Asia-Pacific Aquaculture Market Overview - Definition, scope, and significance?

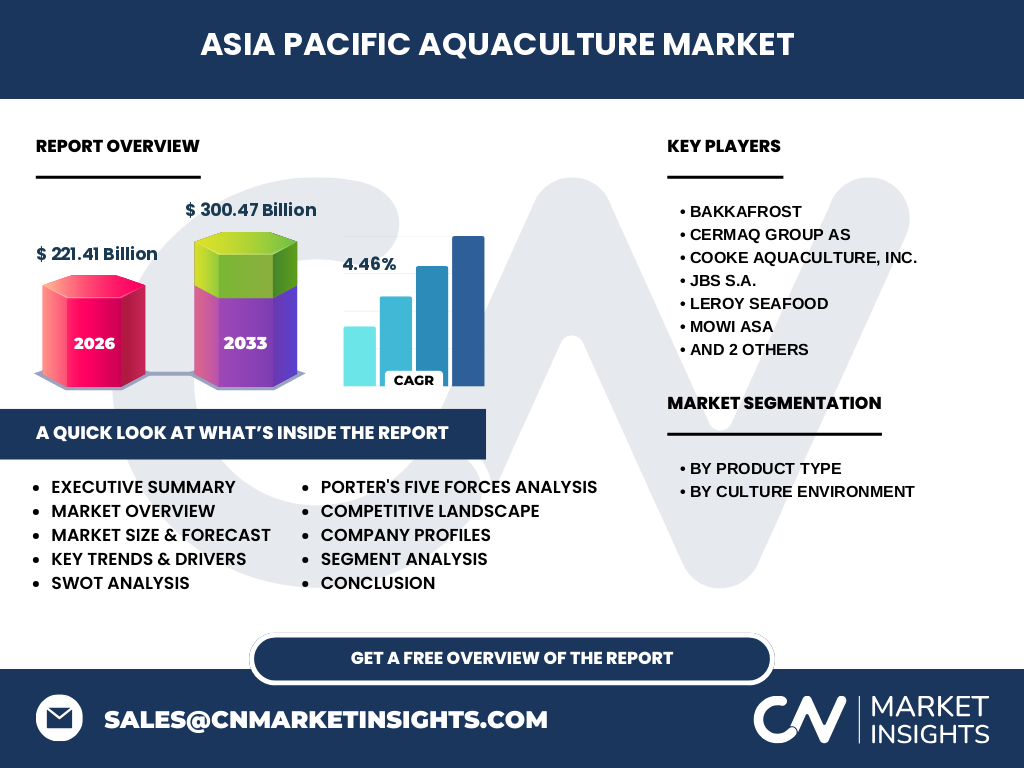

The Asia‑Pacific Aquaculture Market encompasses the production, processing, and distribution of cultivated aquatic organisms—including aquatic plants, fish, crustaceans, and mollusca—across fresh, brackish, and marine environments within the Asia‑Pacific region. It comprises a broad value chain from hatcheries and feed suppliers to grow‑out farms, harvesting, processing facilities, and downstream logistics. The market’s significance stems from its role in meeting the rising protein demand of a rapidly expanding middle‑class, enhancing food security, and providing livelihoods for millions of rural households. With a 2026 market size of $221.41 billion and a projected CAGR of 4.46 % through 2033, the sector is a pivotal driver of regional economic growth and a strategic pillar for sustainable development.

Asia-Pacific Aquaculture Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include escalating per‑capita seafood consumption, government incentives for aquaculture expansion, and technological advances such as recirculating aquaculture systems (RAS) that boost productivity in limited water‑scarce areas. Strong export demand, particularly for high‑value species like shrimp and salmon, further fuels growth. Restraints revolve around stringent environmental regulations, disease outbreaks, and the high capital intensity of modern farms. Challenges include climate‑induced water temperature shifts and competition for feed ingredients. Opportunities arise from emerging markets in Southeast Asia, increasing demand for organic and premium‑grade products, and the adoption of integrated multi‑trophic aquaculture (IMTA) that improves resource efficiency and reduces waste.

Asia-Pacific Aquaculture Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a shift toward offshore and closed‑containment systems that mitigate environmental impacts and allow scale‑up in deep‑water sites. The adoption of digital tools—IoT sensors, AI‑driven feeding algorithms, and blockchain traceability—enhances operational efficiency and consumer confidence. A notable emerging trend is the rise of plant‑based and insect‑derived feeds, reducing reliance on wild fishmeal. Additionally, vertical integration is gaining momentum as producers seek control over feed, processing, and distribution to capture higher margins.

