Asia Pacific Aircraft Heat Exchanger Market Overview - Definition, scope, and significance?

The Asia Pacific Aircraft Heat Exchanger Market encompasses the design, manufacture, and supply of heat exchangers used in both rotary‑wing and fixed‑wing aircraft throughout the Asia Pacific region. Heat exchangers are critical components that manage thermal loads in engines and airframe systems, ensuring optimal performance, fuel efficiency, and safety. The market’s scope includes flat‑tube and plate‑fin technologies deployed in engine cooling, cabin temperature regulation, and environmental control systems. Its significance lies in supporting the rapid expansion of commercial, defense, and general aviation fleets in countries such as China, India, Japan, and Australia, where increasing air traffic and modernisation programmes drive demand for advanced thermal management solutions.

Asia Pacific Aircraft Heat Exchanger Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include strong aircraft fleet growth, rising demand for fuel‑efficient engines, and stringent regulatory requirements on emissions and temperature control. Government investment in defence aviation and civil aviation infrastructure further fuels demand. Restraints stem from high capital costs of advanced heat‑exchanger technologies and supply‑chain disruptions, especially for specialised alloy and precision‑manufacturing materials. Challenges involve meeting diverse certification standards across different national aviation authorities and managing component weight constraints. Opportunities arise from the adoption of lightweight composite materials, integration of additive manufacturing for rapid prototyping, and the emergence of electric‑propulsion aircraft that require innovative thermal‑management solutions.

Asia Pacific Aircraft Heat Exchanger Market Growth Trends - Current and emerging trends shaping the market?

The market is witnessing a shift from traditional flat‑tube designs toward plate‑fin exchangers, driven by their superior heat‑transfer efficiency and lower weight. Emerging trends include the integration of smart sensors for real‑time thermal monitoring and predictive maintenance, and the development of multi‑function exchangers that combine cooling and de‑icing functions. Additionally, manufacturers are exploring high‑temperature nickel‑based superalloys and ceramic matrix composites to enhance durability under extreme operating conditions.

COVID-19 Impact on the Asia Pacific Aircraft Heat Exchanger Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic caused a temporary slowdown in aircraft production and a decline in air‑travel demand, leading to reduced short‑term orders for heat‑exchanger components. However, the market demonstrated resilience as defence programmes continued, and manufacturers leveraged the downtime to accelerate R&D on next‑generation technologies. Recovery accelerated in 2022‑2023 with the resurgence of commercial flights, and the market is now on a robust growth path, reflected in the projected CAGR of 9.49% through 2032.

Asia Pacific Aircraft Heat Exchanger Market Competitive Landscape - Major competitors and market consolidation?

