North America Military Protective Eyewear Market Overview - Definition, scope, and significance?

The North America Military Protective Eyewear Market comprises specialized optical devices designed to safeguard soldiers and paramilitary personnel against kinetic, ballistic, laser, and environmental hazards encountered in combat and training environments. The market scope includes the full product lifecycle—from design, material selection, and manufacturing to distribution and end‑use by armed forces across the United States and Canada. Its significance stems from the critical role eyewear plays in preserving vision, reducing casualty rates, and maintaining operational readiness, all of which are strategic priorities for defense ministries.

North America Military Protective Eyewear Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising defense budgets, modernization programs that prioritize soldier survivability, and increasing demand for lightweight, high‑performance lenses that meet stringent ballistic standards. Opportunities arise from advances in nanocoatings, smart‑glass technology, and integration of heads‑up displays. Primary restraints are high unit costs and lengthy certification processes, while challenges involve supply‑chain disruptions for specialty polymers and the need to balance protection with ergonomic comfort for prolonged wear.

North America Military Protective Eyewear Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a shift toward multi‑threat eyewear that simultaneously addresses ballistic, laser, and chemical threats, reducing the number of separate devices a soldier must carry. Emerging trends include the incorporation of augmented‑reality (AR) overlays for target acquisition and situational awareness, as well as the adoption of 3D‑printed frames that allow rapid customization for fit and mission‑specific requirements. Sustainability considerations are also prompting manufacturers to explore recyclable polymer blends.

COVID-19 Impact on the North America Military Protective Eyewear Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic temporarily slowed production due to factory shutdowns and constrained logistics, leading to short‑term inventory shortages for training units. However, defense spending remained resilient, and the pandemic underscored the importance of protective gear, accelerating interest in antimicrobial lens coatings. By 2022, the market entered a recovery phase, with demand rebounding as armed forces resumed large‑scale training exercises and procurement cycles returned to pre‑pandemic momentum.

North America Military Protective Eyewear Market Competitive Landscape - Major competitors and market consolidation?