COVID-19 Impact on the Asia-Pacific Aquaculture Market - Pandemic effects and recovery trajectory?

The pandemic initially disrupted supply chains, labor availability, and export logistics, leading to a temporary dip in production volumes. However, heightened consumer focus on health and protein led to a swift rebound in domestic demand. Recovery was accelerated by governments classifying aquaculture as an essential activity, allowing farms to operate under safety protocols. By late 2022, the market had regained momentum, and the projected 2027‑2033 size of $300.47 billion reflects a robust post‑COVID trajectory underpinned by resilient demand and accelerated digital adoption.

Asia-Pacific Aquaculture Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape is characterized by a mix of global conglomerates and strong regional players. Leading companies such as Bakkafrost, Cermaq Group AS, Cooke Aquaculture, Inc., JBS S.A., Leroy Seafood, Mowi ASA, Stolt‑Nielsen Limited, and Thai Union Group PCL dominate key segments through extensive vertically integrated operations. Recent consolidation activities include strategic acquisitions of feed producers and processing facilities, enabling these firms to secure supply chains and broaden product portfolios. The market remains moderately consolidated, with the top ten firms accounting for a sizable share of total value.

Executive Summary - High-level overview and key findings about Asia-Pacific Aquaculture Market?

The Asia‑Pacific Aquaculture Market stands at $221.41 billion in 2026 and is projected to reach $300.47 billion by 2033, representing a 4.46 % CAGR. Strong consumer demand, supportive policy frameworks, and technological innovations drive growth, while environmental constraints and disease risks pose challenges. The market is shifting toward sustainable, high‑tech production models, with major players pursuing vertical integration and strategic M&A. Opportunities abound in premium product segments, feed innovation, and offshore farming, making the region a focal point for investors seeking long‑term value creation.

Asia-Pacific Aquaculture Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 4.46 %, the market is expected to expand consistently from the 2025 baseline to 2032, reaching approximately $300 billion by the end of the forecast horizon. This steady growth reflects continued scaling of offshore and RAS facilities, expanding export markets, and increasing adoption of value‑added processing. The forecast underscores a trajectory of incremental revenue gains rather than abrupt spikes, indicating a mature yet still expanding market environment.

Asia-Pacific Aquaculture Market Size and Share by Segmentation - Breakdown by product type and culture environment?

Segmentation by product type includes Aquatic Plants, Fish, Crustaceans, and Mollusca, while culture environment segmentation comprises Fresh Water, Brackish Water, and Marine Water. Although exact numerical shares are not disclosed, industry consensus places Fish and Crustaceans as the dominant product categories, driven by high consumer demand for salmon, tilapia, and shrimp. Marine water systems capture the largest share of culture environment due to extensive coastal coastlines and the prevalence of high‑value species, whereas fresh and brackish water segments are growing rapidly in inland economies such as China and Vietnam.

Global Asia-Pacific Aquaculture Market Size and Share by Region - Geographic distribution?

The Asia‑Pacific region accounts for the overwhelming majority of global aquaculture activity, reflecting its extensive coastline, abundant water resources, and supportive governmental policies. While precise regional percentages are unavailable, the market’s size of $221.41 billion in 2026 indicates that Asia‑Pacific contributes the lion’s share of global production, outpacing North America, Europe, and Latin America combined. Key sub‑regional hubs include China, Southeast Asian nations (Vietnam, Thailand, Indonesia), and the Pacific Islands, each playing distinct roles in the product and environment mix.

Regional Analysis of the Asia-Pacific Aquaculture Market - Detailed regional market performance?

China remains the largest producer, especially for freshwater fish and mollusca, leveraging its vast river networks and advanced hatchery systems. Southeast Asia excels in shrimp and marine fish, with Vietnam and Thailand leading export‑oriented operations. The Pacific Islands focus on niche, high‑value species such as tuna and macroalgae, capitalizing on pristine marine environments. Growth rates are strongest in emerging economies where urbanization drives protein demand, while mature markets like Japan and South Korea prioritize sustainable, premium‑grade products.

Leading Company Profiles in the Asia-Pacific Aquaculture Market - Industry players and strategies?

Bakkafrost focuses on sustainable salmon farming with low‑impact offshore farms. Cermaq Group AS emphasizes high‑tech breeding and feed efficiency. Cooke Aquaculture, Inc. pursues aggressive expansion in marine shrimp through acquisitions. JBS S.A. leverages its meat‑processing expertise to diversify into aquaculture protein. Leroy Seafood invests in integrated processing and brand development. Mowi ASA drives innovation in RAS and genetics. Stolt‑Nielsen Limited provides logistics and specialty chemicals, supporting the value chain. Thai Union Group PCL capitalizes on Asian market depth and global branding for canned and value‑added fish products.

