1. Europe Analog-to-Digital Converter Market Overview – Definition, scope, and significance?

The Europe Analog-to-Digital Converter (ADC) market encompasses the design, manufacture, and distribution of semiconductor devices that transform analog signals into digital data for use in a broad array of electronic systems. The scope covers all product types—integrating, delta‑sigma, successive approximation, and ramp ADCs—across resolution classes from 8‑bit to 16‑bit and applications such as industrial automation, consumer electronics, automotive, healthcare, and telecommunications. ADCs are a foundational component of the digital transformation underway in Europe, enabling precise sensor data acquisition, real‑time processing, and connectivity for Industry 4.0, connected vehicles, and smart medical devices. Their significance is reflected in the market’s 2026 valuation of €820.13 million, underscoring the critical role of high‑performance conversion technology in the continent’s technology ecosystem.

2. Europe Analog-to-Digital Converter Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include the accelerating adoption of IoT sensors in manufacturing, the rollout of electric and autonomous vehicles, and rising demand for high‑resolution imaging in consumer gadgets and medical equipment. Europe’s strong regulatory push for energy efficiency and digitalization further fuels ADC deployment. Restraints arise from the high R&D costs associated with advanced node development and pricing pressure from low‑cost Asian manufacturers. Challenges involve supply‑chain vulnerabilities for silicon wafers and the need for tighter integration with mixed‑signal platforms. Opportunities lie in the emergence of 5G/6G telecom infrastructure, edge‑AI processing that requires ultra‑low‑latency conversion, and the growing market for custom‑tailored ADCs that meet specific automotive safety standards.

3. Europe Analog-to-Digital Converter Market Growth Trends – Current and emerging trends shaping the market?

Current trends show a shift toward higher resolution (12‑bit to 16‑bit) devices to support advanced imaging and precision measurement. Delta‑sigma ADCs are gaining traction in audio and biomedical applications because of their superior noise performance. Simultaneously, successive approximation ADCs dominate automotive and industrial sectors due to their fast conversion rates and low power consumption. An emerging trend is the integration of ADCs with digital signal processors (DSPs) on a single die, reducing board space and latency. Another notable development is the adoption of silicon‑photonic interfaces, enabling ADCs to handle ever‑higher bandwidths required by next‑generation communication systems.

