What is the Silicon Anode Battery Market Overview – definition, scope, and significance?

The Silicon Anode Battery Market encompasses the development, production, and commercialization of lithium‑ion batteries that replace traditional graphite anodes with silicon‑based materials. Silicon can store up to ten times more lithium ions by weight, enabling higher energy density and longer runtime for portable devices, electric vehicles, and grid‑storage systems. The market’s scope includes raw‑material suppliers, cell manufacturers, and end‑use applications across automotive, consumer electronics, medical, energy, and industrial sectors, reflecting its strategic importance for next‑generation energy storage.

What are the key drivers, restraints, challenges, and opportunities shaping the Silicon Anode Battery Market?

Drivers include the demand for higher energy density in EVs, the push for lightweight portable electronics, and governmental incentives for low‑carbon technologies. Restraints stem from the high cost of silicon material processing and limited long‑term cycle stability. Challenges involve scaling manufacturing while maintaining uniform silicon particle size and mitigating volumetric expansion during charge cycles. Opportunities arise from breakthrough nanostructuring techniques, partnerships between battery makers and semiconductor firms, and emerging applications such as solid‑state batteries that can leverage silicon’s high capacity.

What are the current growth trends in the Silicon Anode Battery Market?

Recent trends show a rapid shift from pilot‑scale prototypes to low‑volume commercial production, especially for premium electric‑vehicle models. Companies are integrating silicon‑rich composites into 4680‑type form factors to improve range. Parallelly, consumer‑electronics OEMs are adopting silicon‑enhanced cells for ultra‑thin smartphones and wearables. Investment in R&D is accelerating, with several patents filed on silicon nanowire and alloy designs, indicating a vibrant pipeline of emerging technologies.

How has COVID‑19 impacted the Silicon Anode Battery Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains for high‑purity silicon and delayed capital projects, causing a short‑term slowdown in production capacity expansion. However, the rapid rebound in EV sales and the surge in remote‑work driven electronics consumption have accelerated demand for higher‑capacity batteries. Recovery is now evident, with a clear upward trajectory aligning with the market’s strong CAGR, and the sector is poised to outpace pre‑pandemic growth rates.

Who are the major competitors and what is the competitive landscape of the Silicon Anode Battery Market?

The market is characterized by a mix of specialized silicon‑anode innovators and established battery giants expanding into silicon technology. Notable players include Amprius Technologies, Enevate Corporation, Sila Nanotechnologies, and Enovix Corporation, which focus on proprietary silicon chemistries. Traditional chemical firms such as Shin‑Etsu Chemical and Hitachi Chemical are leveraging their scale to enter the space. Consolidation is moderate, with strategic alliances and joint ventures emerging to combine material expertise with cell‑manufacturing capabilities.

