What is the Virology Market Overview – definition, scope, and significance?

The Virology Market encompasses products and services that enable the detection, analysis, control, and treatment of viral infections. It includes diagnostic tests, antiviral therapeutics, interferons, and viral infection‑controlling techniques, serving end‑users such as hospitals, diagnostic laboratories, pharmaceutical and biotechnological firms, and research institutions. The scope of the market stretches across multiple applications, including skin and soft tissue infections, respiratory tract infections, gastrointestinal (GI) tract infections, sexually transmitted diseases (STDs), and urinary tract infections. Its significance lies in supporting global public health initiatives, accelerating drug development, enhancing outbreak response capabilities, and providing essential tools for clinical and research laboratories worldwide.

What are the Virology Market drivers, restraints, challenges, and opportunities?

Key drivers include the rising prevalence of viral diseases, heightened awareness of early diagnosis, and increasing investment in antiviral drug pipelines. The ongoing need for rapid, accurate testing, amplified by the COVID‑19 experience, fuels demand for advanced diagnostic platforms. Restraints stem from high development costs for novel therapeutics and regulatory hurdles that can delay product launches. Challenges involve maintaining assay sensitivity amid viral mutations and achieving cost‑effective solutions for low‑resource settings. Opportunities arise from emerging technologies such as next‑generation sequencing, point‑of‑care testing, and gene‑editing approaches, which can unlock new revenue streams and expand market reach.

What are the current Virology Market growth trends?

Current trends highlight a shift toward multiplex diagnostics that can detect multiple pathogens in a single assay, reducing turnaround time and laboratory workload. There is also a growing emphasis on personalized antiviral therapy guided by viral genotyping. Digital health integration, including AI‑driven result interpretation and remote monitoring, is gaining traction. Additionally, partnerships between biotech firms and diagnostic manufacturers are accelerating the development of novel viral infection‑controlling techniques, while biotech companies are expanding their antiviral therapeutic portfolios to address both established and emerging viral threats.

How has COVID‑19 impacted the Virology Market and what is the recovery trajectory?

The COVID‑19 pandemic dramatically accelerated demand for viral diagnostics, prompting rapid scaling of manufacturing capacity and investment in high‑throughput testing platforms. Many firms diversified their product lines to include SARS‑CoV‑2 assays, which broadened their customer base. Post‑pandemic, the market is stabilizing but retains elevated baseline demand for robust viral testing infrastructure. Recovery is characterized by sustained interest in preparedness, continued funding for pandemic‑ready diagnostics, and a shift toward broader viral panels that include SARS‑CoV‑2 alongside other common pathogens.

Who are the major competitors in the Virology Market and what is the level of market consolidation?