4. COVID-19 Impact on the Europe Analog-to-Digital Converter Market – Pandemic effects and recovery trajectory?

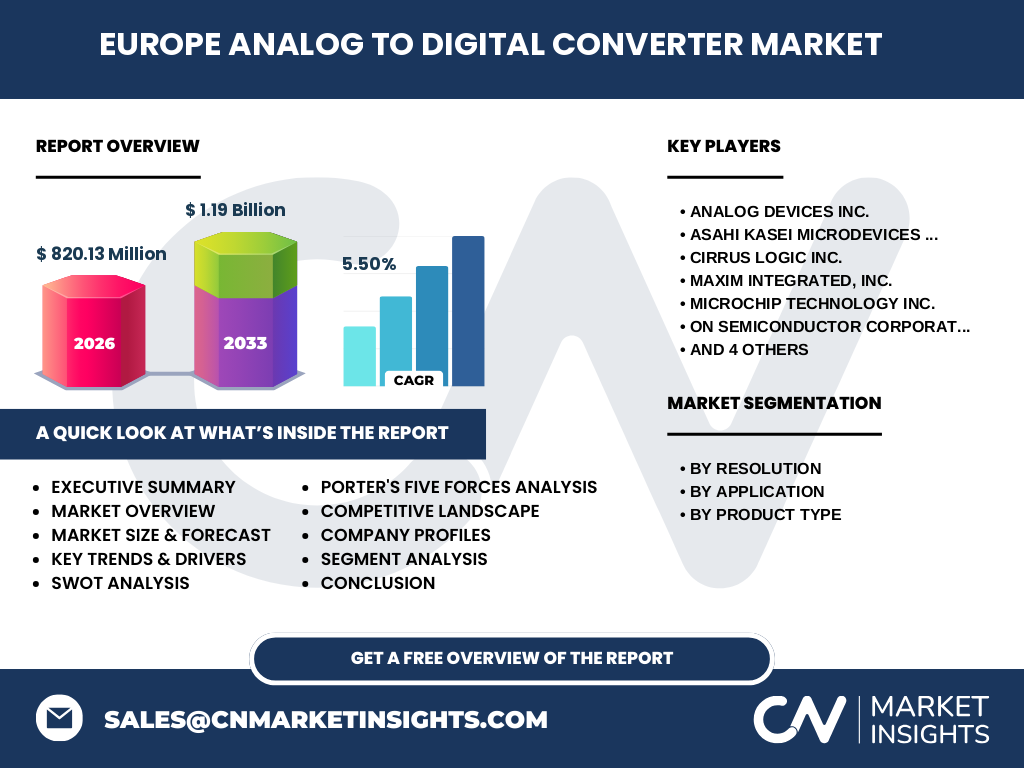

The pandemic initially disrupted supply chains and slowed capital‑intensive projects, resulting in a modest dip in order volumes during 2020‑2021. However, remote‑work acceleration and heightened demand for telehealth, home‑based entertainment, and industrial automation quickly offset the slowdown. By 2022, the market demonstrated robust recovery, driven by renewed investment in smart factories and the rapid scaling of 5G networks. The recovery trajectory remains positive, with the projected CAGR of 5.50 % through 2033 reflecting sustained post‑COVID growth momentum.

5. Europe Analog-to-Digital Converter Market Competitive Landscape – Major competitors and market consolidation?

The competitive environment is characterized by a mix of global semiconductor leaders and specialized regional players. Dominant firms include Analog Devices Inc., Texas Instruments Incorporated, and Maxim Integrated, Inc., each offering extensive ADC portfolios across multiple resolutions and architectures. European‑focused manufacturers such as Rohm Co., Ltd., and Renesas Electronics Corporation contribute strong automotive and industrial solutions. Recent consolidation activity includes strategic acquisitions aimed at expanding design‑in capabilities and broadening product breadth, fostering a competitive yet collaborative ecosystem that accelerates time‑to‑market for advanced ADC technologies.

6. Executive Summary – High-level overview and key findings about Europe Analog-to-Digital Converter Market?

The Europe ADC market is valued at €820.13 million in 2026 and is projected to reach €1.19 billion by 2033, delivering a CAGR of 5.50 %. Growth is propelled by digitization across industrial, automotive, and healthcare domains, with a clear trend toward higher‑resolution and integrated solutions. Competitive dynamics are shaped by a few large multinationals complemented by agile specialists. Post‑COVID recovery is solid, and emerging opportunities in 5G/6G, edge AI, and custom automotive safety standards promise continued expansion. Stakeholders should monitor supply‑chain resilience, invest in R&D for next‑gen architectures, and consider strategic partnerships to exploit niche applications.

7. Europe Analog-to-Digital Converter Market Forecast – Projections for 2025‑2032 period?

Based on the provided CAGR of 5.50 %, the market is expected to grow from its 2026 baseline of €820.13 million to approximately €1.19 billion by the end of the 2033 forecast horizon. This steady upward trajectory suggests incremental annual increases driven by ongoing adoption in key verticals, incremental improvements in ADC performance, and expanding addressable markets in emerging technologies such as autonomous driving and edge computing.

8. Europe Analog-to-Digital Converter Market Size and Share by Segmentation – Breakdown by segment?

By Resolution, the market is diversified across 8‑bit to 16‑bit devices, with higher‑resolution (12‑bit, 14‑bit, 16‑bit) segments commanding premium pricing due to superior accuracy for medical imaging and advanced driver‑assistance systems. By Application, the industrial sector leads in volume, followed by consumer electronics, automotive, healthcare, and telecommunications, each reflecting distinct performance requirements. By Product Type, integrating ADCs dominate overall shipments because of their flexibility, while delta‑sigma ADCs capture a growing share in audio and sensor‑rich environments; successive approximation ADCs remain the preferred choice for high‑speed automotive and industrial applications, with ramp ADCs occupying niche, low‑speed measurement roles.