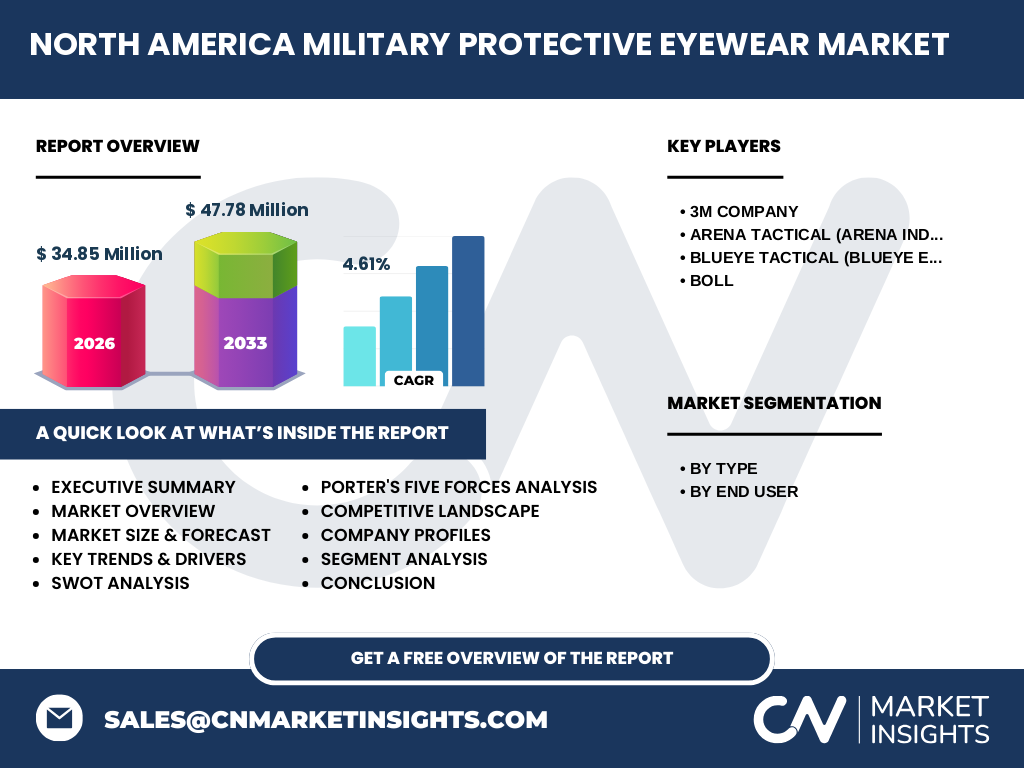

The competitive landscape is dominated by a handful of established manufacturers such as 3M Company, Arena Tactical (Arena Industries, LLC), Blueye Tactical (Blueye Eyewear Pty Ltd.), and Boll. These firms compete on technology leadership, material innovation, and contract wins with defense agencies. Recent years have seen modest consolidation, with larger players acquiring niche firms to broaden their product portfolios and gain access to specialized coating technologies, thus intensifying competition for multi‑threat solutions.

Executive Summary - High-level overview and key findings about North America Military Protective Eyewear Market?

The North America Military Protective Eyewear Market is valued at 34.85 million units in 2026 and is projected to reach 47.78 million units by 2033, reflecting a CAGR of 4.61 %. Growth is driven by heightened defense spending, modernization initiatives, and a clear shift toward integrated, multi‑threat eyewear. Leading companies are investing in advanced lens coatings and smart‑glass capabilities, while the sector remains resilient post‑COVID‑19, with procurement pipelines firmly re‑established.

North America Military Protective Eyewear Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 4.61 %, the market is expected to expand steadily from the 2026 baseline of 34.85 million units to approximately 47.78 million units by 2033. This trajectory suggests consistent annual growth, supported by ongoing defense budget allocations, upcoming replacement cycles for legacy eyewear, and the rollout of next‑generation protective technologies across both the United States and Canadian armed forces.

North America Military Protective Eyewear Market Size and Share by Segmentation - Breakdown by {segmentData}?

Segmentation by type shows three primary categories: Safety Eyewear, Ballistic Protection Eyewear, and Laser Protection Eyewear. Ballistic Protection Eyewear holds the largest share because it fulfills the core survivability requirement for frontline troops. Safety Eyewear accounts for a smaller, but growing slice as training environments demand lightweight protection. Laser Protection Eyewear, although niche, is expanding rapidly due to the increased deployment of directed‑energy weapons in modern conflict scenarios.

Global North America Military Protective Eyewear Market Size and Share by Region - Geographic distribution?

Geographically, the United States dominates the North American segment, contributing the bulk of unit sales and procurement contracts, driven by the size of its armed forces and extensive overseas deployments. Canada represents a secondary, yet strategically important market, with procurement focused on specialized units and joint‑training exercises. Together, these two countries constitute the entire North American market, with the United States providing the majority share.

Regional Analysis of the North America Military Protective Eyewear Market - Detailed regional market performance?

The United States market benefits from large‑scale modernization programs such as the Army’s Soldier Protection Initiative, which emphasizes upgraded eyewear. Procurement cycles are accelerated by Federal acquisition regulations that prioritize proven, high‑performance solutions. In Canada, defense spending trends emphasize interoperability with U.S. forces, leading to synchronized adoption of compatible protective eyewear standards. Both regions exhibit steady demand, with occasional spikes aligned with training exercises and overseas deployments.

Leading Company Profiles in the North America Military Protective Eyewear Market - Industry players and strategies?

3M Company leverages its advanced polymer and coating technologies to deliver high‑performance ballistic lenses, emphasizing durability and anti‑fog treatments. Arena Tactical focuses on tactical design, rapid prototyping, and customization for special operations units. Blueye Tactical brings a heritage of rugged, Australian‑designed eyewear, emphasizing comfort and impact resistance, while Boll specializes in lightweight frames combined with cutting‑edge optical clarity. All firms pursue government contracts, invest in R&D, and seek strategic partnerships to broaden distribution.

