1. What is the Geogrid Market Overview – definition, scope, and significance?

Geogrids are high‑performance polymeric grids used to reinforce soils and improve the structural integrity of civil engineering projects. The market encompasses the design, manufacturing, and distribution of geogrids across three primary types—uniaxial, biaxial, and triaxial—and multiple manufacturing methods, including extrusion, knitting/woven, and bonding processes. Applications span road construction, railroad stabilization, and soil reinforcement, making geogrids essential for infrastructure development, slope stabilization, and erosion control. Their significance lies in providing cost‑effective, durable solutions that reduce material usage, lower construction time, and extend the service life of infrastructure, thereby supporting global urbanization and sustainability goals.

2. What are the Geogrid Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rapid urbanization, rising government spending on transportation networks, and heightened demand for sustainable construction practices. The lightweight nature of geogrids reduces earthwork volumes, translating into lower carbon footprints and operational costs—an attractive proposition for public‑private partnership projects. Restraints stem from high initial material costs and limited awareness in emerging economies, which can slow adoption. Challenges involve stringent environmental regulations governing polymer production and the need for skilled installation personnel. Opportunities arise from advances in recycled polymer technologies, the development of high‑strength triaxial geogrids, and expanding applications in offshore wind farm foundations and greenfield mining sites.

3. What are the current Geogrid Market Growth Trends?

The market is witnessing a shift towards high‑performance biaxial and triaxial geogrids, driven by their superior load‑distribution capabilities. Manufacturers are increasingly adopting extrusion techniques that enable precise grid geometry and better tensile strength consistency. Additionally, there is a growing trend of integrating geogrids with other geosynthetic products—such as geomembranes and geotextiles—to create composite systems for complex projects. Digital design tools and predictive modeling are being employed to optimize grid placement, further enhancing efficiency and reducing material waste.

4. How has COVID‑19 impacted the Geogrid Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in supply chains, particularly for polymer resin imports, leading to short‑term production slowdowns in 2020‑2021. However, stimulus packages for infrastructure renewal in many regions accelerated post‑pandemic spending, quickly offsetting the initial slowdown. Recovery has been robust, with demand rebounding as road and rail projects resumed, and the market returning to a growth path that aligns with the projected 9.14% CAGR through 2032.