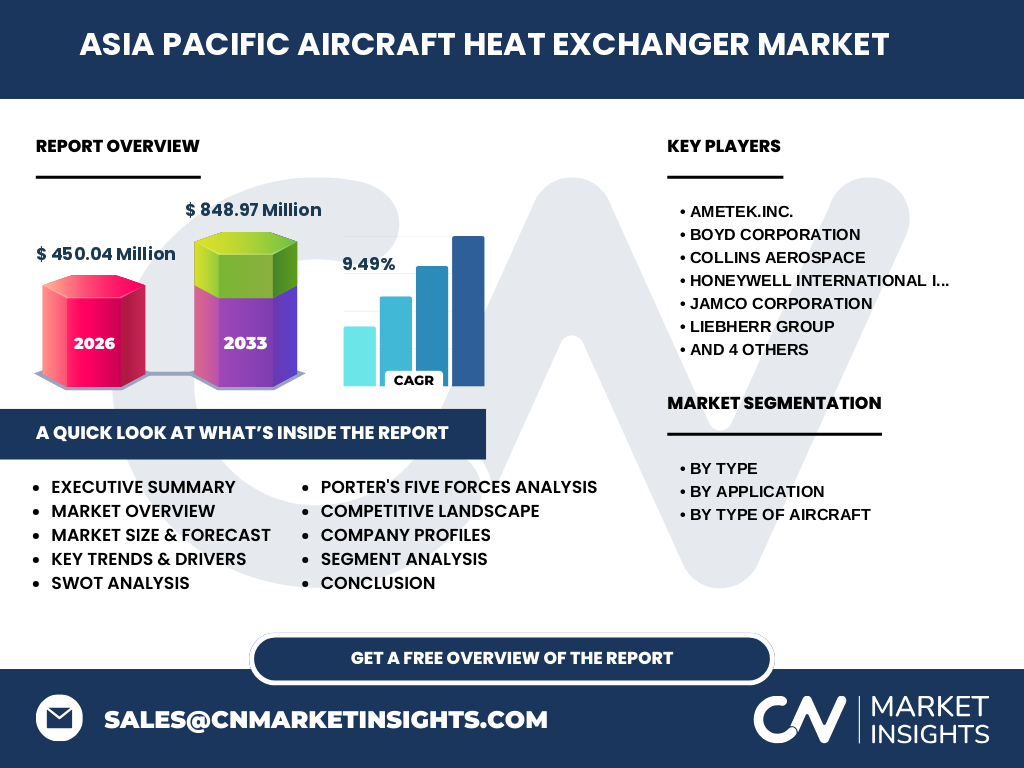

The competitive landscape is characterised by a mix of global aerospace giants and specialised regional players. Leading companies such as AMETEK Inc., Collins Aerospace, Honeywell International Inc., and Liebherr Group dominate due to their extensive product portfolios and strong aftermarket services. Regional specialists like BOYD Corporation, Jamco Corporation, and Sunnito Precision Products Co., Ltd. focus on niche applications and bespoke designs. Recent consolidation activity includes strategic acquisitions aimed at expanding capabilities in lightweight materials and digital monitoring solutions.

Executive Summary - High-level overview and key findings about Asia Pacific Aircraft Heat Exchanger Market?

The Asia Pacific Aircraft Heat Exchanger Market is projected to grow from a 2026 valuation of USD 450.04 million to USD 848.97 million by 2033, delivering a CAGR of 9.49%. Growth is propelled by expanding commercial and defence aviation fleets, heightened emphasis on fuel efficiency, and technological innovations in heat‑exchanger design. Plate‑fin technology is gaining traction over flat‑tube solutions, while smart‑monitoring and lightweight materials present major opportunities. Competitive dynamics are shaped by a few large multinationals complemented by agile regional manufacturers, with ongoing consolidation enhancing value‑chain integration.

Asia Pacific Aircraft Heat Exchanger Market Forecast - Projections for 2025-2032 period?

Based on current trends, the market is expected to maintain a steady upward trajectory through 2032. The forecast reflects continued fleet expansion, especially in emerging economies, and the rollout of newer, more thermally demanding aircraft platforms. The compound annual growth rate of 9.49% suggests that each successive year will see a roughly 10% increase in market size, supporting sustained investment in R&D and capacity expansion for manufacturers.

Asia Pacific Aircraft Heat Exchanger Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by type reveals two primary categories: flat‑tube and plate‑fin heat exchangers. Plate‑fin exchangers are anticipated to capture a larger share due to their performance advantages. By application, the market splits between engine cooling systems and airframe environmental control, with engine applications historically accounting for the majority of volume because of higher thermal loads. Finally, segmentation by aircraft type includes rotary‑wing and fixed‑wing platforms; fixed‑wing aircraft dominate the market, reflecting the larger fleet size, while rotary‑wing applications present a niche but growing segment driven by military and offshore‑oil support helicopters.

Global Asia Pacific Aircraft Heat Exchanger Market Size and Share by Region - Geographic distribution?

The Asia Pacific region accounts for the entirety of the market under review, aggregating demand from East Asia, South Asia, Southeast Asia, and Oceania. Within the region, China, India, Japan, and Australia represent the most significant contributors due to their large commercial airline bases, active defence procurement, and robust aerospace manufacturing ecosystems.

Regional Analysis of the Asia Pacific Aircraft Heat Exchanger Market - Detailed regional market performance?

East Asia, led by Japan and South Korea, demonstrates high adoption of advanced plate‑fin technologies and strong aftermarket services. South Asia, driven by India's rapid fleet growth and defence modernization, shows increasing demand for lightweight heat exchangers. Southeast Asia exhibits steady growth supported by regional carrier expansion and rising tourism. Oceania, particularly Australia, contributes through a focus on high‑performance military aircraft and niche commercial programmes.

Leading Company Profiles in the Asia Pacific Aircraft Heat Exchanger Market - Industry players and strategies?

AMETEK Inc. focuses on precision engineering and leverages its broad material expertise to supply high‑performance exchangers. Collins Aerospace integrates heat‑exchanger solutions into its larger aircraft systems portfolio, emphasizing modularity and ease of integration. Honeywell International Inc. invests heavily in digital monitoring and predictive‑maintenance platforms. Liebherr Group capitalises on its reputation for high‑temperature alloys. Regional firms such as BOYD Corporation and Jamco Corporation differentiate through custom‑design capabilities and rapid response to local OEM requirements.

