What is the Content Disarm and Reconstruction Market Overview - Definition, scope, and significance?

Content Disarm and Reconstruction (CDR) refers to a cybersecurity technology that removes potentially malicious code from files and data streams while preserving the original, usable content. The market covers solutions that intercept, sanitize, and rebuild files across various vectors such as web uploads, email attachments, FTP transfers, and removable media. Its scope includes both software products and related services, delivered via on‑premise installations or cloud platforms, and serves organizations of all sizes—from SMEs to large enterprises. The significance of CDR lies in its proactive approach to neutralizing zero‑day threats, ransomware, and advanced persistent attacks that bypass traditional signature‑based defenses, thereby protecting critical data, ensuring compliance, and reducing breach‑related costs.

What are the Content Disarm and Reconstruction Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the rising frequency of file‑based attacks, increasing regulatory pressure on data protection, and the shift toward remote work that expands the attack surface. Restraints stem from high initial deployment costs and limited awareness among smaller firms. Challenges involve integrating CDR with legacy security stacks and managing latency for real‑time sanitization. Opportunities arise from growing demand for cloud‑based CDR services, the emergence of AI‑enhanced disarm techniques, and expanding use cases in IoT and industrial control systems where file integrity is critical.

What are the Content Disarm and Reconstruction Market Growth Trends?

Current trends show a rapid adoption of cloud‑native CDR solutions that offer scalability and subscription pricing, catering to both SMEs and large enterprises. Providers are increasingly bundling CDR with broader secure content management suites, enabling unified policy enforcement across email, web, and file‑transfer gateways. Another emerging trend is the integration of machine‑learning models that can predict and prioritize high‑risk file types, improving processing efficiency. Lastly, the market is witnessing consolidation, with larger cybersecurity firms acquiring niche CDR vendors to expand their attack‑surface‑reduction portfolios.

How has COVID‑19 impacted the Content Disarm and Reconstruction Market?

The pandemic accelerated digital transformation, prompting organizations to adopt remote work tools and increase reliance on file sharing. This surge in data exchange heightened exposure to malicious files, driving a notable uptick in CDR deployments in 2020‑2021. While supply‑chain disruptions briefly slowed vendor onboarding, the recovery trajectory has been strong, with renewed focus on securing outbound and inbound content as hybrid work models become permanent.

What does the Content Disarm and Reconstruction Market Competitive Landscape look like?

The competitive landscape features a mix of established network security giants and specialized CDR innovators. Major players such as Broadcom, Cisco Systems, and Fortinet leverage their broad security portfolios to cross‑sell CDR capabilities, whereas firms like OPSWAT and Resec Technologies focus on deep‑tech disarm engines. Recent market consolidation includes strategic acquisitions that integrate CDR into unified threat management solutions, reinforcing the trend toward comprehensive, platform‑centric offerings.