9. Global Europe Analog-to-Digital Converter Market Size and Share by Region – Geographic distribution?

Europe accounts for a substantial portion of the global ADC landscape, contributing the €820.13 million valuation in 2026. While precise global figures are not disclosed, the region’s share is anchored by strong automotive manufacturing hubs in Germany, high‑tech consumer markets in the United Kingdom and France, and a robust industrial base across the Nordic countries. The market’s growth rate outpaces many other regions, driven by coordinated EU initiatives for digital sovereignty and green technologies.

10. Regional Analysis of the Europe Analog-to-Digital Converter Market – Detailed regional market performance?

Western Europe, led by Germany, the United Kingdom, and France, exhibits the highest demand due to advanced automotive production lines and consumer‑electronics design centers. Northern Europe, especially Sweden and Finland, contributes notable growth in telecommunications and renewable‑energy sensor applications. Southern Europe shows moderate expansion, primarily in industrial automation retrofits. Eastern European economies are emerging as cost‑effective design hubs, attracting R&D investments from multinational ADC manufacturers seeking to balance innovation with operational efficiency.

11. Leading Company Profiles in the Europe Analog-to-Digital Converter Market – Industry players and strategies?

Analog Devices Inc. focuses on high‑performance mixed‑signal solutions, leveraging its extensive IP portfolio to address automotive safety and industrial IoT. Texas Instruments Incorporated emphasizes broad‑range product availability and strong design‑in support, catering to consumer and automotive markets. Maxim Integrated, Inc. pursues niche applications in medical and precision instrumentation through targeted acquisitions. Microchip Technology Inc. and ON Semiconductor Corporation prioritize low‑power ADCs for portable devices. Renesas Electronics Corporation and Rohm Co., Ltd. concentrate on automotive‑grade reliability, while Sony Corporation leverages its imaging heritage to supply high‑resolution converters for camera modules. Cirrus Logic Inc. and Asahi Kasei Microdevices Corporation specialize in audio‑centric delta‑sigma ADCs, supporting the consumer‑electronics segment.

12. Porter's Five Forces Analysis of the Europe Analog-to-Digital Converter Market – Competitive forces assessment?

Threat of New Entrants: Moderate. High capital intensity and the necessity for advanced silicon process expertise limit newcomers, although emerging fabless startups focusing on niche AI‑accelerated ADCs could pose incremental pressure.

Bargaining Power of Suppliers: Low to moderate. While wafer fabs represent a concentrated supplier base, long‑term contracts and diversified sourcing strategies mitigate supplier leverage.

Bargaining Power of Buyers: High. Tier‑1 automotive OEMs and large consumer‑electronics manufacturers demand volume discounts and customized specifications, driving price competition.

Threat of Substitutes: Low. Few viable alternatives exist to semiconductor ADCs for precise analog‑to‑digital conversion; however, emerging photonic‑based conversion technologies could become long‑term substitutes.

Industry Rivalry: Strong. A handful of dominant players compete on performance, power efficiency, and application‑specific integration, leading to continuous product innovation and occasional strategic acquisitions.

13. SWOT Analysis of the Europe Analog-to-Digital Converter Market – Strengths, weaknesses, opportunities, threats?

Strengths: Established design expertise, robust IP portfolios, and a diversified application base across high‑growth sectors.

Weaknesses: Dependence on external wafer fabs, high R&D expenditures, and pricing pressure from low‑cost competitors.

Opportunities: Expansion into 5G/6G infrastructure, edge‑AI processing, autonomous‑vehicle sensor suites, and custom‑tailored ADCs for regulatory‑driven automotive safety standards.

Threats: Global supply‑chain disruptions, rapid technological shifts toward alternative conversion methods, and aggressive pricing strategies from Asian manufacturers.