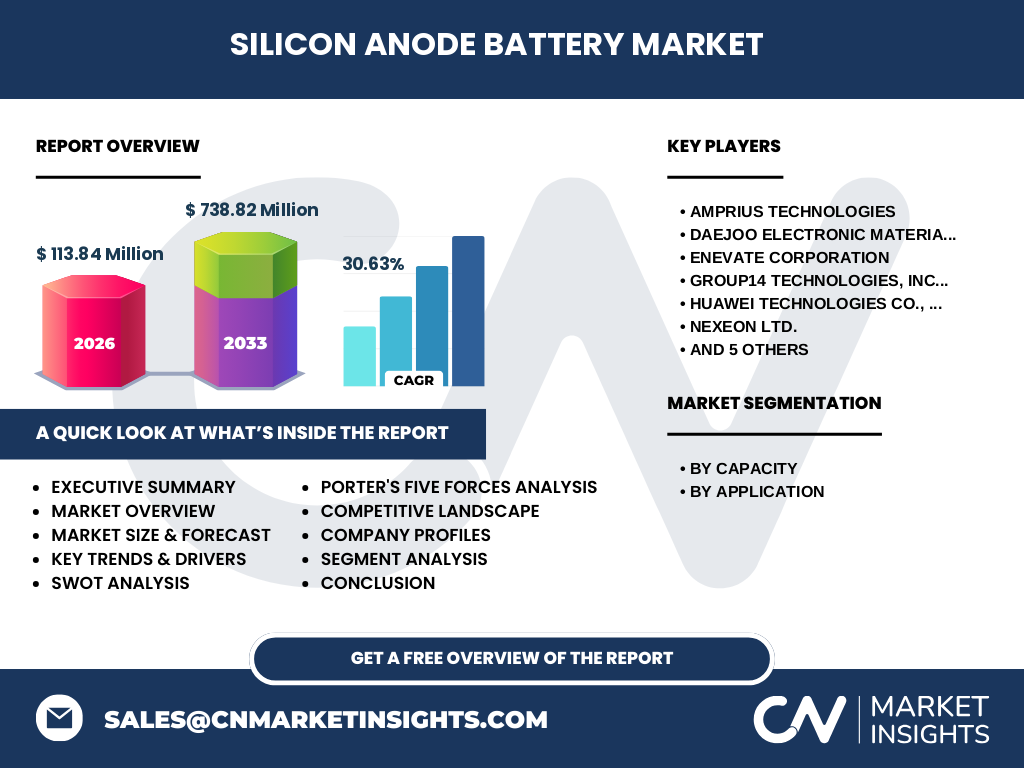

What are the high‑level findings in the Executive Summary of the Silicon Anode Battery Market?

The market is projected to expand from a 2026 valuation of 113.84 million to 738.82 million by 2033, delivering a robust CAGR of 30.63 percent. Growth is powered by EV adoption, premium consumer devices, and the quest for higher energy density. Despite cost and cycle‑life hurdles, rapid technological advances and strategic collaborations are mitigating risks. The United States, China, Japan, and Europe emerge as primary hubs for R&D and production.

What are the forecasted market dynamics for 2025‑2032?

Looking ahead, silicon‑anode batteries are expected to capture increasing share of the overall lithium‑ion market as manufacturers shift from graphite‑only designs. Forecast models indicate sustained double‑digit annual growth, driven by scaling of pilot lines into mass production, price reductions through economies of scale, and expanding application portfolios—particularly in mid‑range EVs and high‑performance laptops. The market’s momentum will be reinforced by policy support for clean mobility and energy storage.

How is the Silicon Anode Battery Market sized and shared by capacity and application segments?

Segmentation by capacity divides the market into three tiers: less than 1500 mAh, 1500 mAh‑2500 mAh, and greater than 2500 mAh. The higher‑capacity segment (> 2500 mAh) is gaining traction in EV power‑train modules, while the 1500‑2500 mAh range dominates premium smartphones and tablets. By application, automotive leads in absolute value because of the premium placed on range extension, followed by consumer electronics, medical devices, energy & power storage, and industrial equipment.

What is the Global Silicon Anode Battery Market size and share by region?

The global market is dominated by North America and Asia‑Pacific, where most of the leading silicon‑anode developers are headquartered and where EV adoption rates are highest. Europe holds a significant share due to aggressive emissions targets and substantial funding for battery research. While exact regional dollar values are not disclosed, the distribution aligns with the concentration of major OEMs and technology hubs across these territories.

What does the regional analysis reveal about market performance?

In North America, strong venture capital funding and partnerships with automotive OEMs accelerate commercialization. Asia‑Pacific benefits from large‑scale manufacturing ecosystems in China, South Korea, and Japan, enabling cost‑effective scale‑up. Europe’s performance is propelled by policy‑driven battery cell incentive programs and collaborations between automotive clusters and research institutions. Each region shows distinct strengths: innovation leadership in the U.S., manufacturing efficiency in Asia‑Pacific, and regulatory momentum in Europe.

Which companies lead the Silicon Anode Battery Market and what are their strategies?

