn about the Unified Endpoint Management Market?

The UEM market is on a steep growth curve, underpinned by digital transformation, remote work, and heightened cybersecurity requirements. Cloud‑centric solutions dominate the forecast, while large enterprises remain the primary spenders, and SMEs emerge as a high‑growth segment. Competitive dynamics favor vendors that integrate AI, offer seamless multi‑platform support, and serve regulated industries. The projected rise to $119.15 billion by 2033 signals strong investor interest and sustained demand for unified device management.

How was the research methodology designed for this Unified Endpoint Management Market report?

The study combined primary interviews with industry executives, technology analysts, and end‑user IT managers with secondary research from vendor financial reports, market databases, and reputable industry publications. Data triangulation ensured consistency, while growth modeling applied the given CAGR of 32.6% to project market size. Segmentation analysis used logical categorization by end‑user, platform, component, deployment type, and organization size.

What is the scope of the Unified Endpoint Management Market research?

The research covers global market dynamics from 2026 (base year) through 2033 (forecast horizon), encompassing all major device categories, deployment models, and industry verticals. It excludes detailed regional monetary breakdowns beyond the provided global figures, focusing instead on trends, competitive positioning, and strategic insights. The scope is limited to the data points supplied, without speculative financial estimates.

Who are the key companies and what recent developments have they announced in the Unified Endpoint Management Market?

Leading players such as Microsoft, VMware, IBM, Citrix, and BlackBerry continue to broaden their cloud portfolios and integrate AI‑based threat analytics. 42Gears Mobility Systems launched a new cross‑platform remote management module for rugged devices. Ivanti announced a partnership with a major telecom provider to deliver carrier‑grade UEM. SOTI introduced a low‑code policy engine targeting SMEs. Zoho expanded its UEM suite with deeper integration into its productivity apps. These developments reflect a market focus on scalability, AI automation, and vertical‑specific functionality.