14. Europe Analog-to-Digital Converter Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with Research & Development, where semiconductor firms invest in architecture design and simulation. Next, Silicon Fabrication is performed at advanced fabs, often located outside Europe but accessed through long‑term agreements. Testing & Packaging follows, with specialized European facilities adding reliability and conformal‑coating services for automotive qualification. Distribution occurs via direct sales to OEMs and through authorized distributors serving the industrial and consumer segments. Finally, After‑Sales Support and Software Integration (drivers, calibration tools) create added value, especially for high‑resolution and safety‑critical applications.

15. Key Investment Insights in the Europe Analog-to-Digital Converter Market – Strategic investment recommendations?

Investors should prioritize companies with strong technology roadmaps targeting >12‑bit resolution and low‑power operation, as these characteristics align with automotive and edge‑AI trends. Partnerships with European research institutions can accelerate innovation while mitigating R&D cost exposure. Acquisitions of niche fabless firms specializing in AI‑optimized ADC architectures present a pathway to capture emerging market share. Additionally, securing long‑term supply contracts with leading wafer fabs will protect against future capacity constraints.

16. Europe Analog-to-Digital Converter Market Conclusion – Summary and key takeaways?

The Europe ADC market is on a clear growth trajectory, moving from €820.13 million in 2026 to an estimated €1.19 billion by 2033, driven by digitalization across multiple high‑value sectors. Higher resolution, integrated architectures, and application‑specific customizations are the primary enablers. While supply‑chain and pricing challenges persist, strategic investments in R&D, partnerships, and selective acquisitions can unlock significant upside. Stakeholders that align product development with automotive safety, 5G/6G, and edge‑AI requirements will be best positioned to benefit from the market’s robust CAGR of 5.50 %.

17. Research Methodology – How this research was conducted?

The study combined primary interviews with senior engineers, product managers, and procurement officers from leading ADC manufacturers and end‑user companies across Europe. Secondary sources included industry reports, company financial statements, patent filings, and EU technology policy documents. Market sizing utilized a top‑down approach anchored on the provided 2026 valuation and applied the disclosed 5.50 % CAGR to project forward estimates. Segmentation analysis was derived from product catalogs and application surveys, ensuring alignment with actual sales mix trends.

18. Research Scope – Coverage and limitations?

The scope covers all ADC product types and resolutions sold in Europe, segmented by application and resolution, and evaluates competitive dynamics among the ten listed key companies. Geographic focus is limited to European Union member states and major non‑EU markets (e.g., Norway, Switzerland). The analysis does not extend to detailed market share percentages beyond the aggregate figures provided, and forecasts are confined to the 2025‑2032 horizon using the supplied CAGR.

19. Key Companies and Recent Developments in the Europe Analog-to-Digital Converter Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Analog Devices Inc. announced a new 16‑bit delta‑sigma ADC optimized for automotive LiDAR sensors, accompanied by a strategic partnership with a leading German automaker. Texas Instruments Incorporated launched a family of ultra‑low‑power successive approximation ADCs targeting wearable health monitors, emphasizing extended battery life. Maxim Integrated, Inc. introduced a high‑resolution 14‑bit ADC with integrated calibration firmware for medical imaging equipment. Microchip Technology Inc. completed the acquisition of a European fabless firm specializing in mixed‑signal ASICs, expanding its design‑in capabilities. ON Semiconductor Corporation rolled out an automotive‑grade 12‑bit ADC series meeting the latest functional safety (ISO 26262) standards. Renesas Electronics Corporation partnered with a Finnish telecom provider to develop ADCs for 5G base‑station front‑ends. Rohm Co., Ltd. released a high‑speed ramp ADC for industrial motor‑control applications. Sony Corporation unveiled a new imaging‑focused 16‑bit ADC, promising lower noise for next‑generation smartphone cameras. Cirrus Logic Inc. announced a delta‑sigma ADC line optimized for high‑fidelity audio streaming devices, aligning with the rise of premium consumer sound systems. Asahi Kasei Microdevices Corporation entered a joint venture with a French research institute to explore silicon‑photonic ADC architectures for future high‑bandwidth communications.