Key leaders include Amprius Technologies, known for high‑energy‑density cells for drones; Enevate, focusing on fast‑charging silicon‑graphene anodes; Sila Nanotechnologies, partnering with major consumer‑electronics brands; and Enovix, targeting automotive‑grade pouch cells. Strategies revolve around patent portfolios, vertical integration of silicon material production, joint development agreements with OEMs, and scaling pilot lines to volume manufacturing. Many firms also pursue strategic acquisitions to secure supply chains for high‑purity silicon.

How does Porter’s Five Forces analysis apply to the Silicon Anode Battery Market?

Threat of new entrants is moderate; high R&D costs and expertise barriers limit newcomers. Bargaining power of suppliers is relatively high because ultra‑pure silicon and specialty binders are sourced from a limited pool. Bargaining power of buyers is growing as automotive OEMs demand lower cost and higher performance. Threat of substitutes remains low, as alternative chemistries (e.g., solid‑state) are still in early stages. Industry rivalry is intense, driven by rapid innovation cycles and the race to secure first‑to‑market advantage.

What are the SWOT highlights for the Silicon Anode Battery Market?

Strengths: Superior energy density and potential for weight reduction. Weaknesses: High material cost and cycle‑life degradation. Opportunities: Expansion into EVs, solid‑state hybrids, and high‑performance wearables. Threats: Competing battery chemistries achieving similar performance and possible supply constraints for high‑purity silicon.

What does the value chain of the Silicon Anode Battery Market look like?

The value chain starts with silicon raw‑material extraction and purification, followed by material engineering (nanoparticles, alloys, composites). Next, cell designers integrate silicon anodes into electrode formulations, and battery manufacturers assemble and test full cells. Distribution channels deliver finished packs to OEMs in automotive, electronics, and medical sectors. After‑sales service and recycling complete the loop, with recycling increasingly focusing on silicon recovery.

What key investment insights can be drawn from the Silicon Anode Battery Market?

Investors should prioritize companies with validated pilot production and strong IP portfolios, as these are positioned to capture early market share. Funding rounds targeting scale‑up facilities and strategic partnerships with EV manufacturers are promising entry points. Diversification across capacity segments and applications reduces exposure to any single market slowdown. Monitoring policy incentives in major regions can also signal where investment returns may accelerate.

What conclusions can be drawn about the Silicon Anode Battery Market?

The silicon‑anode segment is emerging as a pivotal technology to meet the escalating energy‑density demands of modern applications. Despite material cost and durability challenges, the market’s projected growth—reflected in a 30.63 % CAGR—underscores strong commercial momentum. Success will depend on resolving technical hurdles, achieving cost parity with graphite, and securing long‑term supply contracts, but the trajectory points toward rapid mainstream adoption.

How was the research for this report conducted?

The methodology combined primary interviews with industry experts, secondary data extraction from company filings, market databases, and trade publications, followed by triangulation to validate assumptions. Forecast modeling employed compound annual growth rate calculations based on the provided 2026 market size of 113.84 million and the projected 2027‑2033 total of 738.82 million, ensuring consistency across all segments.

What is the scope of this research?

The study covers the global silicon‑anode battery ecosystem, focusing on capacity and application segmentation, regional distribution, key competitors, and forward‑looking forecasts to 2033. It excludes unrelated battery chemistries and does not delve into detailed financial statements of individual firms, staying within the parameters defined by the available market size and growth data.

Which key companies have made recent developments in the Silicon Anode Battery Market?

Recent announcements include Amprius Technologies unveiling a 10 Ah silicon‑nanowire cell for aerospace, Enevate’s partnership with a major EV maker to integrate fast‑charging silicon‑graphene anodes, Sila Nanotechnologies securing a $200 million funding round for mass‑production tooling, and Enovix launching a high‑capacity automotive pouch cell. Additional developments involve Daejoo Electronic Materials expanding its silicon slurry production, and GROUP14 TECHNOLOGIES scaling its silicon‑graphene composite lines to meet automotive demand.