1. What is the definition, scope, and significance of the Organic Fertilizers Market?

The Organic Fertilizers Market comprises products derived from natural sources—such as plant, animal, and mineral materials—that enhance soil fertility and crop yields without synthetic chemicals. Its scope spans dry and liquid formulations, serving a wide array of crops including fruits, cereals, turf, and specialty horticulture. Significance lies in meeting rising consumer demand for sustainable agriculture, reducing environmental impact, and complying with stricter government regulations on chemical inputs.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Organic Fertilizers Market?

Key drivers include increasing awareness of soil health, government incentives for organic farming, and a shift toward eco‑friendly practices. Restraints stem from higher upfront costs compared with conventional fertilizers and limited awareness in developing regions. Challenges involve ensuring consistent nutrient content, logistics of bulk organic material handling, and certification complexities. Opportunities arise from technological advances in composting, bio‑stimulators, and expanding organic produce markets in North America, Europe, and Asia‑Pacific.

3. Which current and emerging trends are influencing the growth of the Organic Fertilizers Market?

Current trends feature a surge in premium dry blends that combine multiple organic sources for balanced nutrition, and a rise in liquid concentrates for precision application. Emerging trends include the integration of microbial inoculants, development of slow‑release granules, and adoption of digital platforms for dosage recommendations. Additionally, the use of waste streams—such as food processing residues—as feedstock is gaining traction, supporting circular economy initiatives.

4. How did COVID‑19 affect the Organic Fertilizers Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains, causing temporary shortages of raw organic material and delayed shipments of finished products. However, heightened focus on food security and resilient farming practices accelerated demand for organic inputs. As economies reopened, the market rebounded quickly, supported by government stimulus programs for sustainable agriculture. Recovery is now steady, with growth rates aligning with pre‑pandemic forecasts.

