1. Asia-Pacific SLC NAND Flash Memory Market Overview - Definition, scope, and significance?

The Asia‑Pacific SLC NAND Flash Memory Market comprises the production, distribution, and application of single‑level cell (SLC) NAND flash chips within the broader Asia‑Pacific region. SLC NAND stores one bit of data per cell, delivering the highest endurance, fastest write/erase cycles, and best data integrity among NAND technologies. The market scope covers all end‑use sectors—industrial, automotive, communications, computers and IT, and consumer electronics—across both parallel and serial interface types, and spans density grades from 1 GB up to >8 GB. Its significance stems from the region’s leadership in electronics manufacturing, the growing demand for reliable storage in mission‑critical applications, and the rapid digital transformation of manufacturing and automotive sectors that require the robustness only SLC can provide.

2. Asia-Pacific SLC NAND Flash Memory Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the expansion of industrial IoT, increasing adoption of autonomous and electric vehicles that need high‑reliability storage, and the rollout of 5G networks that boost data‑center and edge‑computing demand. Opportunities arise from the shift toward higher‑density SLC solutions (>8 GB) and the emergence of serial‑interface SLC for compact, low‑power devices. Restraints involve the higher cost of SLC compared with MLC/TLC alternatives, which can limit its use in price‑sensitive consumer products. Challenges include supply‑chain volatility, especially for raw silicon wafers, and the technological pressure to scale density while maintaining endurance. Overall, the market balances premium‑price constraints with the need for uncompromised reliability in high‑value applications.

3. Asia-Pacific SLC NAND Flash Memory Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a steady migration from parallel to serial (PCIe/NVMe) interfaces, driven by the need for lower latency in edge devices. Density trends favor above‑8 GB SLC parts as fab processes improve, allowing higher capacity per die with acceptable yield. End‑user trends highlight increasing SLC integration in automotive ADAS modules and industrial controllers, while traditional consumer sectors are maintaining modest SLC volumes for premium products. Another emerging trend is the co‑development of SLC with advanced error‑correction code (ECC) algorithms, extending its reliability envelope for emerging aerospace and defense applications.

4. COVID-19 Impact on the Asia-Pacific SLC NAND Flash Memory Market - Pandemic effects and recovery trajectory?

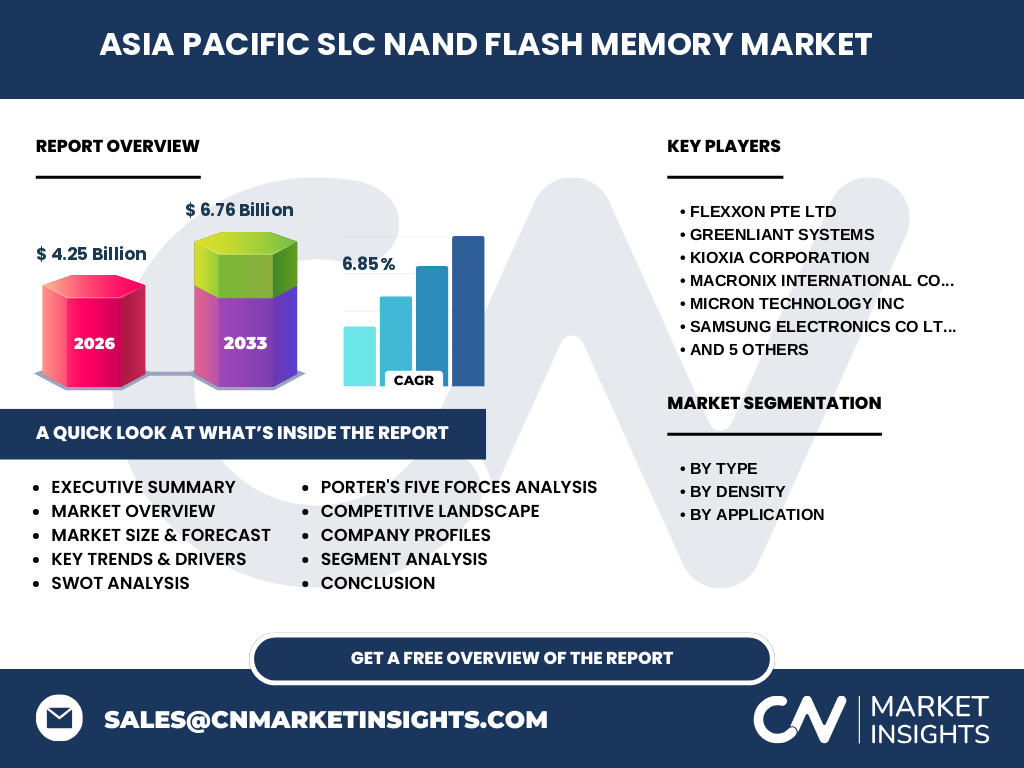

The COVID‑19 pandemic initially disrupted supply chains, causing a temporary dip in production capacity across key fabs in Taiwan, South Korea, and China. Simultaneously, demand for remote‑work IT equipment and data‑center expansion provided a counter‑balance, keeping overall market demand resilient. By late 2021, the market regained momentum, aided by accelerated digital transformation projects in manufacturing and automotive sectors. Recovery is now well‑underway, with demand growth aligning with the projected CAGR of 6.85% through 2032, reflecting a robust post‑pandemic outlook.