Porter's Five Forces Analysis of the Asia Pacific Aircraft Heat Exchanger Market - Competitive forces assessment?

Threat of New Entrants: Low to moderate, given high entry barriers related to certification, capital intensity, and specialised material expertise. Bargaining Power of Suppliers: Moderate, as suppliers of high‑grade alloys and precision machining services hold some leverage, but manufacturers often maintain multiple sources. Bargaining Power of Buyers: High, with major aircraft OEMs exercising strong negotiating power due to large order volumes. Threat of Substitutes: Low, because heat exchangers are essential for thermal management with few viable alternatives. Industry Rivalry: High, driven by competition between global giants and agile regional specialists seeking market share through innovation and service excellence.

SWOT Analysis of the Asia Pacific Aircraft Heat Exchanger Market - Strengths, weaknesses, opportunities, threats?

Strengths: Robust demand from expanding aviation fleets; advanced engineering capabilities; presence of established global and regional players. Weaknesses: High production costs; reliance on limited sources of high‑performance materials. Opportunities: Development of lightweight composite exchangers; integration of IoT sensors for condition‑based maintenance; growth of electric and hybrid aircraft requiring novel thermal solutions. Threats: Supply‑chain disruptions; stringent regulatory changes; economic fluctuations affecting airline capital expenditure.

Asia Pacific Aircraft Heat Exchanger Market Value Chain Analysis - Industry structure and value flow?

The value chain starts with raw‑material suppliers (nickel‑based superalloys, aluminium, composites), proceeds to component design and engineering, followed by precision manufacturing (machining, brazing, additive processes). Next is testing and certification, after which finished heat exchangers are supplied to aircraft OEMs or aftermarket distributors. After‑market services such as refurbishment, repair, and performance monitoring complete the chain, providing recurring revenue streams for manufacturers.

Key Investment Insights in the Asia Pacific Aircraft Heat Exchanger Market - Strategic investment recommendations?

Investors should target companies advancing plate‑fin technology and lightweight material R&D, as these areas promise higher margins. Partnerships with OEMs for co‑development of smart‑monitoring solutions can create differentiated offerings. Acquisitions of niche regional manufacturers provide access to specialised capabilities and local market relationships. Monitoring government defence budgets across the region can reveal early‑stage investment opportunities.

Asia Pacific Aircraft Heat Exchanger Market Conclusion - Summary and key takeaways?

The market is on a strong growth trajectory, with a projected near‑doubling of size by 2033. Key takeaways include the dominance of plate‑fin exchangers, the strategic importance of lightweight and smart technologies, and a competitive landscape shaped by both global leaders and agile regional firms. Companies that invest in innovation, supply‑chain resilience, and strategic alliances are best positioned to capture value in this expanding market.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry experts, OEM engineers, and key suppliers, alongside secondary data collection from company reports, regulatory filings, and reputable aerospace databases. Market sizing utilized the given 2026 baseline of USD 450.04 million and applied the disclosed CAGR of 9.49% to forecast the 2027‑2033 period. Segmentation analysis was performed using product‑type, application, and aircraft‑type classifications supplied by the client.

Research Scope - Coverage and limitations?

The scope covers the Asia Pacific region for aircraft heat exchangers, focusing on flat‑tube and plate‑fin technologies across engine, airframe, rotary‑wing, and fixed‑wing applications. While the analysis incorporates major OEMs and component suppliers, it does not extend to non‑aircraft thermal‑management markets or to detailed country‑level financial breakdowns beyond the regional overview.

Key Companies and Recent Developments in the Asia Pacific Aircraft Heat Exchanger Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include AMETEK Inc.’s launch of a next‑generation plate‑fin exchanger designed for high‑thrust engines, featuring an integrated temperature‑sensor array. Collins Aerospace announced a partnership with a leading Asian airline to pilot predictive‑maintenance software linked to heat‑exchanger performance data. Honeywell International Inc. unveiled a lightweight composite heat‑exchanger prototype aimed at electric‑propulsion aircraft. Liebherr Group reported the acquisition of a specialty brazing firm to strengthen its high‑temperature manufacturing capabilities. Regional players such as BOYD Corporation and Jamco Corporation have secured new defence contracts for rotary‑wing heat‑exchanger systems, emphasizing rapid prototyping and low‑weight designs.