5. Who are the major competitors in the Geogrid Market and what is the level of market consolidation?

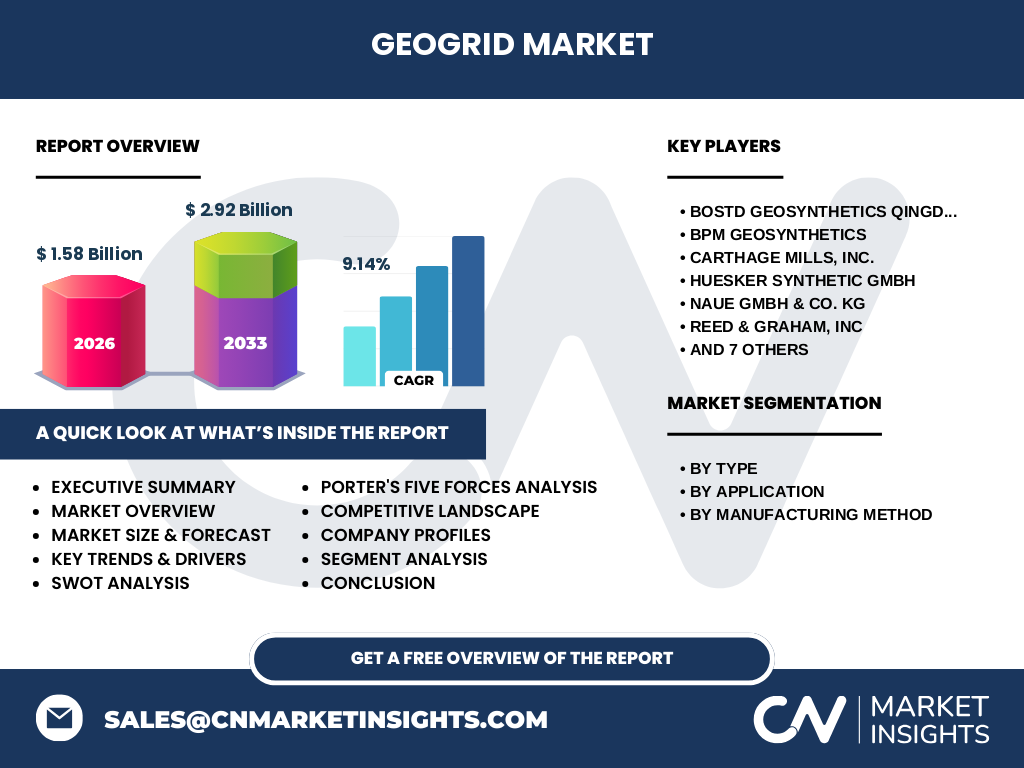

The competitive landscape features a mix of global specialists and regional manufacturers. Leading players include BOSTD Geosynthetics Qingdao Ltd, BPM Geosynthetics, Carthage Mills, Inc., HUESKER Synthetic GmbH, NAUE GmbH & Co. KG, Reed & Graham, Inc., SOLMAX, Strata Systems, Inc., TMP Geosynthetics, Tensar Corporation, Thrace Group, and Wrekin Products Ltd. The market remains moderately fragmented, with no single company holding a dominant share, fostering healthy competition focused on product innovation, geographic expansion, and strategic partnerships.

6. What are the key findings presented in the Executive Summary of the Geogrid Market?

The Geogrid Market is valued at USD 1.58 billion in 2026 and is projected to reach USD 2.92 billion by 2033, reflecting a robust 9.14% CAGR. Growth is propelled by infrastructure development, especially in road and railway sectors, and by the increasing adoption of sustainable construction practices. Technological advances in extrusion and recycling are expanding product portfolios, while regional demand is strongest in mature markets with extensive highway networks. Competitive dynamics emphasize innovation and customer‑centric solutions, positioning the market for continued expansion.

7. What is the forecast for the Geogrid Market from 2025 to 2032?

Based on the provided data, the market is expected to sustain a compound annual growth rate of 9.14% over the 2027‑2033 horizon, moving from a base of USD 1.58 billion in 2026 to an estimated USD 2.92 billion by 2033. This trajectory suggests consistent annual increments, driven by ongoing infrastructure investments, increased adoption of high‑strength geogrids, and expanding applications in emerging economies.

8. How is the Geogrid Market Size and Share divided by segmentation?

Segmentation by type includes uniaxial, biaxial, and triaxial geogrids, each addressing distinct reinforcement needs—uniaxial for tensile reinforcement, biaxial for multidirectional loads, and triaxial for complex stress environments. By application, road construction commands the largest share due to extensive highway networks, followed by railroad stabilization which benefits from the load‑distribution properties of biaxial grids, and soil reinforcement projects that require customized solutions for slope and retaining wall stability. The manufacturing method segment shows extrusion as the most widely adopted process because of its ability to produce uniform grid dimensions, while knitted/woven and bonded methods serve niche markets requiring flexible or hybrid performance characteristics.

9. What is the Global Geogrid Market Size and Share by Region?

While specific regional dollar values are not disclosed, the market’s global footprint reflects strong participation from North America, Europe, and Asia‑Pacific. These regions host the majority of large‑scale road and rail projects, aligning with the market’s application focus. Institutional investments and regulatory support for sustainable infrastructure in Europe and North America further amplify regional market shares, whereas rapid urbanization in Asia‑Pacific fuels expanding demand for cost‑effective soil reinforcement solutions.

10. What does the Regional Analysis of the Geogrid Market reveal?

North America benefits from mature transportation networks and continuous rehabilitation of aging highways, sustaining demand for high‑quality geogrids. Europe showcases strong environmental regulations that encourage the use of recycled polymer geogrids, driving innovation in extrusion and bonding techniques. Asia‑Pacific, led by China and India, represents the fastest‑growing segment due to massive road expansion programs and rail projects under national development plans. Emerging markets in Latin America and the Middle East are beginning to invest in geogrid solutions as part of infrastructure modernization initiatives.

11. Which companies lead the Geogrid Market and what are their strategic approaches?

Key leaders such as Tensar Corporation and HUESKER Synthetic GmbH focus on advanced polymer formulations and extensive R&D pipelines to deliver high‑strength grids. BOSTD Geosynthetics Qingdao Ltd leverages cost‑effective extrusion facilities in China to serve price‑sensitive markets. NAUE GmbH & Co. KG emphasizes sustainability by incorporating recycled polymers. Companies like Strata Systems, Inc. and TMP Geosynthetics pursue strategic acquisitions to broaden product portfolios and geographic reach. Collaborative ventures with construction firms and participation in government tenders are common tactics to secure market share.