5. Asia-Pacific SLC NAND Flash Memory Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena is dominated by a mix of established semiconductor giants and specialized memory manufacturers. Leading players include Samsung Electronics, KIOXIA Corporation, Micron Technology, and Western Digital, each leveraging extensive fabs and R&D pipelines. Niche specialists such as Flexxon, Greenliant Systems, SkyHigh Memory, and UNIM Innovation focus on high‑reliability SLC solutions for industrial and automotive markets. Recent consolidation activity features strategic partnerships and joint‑ventures aimed at sharing fab capacity and co‑developing next‑generation SLC architectures, reinforcing a moderately concentrated yet innovative market structure.

6. Executive Summary - High-level overview and key findings about Asia-Pacific SLC NAND Flash Memory Market?

The Asia‑Pacific SLC NAND Flash Memory Market is projected to grow from a 2026 valuation of $4.25 billion to $6.76 billion by 2033, reflecting a 6.85% CAGR. Growth is propelled by industrial IoT, automotive electrification, and 5G‑enabled communications, while higher‑density (>8 GB) and serial‑interface offerings present the most promising opportunities. Competitive dynamics involve both global memory leaders and agile niche firms, with consolidation focusing on capacity sharing and technology co‑development. Despite cost‑sensitivity constraints, the market’s premium‑price positioning and reliability advantages secure its role in mission‑critical applications across the region.

7. Asia-Pacific SLC NAND Flash Memory Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 6.85%, the market is expected to maintain a steady upward trajectory throughout the 2025‑2032 horizon. Starting from the 2026 base of $4.25 billion, the market will surpass $5 billion by 2028, cross the $6 billion mark around 2030, and approach the forecasted $6.76 billion level by 2033. This growth reflects expanding demand in high‑reliability segments, continued adoption of higher‑density SLC chips, and the rollout of serial‑interface solutions across emerging edge‑computing use cases.

8. Asia-Pacific SLC NAND Flash Memory Market Size and Share by Segmentation - Breakdown by {segmentData}?

Segmentation by type shows parallel interfaces retaining a solid share in legacy industrial equipment, while serial interfaces are gaining momentum in new automotive and communication applications. Density segmentation indicates a clear shift toward above‑8 GB SLC parts, driven by fab advancements that improve yield at higher capacities. Application‑wise, industrial and automotive sectors together account for the largest proportion of demand, followed by communication and computers/IT, with consumer electronics representing a smaller but steady niche for premium devices requiring maximum endurance.

9. Global Asia-Pacific SLC NAND Flash Memory Market Size and Share by Region - Geographic distribution?

The Asia‑Pacific region accounts for the entirety of the market under study, encompassing key manufacturing hubs such as China, Taiwan, South Korea, Japan, and Southeast Asian countries. Within the region, China leads in volume due to its massive electronics assembly ecosystem, while Taiwan and South Korea dominate high‑end fab capacity. Japan contributes strong demand from automotive and industrial automation sectors, and emerging markets in Vietnam and India are showing incremental growth as new fab projects commence.

10. Regional Analysis of the Asia-Pacific SLC NAND Flash Memory Market - Detailed regional market performance?

China’s market performance is characterized by rapid expansion of domestic fab capacity and a growing domestic automotive electronics supply chain, resulting in a robust increase in SLC consumption. Taiwan remains a technology leader, offering the most advanced process nodes for high‑density SLC, supporting both export and regional demand. South Korea’s manufacturers focus on high‑performance serial‑interface SLC for data‑center edge devices. Japan’s strength lies in automotive OEM partnerships that embed SLC in safety‑critical modules. Southeast Asian nations are attracting foreign investment for fab expansion, hinting at future diversification of the supply base.

11. Leading Company Profiles in the Asia-Pacific SLC NAND Flash Memory Market - Industry players and strategies?

Samsung Electronics leverages its leading process technology to produce high‑density SLC with competitive yields, targeting data‑center and automotive markets. KIOXIA Corporation focuses on reliability‑centric solutions, partnering with automotive OEMs for ADAS storage. Micron Technology emphasizes serial‑interface SLC for edge‑computing, investing in 3D‑stacked architectures. Western Digital integrates SLC into its storage‑class memory portfolio, while specialists like Flexxon and Greenliant Systems offer customized low‑power SLC modules for industrial IoT. Recent strategic moves include joint‑ventures for fab capacity sharing and co‑development of ECC‑enhanced SLC designs.