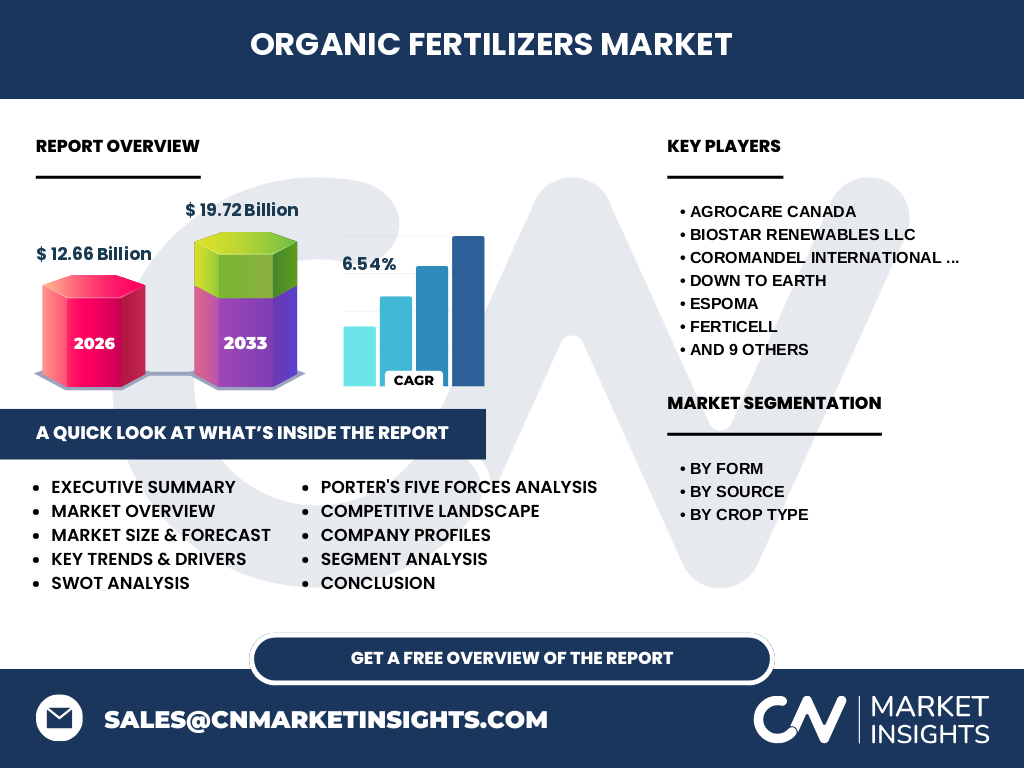

5. Who are the major competitors and what is the level of consolidation in the Organic Fertilizers Market?

Prominent players include Agrocare Canada, Biostar Renewables LLC, Coromandel International Limited, Down To Earth, Espoma, Ferticell, IFFCO, Italpolina SPA, Krishak Bharati Cooperative Limited, Midwestern BioAg, National Fertilizers Limited, Natural Fertilizer Inc, Perfect Blend Biotic Fertilizer, SDF India, and Scotts‑Miracle‑Gro. The market exhibits moderate consolidation, with a mix of large multinational firms and specialized regional producers. Recent mergers and strategic alliances indicate a trend toward strengthening distribution networks and expanding product portfolios.

6. What are the high‑level highlights and key findings of the Organic Fertilizers Market?

The market is valued at USD 12.66 billion in 2026 and is projected to reach USD 19.72 billion by 2033, delivering a CAGR of 6.54 % over the forecast period. Dry and liquid forms both enjoy robust demand, while plant‑based and animal‑based sources dominate the supply mix. Geographic growth is strongest in regions with mature organic standards, yet emerging economies present untapped potential. Innovation, sustainability, and supply‑chain resilience emerge as decisive success factors.

7. What are the forecast expectations for the Organic Fertilizers Market from 2025 to 2032?

Building on the 6.54 % CAGR, the market is expected to maintain steady expansion through 2032. By 2027, revenues will surpass the 2026 baseline, continuing upward momentum each subsequent year. The forecast anticipates incremental adoption across all crop segments, with particular acceleration in high‑value horticulture and turf applications. The outlook remains positive, driven by policy support, consumer preference for organic produce, and ongoing product innovation.

8. How is the Organic Fertilizers Market sized and shared by segmentation?

Segmentation by form divides the market into dry and liquid categories, each serving distinct agronomic needs. By source, products are classified as plant, animal, or mineral‑derived organic fertilizers, reflecting varied nutrient profiles. Crop‑type segmentation spans fruit and vegetables, cereals and grains, turf and ornamental, flowers and nursery, tree crops, legumes, herbs and spices, oilseeds, and tubers and root crops. While exact numeric shares are proprietary, each segment contributes meaningfully to the overall market composition.

9. What is the geographic distribution of the global Organic Fertilizers Market?

The market exhibits a global footprint, with North America and Europe leading due to mature organic certification frameworks and higher consumer willingness to pay premium prices. Asia‑Pacific follows, driven by large agrarian populations and growing regulatory encouragement for sustainable inputs. Latin America and the Middle East show emerging interest, particularly in fruit, vegetable, and export‑oriented horticulture sectors.

10. How does each region perform in the Organic Fertilizers Market?

In North America, the market benefits from strong retail channels and widespread adoption of organic standards. Europe’s performance is bolstered by stringent environmental directives and a well‑established organic farming community. Asia‑Pacific demonstrates rapid growth, propelled by government subsidies and expanding export markets for organic commodities. Latin America’s growth is centered on high‑value crops, while the Middle East and Africa are beginning to explore organic solutions for water‑scarce agriculture.

11. Which companies lead the Organic Fertilizers Market and what strategies do they employ?

Industry leaders such as Scotts‑Miracle‑Gro and IFFCO leverage extensive distribution networks and diversified product lines. Coromandel International focuses on integrating mineral‑derived organics with traditional formulations. Biostar Renewables emphasizes waste‑to‑fertilizer technologies, while Down To Earth prioritizes premium organic blends for horticulture. Strategic initiatives include R&D collaborations, acquisitions of niche brands, and expansion into emerging markets to capture new customer segments.