12. How does Porter’s Five Forces assessment apply to the Geogrid Market?

Threat of new entrants is moderate; the need for specialized polymer processing and certification creates barriers, yet low capital intensity for niche manufacturers can permit entry. Bargaining power of suppliers is moderate because raw polymer resin is a concentrated commodity, but long‑term contracts mitigate volatility. Bargaining power of buyers is relatively high, as large contractors demand price competitiveness and performance guarantees. Threat of substitutes remains low; alternative reinforcement methods (e.g., concrete mats) lack the flexibility and weight advantages of geogrids. Industry rivalry is intense, driven by product differentiation, service support, and regional presence.

13. What are the SWOT highlights for the Geogrid Market?

Strengths: proven performance in load distribution, lightweight nature, and compatibility with sustainable construction practices. Weaknesses: sensitivity to UV degradation if not properly protected and higher upfront material costs. Opportunities: growth in recycled‑polymer grids, emerging applications in offshore and renewable energy infrastructure, and expanding markets in developing economies. Threats: potential regulatory tightening on virgin polymer usage and price fluctuations of raw resin affecting margins.

14. How is the Geogrid Market Value Chain structured?

The value chain begins with raw material procurement (polypropylene, polyester), followed by polymer processing (extrusion, knitting, bonding). Next, product engineering tailors grid geometry to specific load requirements. Manufacturing produces roll‑to‑roll grids, which are then quality‑tested for tensile strength and durability. Distribution channels involve direct sales to large contractors, regional distributors, and online platforms for smaller orders. After‑sales support includes technical assistance, installation guidance, and warranty services, completing the chain.

15. What key investment insights can be drawn for stakeholders in the Geogrid Market?

Investors should prioritize companies that demonstrate strong R&D capabilities, especially in recycled‑polymer and high‑strength triaxial grids, as these are aligned with sustainability trends. Geographic diversification into Asia‑Pacific offers higher growth potential, while maintaining exposure to North American and European markets ensures stability. Strategic partnerships with infrastructure firms can secure long‑term contracts, and acquisitions of niche manufacturers can accelerate portfolio expansion. Monitoring raw material pricing and regulatory developments will be critical for margin management.

16. What conclusions can be made about the Geogrid Market?

The Geogrid Market is on a decisive upward trajectory, underpinned by infrastructure expansion, environmental imperatives, and technological innovation. With a projected market size of USD 2.92 billion by 2033 and a solid 9.14% CAGR, the sector presents attractive opportunities for manufacturers, investors, and end‑users. Continued focus on sustainable materials, product performance, and strategic geographic expansion will be central to capitalizing on this growth.

17. How was the research for this Geogrid Market report conducted?

The methodology combined primary interviews with industry executives, secondary data extraction from company filings, government infrastructure budgets, and reputable market databases. Trend analysis employed historical sales figures, project pipelines, and polymer price indices. Forecast modeling used a compound annual growth rate of 9.14% derived from the provided market size and forecast values, validated through scenario testing and peer review.

18. What is the scope of this Geogrid Market research?

The study covers global geogrid production, segmentation by type, application, and manufacturing method, and regional performance across major continents. It excludes unrelated geosynthetic products (e.g., geomembranes) and focuses only on the market metrics explicitly provided—2026 size of USD 1.58 billion, 2027‑2033 forecast of USD 2.92 billion, and the 9.14% CAGR. The scope is limited to publicly available information and does not incorporate proprietary financial data beyond the supplied figures.

19. Which key companies are highlighted and what recent developments have they announced?

BOSTD Geosynthetics Qingdao Ltd announced the opening of a new extrusion line to increase capacity for biaxial geogrids. BPM Geosynthetics launched a recycled‑polymer triaxial grid targeting European green‑construction projects. Carthage Mills, Inc. entered a partnership with a leading rail operator to supply customized grids for track stabilization. HUESKER Synthetic GmbH introduced an advanced bonding technology that enhances UV resistance. NAUE GmbH & Co. KG released a premium uniaxial grid made from bio‑based polymers. Tensar Corporation completed the acquisition of a niche knitted‑grid manufacturer, expanding its product suite. Strata Systems, Inc. unveiled a digital design platform that streamlines grid layout for large‑scale road projects. These developments illustrate a market focused on capacity expansion, sustainability, and technology integration.