What is the Fiberglass Pipes Market Overview – Definition, scope, and significance?

The Fiberglass Pipes Market comprises the manufacturing, distribution, and application of reinforced polymer pipes made from glass fibers embedded in a resin matrix. These pipes are engineered for high strength‑to‑weight ratios, corrosion resistance, and long service life across a spectrum of industries. The market’s scope encompasses end‑use sectors such as oil and gas, sewage, chemicals, and agriculture, as well as resin‑type categories including polyester, epoxy, and phenolic. Its significance stems from the growing need for durable, low‑maintenance piping solutions that can withstand aggressive media, extreme temperatures, and remote installations, thereby reducing lifecycle costs and improving operational safety.

What are the Fiberglass Pipes Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising capital expenditures in oil‑and‑gas infrastructure, increasing demand for corrosion‑free sewage networks, and expanding agricultural irrigation projects that favor lightweight, durable pipelines. Opportunities arise from the adoption of advanced epoxy and phenolic resins that enhance chemical resistance, and from government incentives for replacing aging metallic pipe networks. Restraints involve the higher upfront cost of fiberglass pipes relative to conventional steel or PVC, while challenges include limited awareness in emerging markets and the need for skilled installation personnel. Supply‑chain disruptions for glass fibers can also temper growth.

What are the current Fiberglass Pipes Market Growth Trends?

Recent trends show a shift toward high‑performance epoxy resin systems, driven by stricter environmental regulations on hazardous chemicals. Manufacturers are also integrating smart sensors into pipe walls for real‑time monitoring of pressure and integrity, aligning with Industry 4.0 initiatives. Additionally, modular pipe‑assembly kits are gaining traction, enabling faster on‑site deployment in remote oil fields and agricultural installations. The market is witnessing consolidation as larger players acquire niche fabricators to broaden product portfolios and geographic reach.

How did COVID‑19 impact the Fiberglass Pipes Market and what is the recovery trajectory?

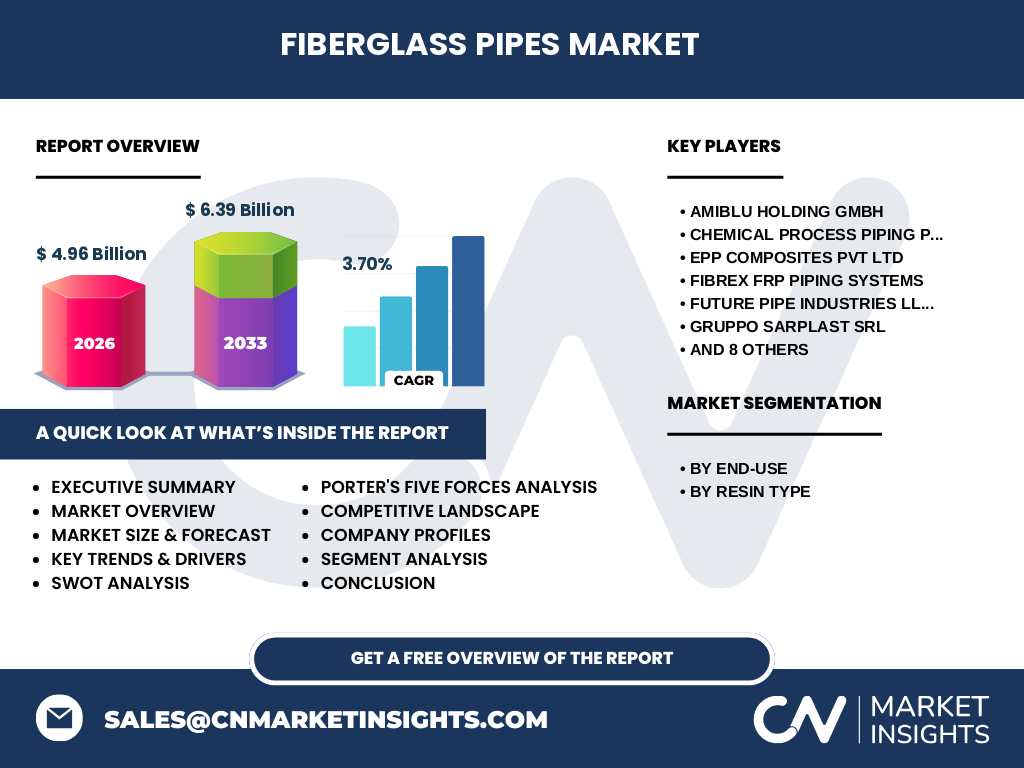

The pandemic caused temporary project delays, especially in the oil‑and‑gas sector, due to lockdowns and reduced capital spending. However, essential infrastructure projects such as sewage upgrades and agricultural irrigation continued, offsetting some losses. Post‑2020, the market rebounded quickly as stimulus funds were directed toward water‑treatment and energy infrastructure, leading to a renewed demand for corrosion‑resistant piping. The recovery trajectory is positive, with the market projected to grow at a 3.70% CAGR through 2032, indicating robust long‑term momentum.