12. What does Porter’s Five Forces reveal about the Organic Fertilizers Market?

Threat of new entrants is moderate; capital requirements for processing and certification create barriers, yet niche innovators can enter with specialized products. Bargaining power of suppliers is moderate, as raw organic materials are sourced from agriculture and waste streams, which can be regionally variable. Bargaining power of buyers is growing, especially among large agribusinesses demanding price transparency. Threat of substitutes is low to moderate; synthetic fertilizers remain alternatives but face regulatory headwinds. Industry rivalry is high, driven by product differentiation, branding, and geographic expansion.

13. What are the strengths, weaknesses, opportunities, and threats (SWOT) of the Organic Fertilizers Market?

Strengths include alignment with sustainability trends and increasing consumer demand for organic produce. Weaknesses involve higher production costs and variability in nutrient content. Opportunities arise from technological advances in bio‑formulations, waste‑upcycling, and expanding certification schemes. Threats encompass potential regulatory changes, supply chain disruptions, and competition from cost‑effective synthetic fertilizers.

14. How is the value chain structured in the Organic Fertilizers Market?

The value chain starts with raw material acquisition—plant residues, animal manure, and mineral by‑products—followed by processing steps such as composting, drying, granulation, or liquid extraction. Subsequent stages involve formulation, quality testing, packaging, and distribution through agricultural input retailers, cooperatives, and direct farm sales. End‑users (farmers, horticulturists, landscapers) apply the products, generating feedback that informs R&D and supply‑chain optimization.

15. What investment insights can be drawn for stakeholders interested in the Organic Fertilizers Market?

Investors should prioritize companies with strong R&D pipelines, diversified raw‑material sources, and scalable manufacturing capabilities. Strategic partnerships with waste‑management firms can enhance raw material security and reduce costs. Geographic diversification—especially into fast‑growing Asia‑Pacific markets—offers upside potential. Monitoring policy developments and certification trends will help identify regulatory catalysts that can boost market demand.

16. What are the key takeaways and conclusions from the Organic Fertilizers Market analysis?

The Organic Fertilizers Market is on a solid growth trajectory, projected to expand from USD 12.66 billion in 2026 to USD 19.72 billion by 2033 at a 6.54 % CAGR. Sustainable agriculture, regulatory support, and consumer preferences drive this expansion. While cost and supply challenges persist, innovation and strategic collaboration are unlocking new opportunities across all crop categories and regions. Stakeholders who align with these dynamics are positioned for long‑term value creation.

17. How was the research for this report conducted?

The methodology combined primary interviews with industry experts, secondary analysis of publicly available financial statements, market reports, and trade publications. Data triangulation ensured consistency across sources. Quantitative forecasting employed compound annual growth rate calculations based on the provided market size figures (USD 12.66 billion in 2026 and USD 19.72 billion forecast for 2033). Qualitative insights were derived from trend monitoring and competitive intelligence.

18. What is the scope of this research and its limitations?

The scope covers global organic fertilizer offerings, segmented by form, source, and crop type, and includes regional performance, competitive landscape, and forward‑looking forecasts through 2033. Limitations arise from the reliance on publicly disclosed data and the absence of proprietary market share percentages. Consequently, the analysis emphasizes trends, growth drivers, and strategic implications rather than precise numeric breakdowns.

19. Which key companies have made recent developments in the Organic Fertilizers Market?

Recent announcements include Scotts‑Miracle‑Gro launching a line of liquid organic concentrates tailored for precision irrigation, while IFFCO introduced a plant‑based granular blend with enhanced micronutrient content. Biostar Renewables secured a partnership with a major food‑processing firm to convert waste streams into premium organic fertilizer. Coromandel International announced a joint venture focused on mineral‑derived organics for cereal crops. These developments underscore ongoing innovation and collaboration across the industry.