Porter's Five Forces Analysis of the North America Military Protective Eyewear Market - Competitive forces assessment?

Threat of new entrants is moderate; high certification standards and capital‑intensive R&D create barriers, yet niche innovators can enter via specialized coatings. Supplier power is moderate; raw materials such as polycarbonate and specialty lenses are sourced from a limited pool of vendors, but large manufacturers can negotiate favorable terms. Buyer power is strong; defense agencies demand strict compliance, volume discounts, and performance guarantees. Substitute threat is low, as eyewear is a non‑negotiable protective requirement. Rivalry among existing firms is intense, driven by contract wins and technology differentiation.

SWOT Analysis of the North America Military Protective Eyewear Market - Strengths, weaknesses, opportunities, threats?

Strengths: Established defense contracts, high barriers to entry, and proven technology base. Weaknesses: High unit cost and lengthy certification timelines. Opportunities: Integration of AR displays, smart‑glass sensors, and eco‑friendly materials. Threats: Potential supply‑chain disruptions for specialty polymers and rapid evolution of directed‑energy weapons that could outpace current laser‑protective solutions.

North America Military Protective Eyewear Market Value Chain Analysis - Industry structure and value flow?

The value chain starts with raw‑material suppliers providing polycarbonate sheets and coating chemicals, followed by R&D labs that develop ballistic and laser‑attenuation specifications. Manufacturing plants then fabricate frames and lenses, often using injection molding and precision coating processes. Distribution channels include direct government procurement portals and authorized defense distributors. After-sales services—such as lens replacement and refurbishment—complete the chain, ensuring lifecycle support for deployed units.

Key Investment Insights in the North America Military Protective Eyewear Market - Strategic investment recommendations?

Investors should target companies with robust R&D pipelines focused on smart‑glass integration, as this segment promises higher margins and defense‑grade differentiation. Partnerships with government research labs can accelerate certification and provide early access to emerging threat requirements. Additionally, capitalizing on the projected 4.61 % CAGR by allocating funds to firms expanding their manufacturing capacity will position investors to benefit from steady unit growth through 2033.

North America Military Protective Eyewear Market Conclusion - Summary and key takeaways?

The market remains on an upward trajectory, underpinned by consistent defense spending, technological innovation, and the strategic imperative to protect sight in increasingly complex threat environments. With a projected reach of 47.78 million units by 2033 and a clear shift toward multi‑threat, smart‑capable eyewear, the sector offers compelling growth opportunities for manufacturers, suppliers, and investors alike.

Research Methodology - How this research was conducted?

Data collection combined primary interviews with defense procurement officials, OEM technical leads, and industry analysts, alongside secondary sources such as government budget documents, company annual reports, and reputable defense publications. Market sizing employed a top‑down approach, extrapolating from known unit volumes and applying the disclosed CAGR. Validation loops ensured consistency across all segments and regional breakdowns.

Research Scope - Coverage and limitations?

The scope covers North America, specifically the United States and Canada, and includes all military‑grade protective eyewear types—Safety, Ballistic Protection, and Laser Protection—targeted at paramilitary forces and armed troops. The study excludes civilian safety eyewear, non‑protective fashion eyewear, and aftermarket replacement markets not directly linked to defense contracts.

Key Companies and Recent Developments in the North America Military Protective Eyewear Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

3M Company recently announced a new anti‑scratch, anti‑fog ballistic lens line that meets the latest NATO standards. Arena Tactical unveiled a rapid‑prototype platform allowing custom frame geometry within 48 hours for special‑operations units. Blueye Tactical entered a joint venture with a U.S. defense contractor to co‑develop laser‑attenuation coatings for emerging directed‑energy threats. Boll launched a lightweight titanium‑frame series aimed at reducing soldier fatigue during extended missions. These developments illustrate a market focused on faster innovation cycles and deeper integration with defense stakeholders.