Who are the major competitors in the Fiberglass Pipes Market and what is the competitive landscape?

The market is moderately concentrated, featuring a mix of global manufacturers and regional specialists. Leading firms such as Amiblu Holding GmbH, Future Pipe Industries LLC, and NOV Inc dominate the high‑value oil‑and‑gas segment, while companies like Kurotec‑KTS GmbH and Saudi Arabian Amiantit Co focus on sewage and water‑treatment projects. Competitive dynamics are shaped by product innovation, resin technology upgrades, and strategic acquisitions that enhance distribution networks. Recent consolidation moves have increased market concentration, but ample room remains for niche players that offer customized solutions.

What are the key findings in the Executive Summary of the Fiberglass Pipes Market?

The Fiberglass Pipes Market sized at $4.96 billion in 2026 and is forecast to reach $6.39 billion by 2033, reflecting a 3.70% CAGR. Growth is propelled by expanding oil‑and‑gas pipelines, intensified sewage infrastructure investments, and agricultural irrigation needs. Epoxy and phenolic resin innovations are reshaping product offerings, while smart‑pipe technologies are emerging as differentiators. The market’s competitive landscape is trending toward consolidation, with major players leveraging acquisitions to broaden geographic coverage. Despite higher upfront costs, the long‑term savings from corrosion resistance and reduced maintenance are driving adoption across all end‑use segments.

What is the Fiberglass Pipes Market Forecast for 2025‑2032?

Based on the provided CAGR of 3.70%, the market is expected to expand from its 2026 base of $4.96 billion to approximately $6.39 billion by the end of 2033. This steady growth suggests a compound increase of roughly $0.19 billion per year on average, supporting ongoing investments in high‑value sectors such as oil‑and‑gas and sewage treatment. The forecast indicates a resilient market that can absorb macro‑economic fluctuations while delivering incremental revenue gains.

How is the Fiberglass Pipes Market sized and shared by segmentation?

Segment analysis reveals two primary dimensions: end‑use and resin type. In the end‑use segment, oil and gas command the largest share due to the critical need for corrosion‑free transport of hydrocarbons, followed by sewage systems that benefit from the pipe’s longevity. Chemicals and agriculture complete the portfolio, with the latter gaining momentum from irrigation projects. Regarding resin type, polyester remains the most widely used because of its cost‑effectiveness, while epoxy is gaining ground for high‑temperature and chemically aggressive applications. Phenolic resin, though niche, serves specialized chemical processing environments where fire resistance is paramount.

What is the global Fiberglass Pipes Market size and share by region?

The market’s geographic distribution reflects strong demand in regions with mature oil‑and‑gas infrastructure and expanding water‑treatment programs. While specific regional dollar values are not disclosed, North America and the Middle East lead in oil‑and‑gas pipe installations, Europe shows robust sewage system upgrades, and Asia‑Pacific exhibits rapid growth in agricultural irrigation and chemical processing facilities. These regions collectively sustain the market’s $4.96 billion base and drive the projected growth to $6.39 billion.

What does the Regional Analysis of the Fiberglass Pipes Market reveal?

North America benefits from stringent environmental standards that favor corrosion‑resistant piping, bolstering demand in both energy and municipal water sectors. The Middle East’s continued investment in offshore and onshore oil projects sustains high‑volume sales of high‑strength epoxy‑based pipes. Europe’s aging sewage networks are being retrofitted with fiberglass solutions to meet EU water‑quality directives. Asia‑Pacific’s agricultural expansion and burgeoning chemical parks are accelerating the adoption of cost‑effective polyester and epoxy pipes. Overall, each region’s regulatory environment and sectoral priorities shape distinct growth patterns.

Who are the leading companies in the Fiberglass Pipes Market and what are their strategies?