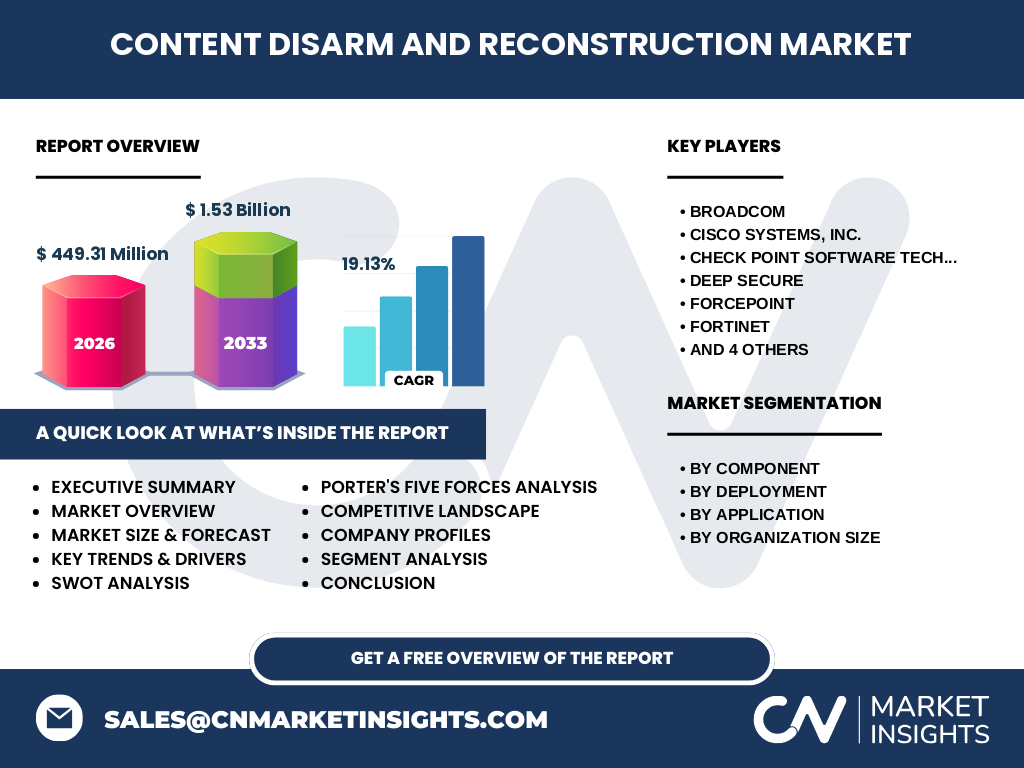

What are the key findings in the Executive Summary of the Content Disarm and Reconstruction Market?

The market is projected to grow from a 2026 valuation of $449.31 million to $1.53 billion by 2033, reflecting a robust CAGR of 19.13 %. Growth is propelled by heightened awareness of file‑based threats, regulatory mandates, and the proliferation of cloud services. Software remains the dominant component, while cloud deployment is outpacing on‑premise models. The market is geographically diverse, with strong adoption in North America and Europe, and emerging traction in APAC. Competitive dynamics point to increasing consolidation and innovation around AI‑driven sanitization.

What is the forecast for the Content Disarm and Reconstruction Market from 2025 to 2032?

Based on the provided CAGR of 19.13 %, the market is expected to maintain double‑digit growth through 2032. The forecast indicates continued expansion of both software licenses and managed services, with cloud‑based subscriptions capturing a larger share of new revenue. Organizational demand from large enterprises will sustain high‑value contracts, while SMEs will drive volume growth through subscription pricing models. The outlook remains positive, supported by evolving threat vectors and expanding regulatory requirements.

How is the Content Disarm and Reconstruction Market sized and shared by segmentation?

Segmentation is organized by component, deployment, application, and organization size. By component, software solutions dominate the revenue mix, complemented by professional and managed services. Deployment analysis shows cloud solutions gaining ground over traditional on‑premise installations. Application‑wise, web and email channels account for the largest usage, followed by FTP and removable‑device scenarios. Lastly, large enterprises contribute the bulk of revenue, while SMEs represent a fast‑growing segment due to affordable cloud subscription options.

What is the Global Content Disarm and Reconstruction Market size and share by region?

The market exhibits a worldwide footprint, with North America leading in absolute revenue owing to early CDR adoption and mature security spending. Europe follows closely, driven by stringent data‑privacy regulations. The Asia‑Pacific region shows the highest growth potential, as enterprises accelerate digital transformation and adopt cloud‑first strategies. While specific monetary shares are not disclosed, the geographic distribution reflects a balanced mix of mature and emerging markets.

What are the detailed regional analyses of the Content Disarm and Reconstruction Market?

In North America, demand is fueled by large‑scale enterprise migrations to hybrid cloud environments and intensive compliance programs. Europe’s market is characterized by strong government directives on data integrity, encouraging widespread CDR deployment across financial and healthcare sectors. APAC’s expansion is led by rapid cloud adoption in China, Japan, and India, where organizations seek scalable CDR services to protect burgeoning digital ecosystems. Latin America and the Middle East show nascent but growing interest, primarily in regulated industries.

Who are the leading companies in the Content Disarm and Reconstruction Market and what are their strategies?

Key players include Broadcom, Cisco Systems, Check Point Software Technologies, Deep Secure, Forcepoint, Fortinet, JiranSecurity, OPSWAT, Resec Technologies, and Sasa Software. Their strategies focus on product integration—embedding CDR into broader security platforms—expanding cloud service offerings, pursuing strategic acquisitions to bolster disarm technology, and targeting verticals with high compliance needs such as finance, healthcare, and government. Partnerships with cloud service providers further extend market reach.