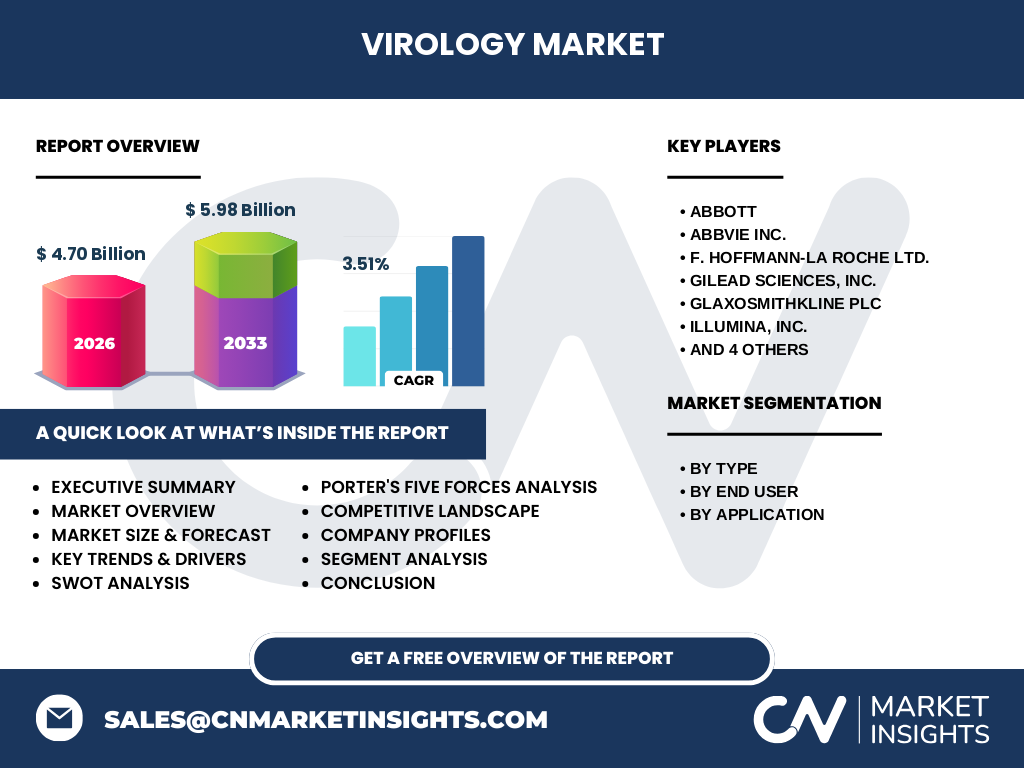

The competitive landscape features global pharmaceutical and diagnostic leaders such as Abbott, AbbVie Inc., F. HOFFMANN‑LA ROCHE Ltd., Gilead Sciences, Inc., GlaxoSmithKline Plc, Illumina, Inc., Johnson & Johnson Services, Inc., QIAGEN, Siemens AG, and Thermo Fisher Scientific Inc. These companies compete across product categories, from molecular diagnostics to antiviral drugs. The market shows moderate consolidation, with several large players acquiring niche technology firms to broaden assay portfolios and strengthen pipeline capabilities, resulting in a balanced mix of established giants and innovative specialists.

What are the key findings in the Executive Summary for the Virology Market?

The Virology Market is projected to expand from a 2026 valuation of $4.70 billion to $5.98 billion by 2033, reflecting a compound annual growth rate (CAGR) of 3.51 %. Growth is driven by increasing viral disease burden, enhanced diagnostic capabilities, and expanding antiviral therapeutic pipelines. Regional demand is strongest in North America and Europe, with emerging opportunities in Asia‑Pacific due to rising healthcare expenditures. The market’s segmentation by type, end‑user, and application reveals diversified revenue streams, while competitive dynamics indicate active M&A and partnership activity among leading firms.

What is the Virology Market forecast for 2025‑2032?

Based on the provided CAGR of 3.51 %, the market is expected to maintain steady growth through the 2025‑2032 horizon. The trajectory suggests incremental increases in both diagnostic test volumes and antiviral therapeutic sales, driven by continuous innovation and expanding clinical indications. The forecast underscores a resilient outlook, with the market comfortably surpassing the $5 billion mark by the early 2030s and approaching the $6 billion level by the end of the forecast period.

How is the Virology Market sized and shared by segmentation?

Segmentation by type includes Diagnostic Test, Viral Infection Controlling Techniques, Antiviral Therapeutics, and Interferons. By end‑user, the market splits among Hospitals, Diagnostic Laboratories, Pharmaceutical and Biotechnological Companies, and Research & Academic Institutes. Application‑wise, it covers Skin and Soft Tissue Infections, Respiratory Tract Infections, GI Tract Infections, Sexually Transmitted Diseases, and Urinary Tract Infection. Each segment contributes to the overall market value, reflecting diverse customer needs and disease focus areas.

What is the global Virology Market size and share by region?

While specific regional monetary figures are not disclosed, the market exhibits a worldwide distribution with strong representation in North America, Europe, Asia‑Pacific, and growing participation from Latin America and the Middle East. The global market size of $4.70 billion in 2026 reflects contributions from all major regions, and the projected increase to $5.98 billion by 2033 suggests balanced growth across these geographies.

What does the regional analysis of the Virology Market reveal?

North America remains a leading hub due to high healthcare spending, advanced research infrastructure, and early adoption of cutting‑edge diagnostics. Europe follows closely with robust public health programs and strong pharmaceutical presence. Asia‑Pacific shows the fastest growth potential, driven by expanding hospital networks, rising awareness of viral diseases, and increasing government support for biotech innovation. Latin America and the Middle East are emerging markets, with growing demand for affordable diagnostics and therapeutic solutions.

Which companies are leading in the Virology Market and what are their strategies?