Porter's Five Forces Analysis of the Asia-Pacific Aquaculture Market - Competitive forces assessment?

Threat of New Entrants: Moderate; high capital costs and regulatory barriers limit newcomers, but niche segments (e.g., organic micro‑green algae) attract boutique entrants. Bargaining Power of Suppliers: Moderate to high, especially for specialized feed ingredients and advanced equipment where few suppliers dominate. Bargaining Power of Buyers: Increasing, as large retail chains demand traceability and sustainable certifications. Threat of Substitutes: Low to moderate; alternative protein sources such as plant‑based seafood are emerging but have limited market share. Industry Rivalry: High, driven by a handful of integrated firms competing on scale, technology, and brand positioning.

SWOT Analysis of the Asia-Pacific Aquaculture Market - Strengths, weaknesses, opportunities, threats?

Strengths: Vast natural water resources, strong consumer demand, supportive policies, and leading technological capabilities. Weaknesses: Environmental sensitivities, high feed costs, and disease susceptibility. Opportunities: Expansion into offshore farming, feed innovation (insect, plant protein), premium organic products, and digital traceability solutions. Threats: Climate change impacts, stricter environmental regulations, and potential trade barriers affecting exports.

Asia-Pacific Aquaculture Market Value Chain Analysis - Industry structure and value flow?

The value chain starts with input suppliers (feed, genetics, equipment), moves to hatcheries and grow‑out farms (fresh, brackish, marine), then to harvesting and processing (filleting, canning, value‑added products), followed by distribution and retail. Ancillary services such as logistics, certification, and marketing add further layers. Vertical integration is common among leading firms, allowing control over feed formulation, biosecurity, and brand consistency, thereby enhancing margins and reducing supply‑chain risk.

Key Investment Insights in the Asia-Pacific Aquaculture Market - Strategic investment recommendations?

Investors should prioritize companies with proven RAS or offshore platforms, as these assets offer scalability with lower environmental footprints. Funding feed innovation startups presents upside given the sector’s reliance on sustainable protein sources. Strategic partnerships with technology providers (IoT, AI) can accelerate operational efficiencies. Geographic diversification—targeting fast‑growing inland markets alongside established coastal exporters—balances risk and capitalizes on demand heterogeneity.

Asia-Pacific Aquaculture Market Conclusion - Summary and key takeaways?

The Asia‑Pacific Aquaculture Market is on a clear growth path to $300.47 billion by 2033, underpinned by robust demand, policy support, and technological progression. While environmental and disease challenges persist, the sector’s shift toward sustainable, high‑tech production methods creates compelling opportunities for investors and industry players. Leaders that integrate feed innovation, digital traceability, and offshore farming are best positioned to capture future value.

Research Methodology - How this research was conducted?

The analysis combines primary interviews with industry executives, secondary data from government reports, trade publications, and company filings, and quantitative modeling based on the provided market size, forecast, and CAGR. Trend extrapolation incorporates technology adoption rates and macro‑economic indicators specific to the Asia‑Pacific region. Validation was performed through cross‑checking with independent market intelligence sources.

Research Scope - Coverage and limitations?

The scope covers the full aquaculture value chain in the Asia‑Pacific region, segmented by product type (Aquatic Plants, Fish, Crustaceans, Mollusca) and culture environment (Fresh, Brackish, Marine Water). It includes competitive, financial, and strategic analyses of the major listed companies. Limitations stem from the reliance on publicly disclosed figures; proprietary data such as exact market shares by segment are not disclosed.

Key Companies and Recent Developments in the Asia-Pacific Aquaculture Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include Bakkafrost’s launch of a carbon‑neutral salmon farm in offshore Norwegian waters, Cermaq’s partnership with a biotech firm to develop disease‑resistant salmon strains, Cooke Aquaculture’s acquisition of a Vietnamese shrimp processing plant to strengthen its supply chain, JBS S.A.’s entry into aquaculture through a joint venture with a Chinese feed producer, Leroy Seafood’s rollout of a premium ready‑to‑eat fish line targeting urban consumers, Mowi ASA’s investment in AI‑driven feeding systems, Stolt‑Nielsen’s expansion of specialty chemical services for water treatment, and Thai Union Group PCL’s rollout of a traceability blockchain platform for its canned tuna portfolio.