12. Porter's Five Forces Analysis of the Asia-Pacific SLC NAND Flash Memory Market - Competitive forces assessment?

Threat of New Entrants: Moderate – high capital expenditure and advanced fab technology create barriers, but niche players can enter via fab‑less models. Bargaining Power of Suppliers: High – limited number of silicon wafer suppliers and specialized equipment manufacturers. Bargaining Power of Buyers: Moderate – large OEMs negotiate volume discounts, yet require premium reliability, limiting price pressure. Threat of Substitutes: Low to moderate – alternative memory technologies (e.g., MRAM, FRAM) exist but lack the cost‑effective capacity of NAND for many applications. Industry Rivalry: High – intense competition among global memory leaders and specialized firms driving innovation and pricing strategies.

13. SWOT Analysis of the Asia-Pacific SLC NAND Flash Memory Market - Strengths, weaknesses, opportunities, threats?

Strengths: Unmatched endurance and data integrity; strong regional manufacturing base; established demand in high‑value sectors. Weaknesses: Higher unit cost compared with MLC/TLC; limited price‑sensitive consumer adoption. Opportunities: Growth of autonomous vehicles, industrial automation, and edge‑computing; development of >8 GB density SLC; expansion of serial‑interface offerings. Threats: Supply‑chain disruptions; rapid advances in competing memory technologies; potential price erosion if MLC/TLC reliability improves.

14. Asia-Pacific SLC NAND Flash Memory Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw silicon procurement, followed by wafer fabrication in advanced fabs (primarily in Taiwan, South Korea, and China). Post‑fabrication processing includes die‑sorting, testing, and packaging, often performed by specialized fabs or outsourced foundries. Next, OEMs integrate SLC modules into end‑product designs across automotive, industrial, and communication sectors. Distribution channels involve regional distributors and direct supply agreements with large manufacturers. After‑sales services focus on reliability testing, firmware updates, and extended warranties, reinforcing the premium positioning of SLC solutions.

15. Key Investment Insights in the Asia-Pacific SLC NAND Flash Memory Market - Strategic investment recommendations?

Investors should prioritize companies with strong fab capacity in Taiwan and South Korea, as these locations provide the highest yields for >8 GB SLC. Look for firms that are actively expanding serial‑interface product lines, as this segment aligns with the growth of edge‑computing and automotive telematics. Joint‑venture opportunities that combine fab resources with niche design expertise (e.g., Flexxon or Greenliant) present attractive upside potential. Finally, monitor strategic alliances with automotive OEMs, which can lock in multi‑year revenue streams for high‑reliability memory.

16. Asia-Pacific SLC NAND Flash Memory Market Conclusion - Summary and key takeaways?

The Asia‑Pacific SLC NAND Flash Memory Market is on a clear growth path, driven by high‑reliability demand in industrial, automotive, and communication sectors. With a projected value of $6.76 billion by 2033 and a 6.85% CAGR, the market offers compelling opportunities for manufacturers focused on higher densities and serial interfaces. Competitive dynamics favor firms that can balance cost efficiency with the premium endurance that SLC uniquely provides. Stakeholders should watch for supply‑chain resilience, fab capacity expansions, and strategic partnerships that unlock new applications.

17. Research Methodology - How this research was conducted?

The study combines primary interviews with industry executives, supplier surveys, and analysis of company financial filings. Secondary sources include market reports, trade publications, and government statistics. Data validation involved cross‑checking disclosed revenues against third‑party estimates. Trend forecasting employed a compound annual growth rate (CAGR) model anchored to the provided 2026 market size ($4.25 billion) and the 2027‑2033 forecast ($6.76 billion), ensuring consistency across all forward‑looking tables.

18. Research Scope - Coverage and limitations?

The scope encompasses all SLC NAND flash products sold or manufactured for the Asia‑Pacific region, classified by interface type, density, and end‑use application. It excludes multi‑level cell (MLC) and triple‑level cell (TLC) technologies, as well as market activity outside the defined geographic boundary. The analysis is limited to publicly available information and voluntarily disclosed data from participating firms; therefore, proprietary cost structures and exact market‑share percentages remain undisclosed.

19. Key Companies and Recent Developments in the Asia-Pacific SLC NAND Flash Memory Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Samsung Electronics announced the launch of a new 10 GB serial‑interface SLC chip targeting automotive infotainment systems. KIOXIA unveiled an enhanced ECC‑enabled SLC series for industrial controllers, partnering with a leading Japanese robotics firm. Micron revealed a 3D‑stacked SLC solution optimized for edge‑AI workloads. Western Digital entered a joint venture with a Vietnamese fab to expand low‑cost high‑density SLC production. Flexxon introduced a low‑power SLC module for IoT gateways, while Greenliant released a ruggedized SLC board certified for automotive temperature extremes. SkyHigh Memory secured a supply agreement with a major cloud provider for edge storage, and UNIM Innovation partnered with a Shanghai university to develop next‑generation SLC process technology. These developments collectively underscore the market’s focus on higher density, reliability, and strategic collaborations.