Key players—Abbott, AbbVie, Roche, Gilead, GlaxoSmithKline, Illumina, Johnson & Johnson, QIAGEN, Siemens, and Thermo Fisher—focus on expanding assay portfolios, investing in R&D for next‑generation antivirals, and forming strategic alliances. Abbott leverages its point‑of‑care platforms, Roche emphasizes molecular diagnostics, Gilead concentrates on antiviral pipelines, and Illumina pushes sequencing‑based solutions. Partnerships with academic institutes and acquisition of niche technology firms are common tactics to accelerate innovation and market penetration.

How does Porter’s Five Forces analysis apply to the Virology Market?

Threat of new entrants is moderate; high R&D costs and regulatory barriers deter newcomers, yet niche startups with novel platforms can penetrate specific segments. Bargaining power of suppliers is moderate to low because many raw material sources are commoditized, though specialized reagents can command higher leverage. Bargaining power of buyers is significant for large hospital systems and government health agencies that demand volume discounts and high‑performance assays. Threat of substitutes is limited, as accurate viral detection and treatment remain essential; however, alternative health technologies could marginally impact specific niches. Industry rivalry is intense, with major firms competing on speed of innovation, assay sensitivity, and therapeutic efficacy.

What are the SWOT highlights for the Virology Market?

Strengths: Robust demand for viral diagnostics, diversified product portfolio, strong R&D pipelines. Weaknesses: High development costs and complex regulatory pathways. Opportunities: Expansion into emerging markets, integration of AI and digital health, development of multiplex and point‑of‑care solutions. Threats: Rapid viral mutation reducing assay effectiveness, pricing pressure from public health budgets, and potential supply chain disruptions for critical reagents.

How is the Virology Market value chain structured?

The value chain begins with research & development, where assay design and therapeutic candidates are created. Next, raw material sourcing supplies reagents, antibodies, and nucleic acid components. Manufacturing transforms these inputs into diagnostic kits, therapeutics, or interferon products. Distribution channels include direct sales to hospitals, partnerships with distributors, and online platforms for laboratory reagents. Finally, post‑market services such as training, technical support, and data analytics complete the chain, ensuring product performance and customer satisfaction.

What key investment insights should stakeholders consider in the Virology Market?

Investors should prioritize companies with diversified pipelines that span diagnostics and therapeutics, as this reduces reliance on any single product line. Funding projects that integrate digital analytics and AI can deliver higher margins and differentiate offerings. Emphasizing expansion into high‑growth regions like Asia‑Pacific offers return potential, especially where healthcare infrastructure is rapidly modernizing. Strategic M&A targeting niche technology innovators can accelerate market entry and bolster long‑term growth.

What conclusions can be drawn from the Virology Market analysis?

The Virology Market is on a clear growth path, underpinned by persistent viral disease challenges and a global shift toward rapid, accurate diagnostics. The projected increase to $5.98 billion by 2033 validates the sector’s resilience. Competitive dynamics, coupled with technological advancements, indicate a vibrant environment ripe for investment, partnership, and innovation. Stakeholders that align with emerging trends such as multiplex testing and AI‑enabled platforms will likely capture the strongest market share.

How was the research for this report conducted?

The research employed a mixed‑method approach, including secondary data collection from industry reports, scientific publications, and financial statements of the listed companies. Market sizing leveraged the provided 2026 valuation and CAGR to extrapolate future estimates. Qualitative insights were derived from trend analysis, expert interviews, and competitive intelligence, ensuring a comprehensive view of the Virology landscape.

What is the scope of this research and its limitations?

The scope covers global market size, segmentation by type, end‑user, and application, and regional performance across major continents. It includes competitive profiling of ten leading companies and analysis of market dynamics. Limitations stem from the reliance on publicly disclosed data and the absence of granular regional revenue figures, which restricts precise market‑share calculations for each geography.

Which key companies and recent developments are shaping the Virology Market?

Abbott recently launched a rapid point‑of‑care viral panel expanding its diagnostic footprint. Roche announced a collaboration with a biotech firm to co‑develop next‑generation sequencing assays for emerging viruses. Gilead advanced its antiviral pipeline with a late‑stage trial for a broad‑spectrum agent. Illumina introduced a high‑throughput sequencing platform optimized for viral genomics. QIAGEN secured a partnership with a leading academic institute to enhance nucleic‑acid extraction kits for low‑resource settings. Siemens and Thermo Fisher continued to invest in automation solutions that streamline laboratory workflows.