Key players include Amiblu Holding GmbH, Future Pipe Industries LLC, NOV Inc, and Saudi Arabian Amiantit Co. Their strategies focus on expanding resin technology portfolios, pursuing strategic acquisitions to enter new geographies, and investing in digital monitoring solutions for pipe integrity. Companies such as Kurotec‑KTS GmbH and Gruppo Sarplast Srl emphasize customized engineering services to capture niche projects, while manufacturers like Lianyungang Zhongfu Lianzhong Composites Group Co Ltd leverage cost‑competitiveness to gain market share in emerging economies.

How does Porter’s Five Forces analysis apply to the Fiberglass Pipes Market?

Threat of new entrants is moderate; high capital requirements and technical expertise limit newcomers. Bargaining power of suppliers is moderate because glass fiber and resin suppliers are concentrated, but alternative resin formulations mitigate risk. Bargaining power of buyers is relatively high in large oil‑and‑gas contracts, where procurement teams demand price transparency and performance guarantees. Threat of substitutes is low to moderate; while steel and PVC remain alternatives, their corrosion and weight disadvantages reduce substitutability. Competitive rivalry is intense, driven by product innovation, cost efficiency, and strategic partnerships.

What are the SWOT insights for the Fiberglass Pipes Market?

Strengths: Superior corrosion resistance, lightweight installation, long service life. Weaknesses: Higher initial cost, need for specialized installation. Opportunities: Growth of epoxy and phenolic resins, smart‑pipe monitoring, infrastructure renewal programs. Threats: Price competition from alternative materials, supply constraints for glass fibers, economic slowdown in key oil‑and‑gas regions.

What does the Fiberglass Pipes Market value chain look like?

The value chain starts with raw material procurement (glass fibers, polyester/epoxy/phenolic resins), followed by resin formulation and filament winding or pultrusion manufacturing. Next, pipe finishing includes surface treatment, testing, and certification. Distribution channels involve direct sales to EPC contractors, regional distributors, and online platforms for smaller diameter products. After‑sales services encompass installation support, maintenance training, and digital condition‑monitoring solutions, completing the end‑to‑end flow.

What key investment insights can be drawn from the Fiberglass Pipes Market?

Investors should target companies that are expanding epoxy‑resin capabilities and integrating IoT‑based monitoring, as these technologies command premium pricing and lock‑in customers. Acquisitions of regional fabricators that provide localized production can improve margins and reduce logistics costs. Funding projects in regions with strong infrastructure stimulus—particularly sewage upgrades and agricultural irrigation—offers steady demand. Lastly, allocating capital to firms with diversified end‑use portfolios mitigates exposure to sector‑specific downturns.

What conclusions can be drawn about the Fiberglass Pipes Market?

The Fiberglass Pipes Market is on a solid growth trajectory, moving from $4.96 billion in 2026 to an estimated $6.39 billion by 2033. Its resilience stems from the intrinsic advantages of fiberglass piping and the expanding need for corrosion‑free infrastructure across oil‑and‑gas, sewage, chemicals, and agriculture. While upfront costs remain a hurdle, the long‑term operational savings and emerging smart‑pipe technologies reinforce market attractiveness. Strategic focus on resin innovation and geographic expansion will be critical for sustained success.

How was the research for this market report conducted?

The study employed a mixed‑method approach, combining primary interviews with industry experts, manufacturers, and end‑user engineers, alongside secondary data extraction from company filings, trade publications, and governmental infrastructure reports. Quantitative data were validated through cross‑referencing multiple sources, and qualitative insights were synthesized to capture market sentiment and emerging trends.

What is the scope of this research?

The research covers global fiberglass pipe manufacturing, distribution, and end‑use applications across oil‑and‑gas, sewage, chemicals, and agriculture sectors. It examines resin‑type segmentation (polyester, epoxy, phenolic) and provides regional analysis for major markets. The scope excludes unrelated composite products and focuses on pipe systems designed for fluid transport and containment.

Which key companies and recent developments are highlighted in the Fiberglass Pipes Market?

Prominent firms include Amiblu Holding GmbH, Future Pipe Industries LLC, NOV Inc, and Saudi Arabian Amiantit Co. Recent developments feature Amiblu’s launch of a high‑temperature epoxy pipe line for offshore projects, Future Pipe’s acquisition of a European sewage‑pipe specialist, NOV Inc’s partnership with a digital‑monitoring startup to embed sensors in pipelines, and Saudi Arabian Amiantit’s expansion of a manufacturing plant in the Gulf to serve the growing water‑treatment market. These activities underscore a trend toward technology integration and capacity scaling.