How does Porter’s Five Forces analysis apply to the Content Disarm and Reconstruction Market?

Threat of new entrants is moderate; high technical barriers and the need for deep security expertise deter newcomers, yet cloud‑native startups can leverage SaaS models. Bargaining power of buyers is growing as SMEs gain access to multiple subscription options, increasing price sensitivity. Bargaining power of suppliers is low, because most components are software‑based and can be developed in‑house. Threat of substitutes remains limited; traditional anti‑virus and sandbox tools do not provide the same proactive sanitization. Industry rivalry is intense, with major vendors competing on integration depth, AI capabilities, and pricing flexibility.

What is the SWOT analysis of the Content Disarm and Reconstruction Market?

Strengths: Proven effectiveness against zero‑day and file‑based attacks; growing regulatory demand; strong vendor expertise. Weaknesses: Perceived latency in file processing; higher upfront costs for on‑premise solutions. Opportunities: Expansion of cloud‑based CDR services; AI‑enhanced disarm algorithms; untapped APAC and vertical markets. Threats: Emerging alternative file‑sanitization technologies; possible market saturation; evolving attacker techniques that attempt to bypass CDR.

What does the Value Chain analysis reveal about the Content Disarm and Reconstruction Market?

The value chain begins with research and development of disarm engines, followed by software engineering and integration with existing security stacks. Next, vendors provide licensing or subscription models, complemented by professional services for deployment, configuration, and training. Ongoing support and managed‑service offerings create recurring revenue streams. Finally, feedback loops from customers drive continuous improvement and feature enhancements, reinforcing the cycle of innovation.

What key investment insights can be drawn for the Content Disarm and Reconstruction Market?

Investors should prioritize companies that demonstrate strong cloud transition capabilities and have established partnerships with major platform providers. Look for firms with robust AI roadmaps, as predictive sanitization is a differentiator. Acquisitions of niche CDR specialists can accelerate market share and technology depth. Finally, targeting vendors with diversified vertical exposure reduces dependency on any single industry’s regulatory cycles.

What is the conclusion of the Content Disarm and Reconstruction Market report?

The CDR market is on a rapid growth trajectory, underpinned by a 19.13 % CAGR and a projected rise to $1.53 billion by 2033. Its relevance is reinforced by escalating file‑based threats, regulatory pressures, and the shift to cloud environments. While challenges such as integration complexity remain, the market presents compelling opportunities for vendors, investors, and end‑users seeking resilient, proactive file protection.

How was the research methodology designed for this Content Disarm and Reconstruction Market study?

The methodology combined primary interviews with industry experts, vendor surveys, and secondary data collection from reputable market databases, financial reports, and regulatory publications. Quantitative data were validated through triangulation, while qualitative insights were synthesized to identify trends, drivers, and competitive dynamics. Forecast modeling applied the stated CAGR of 19.13 % to extrapolate future market size.

What is the scope of the research for the Content Disarm and Reconstruction Market?

The research covers the global CDR market, segmented by component (software, services), deployment (on‑premise, cloud), application (web, email, FTP, removable devices), and organization size (SMEs, large). Geographic coverage includes all major regions. Limitations are confined to publicly available data and disclosed financial figures; proprietary vendor data beyond the provided market size and forecast were not incorporated.

Who are the key companies and what recent developments have occurred in the Content Disarm and Reconstruction Market?

The leading firms—Broadcom, Cisco Systems, Check Point, Deep Secure, Forcepoint, Fortinet, JiranSecurity, OPSWAT, Resec Technologies, and Sasa Software—have announced several notable initiatives. Broadcom expanded its CDR suite through integration with its broader security portfolio. Cisco launched a cloud‑first CDR service targeting remote‑work environments. Check Point introduced AI‑driven policy automation for file sanitization. Deep Secure unveiled a next‑generation disarm engine optimized for low‑latency web traffic. Forcepoint secured a partnership with a major cloud provider to deliver managed CDR services. Fortinet incorporated CDR capabilities into its next‑generation firewall line‑up. OPSWAT released a new API that simplifies integration with DevOps pipelines. Resec Technologies announced a strategic acquisition of a regional vendor to strengthen its APAC presence. These developments reflect a dynamic market focused on innovation, partnership, and geographic expansion.