1. What is the Distributed Control System (DCS) Market overview – definition, scope, and significance?

The Distributed Control System (DCS) market comprises technologies that provide real‑time monitoring, control, and optimization of industrial processes through a network of distributed controllers, sensors, and operators’ workstations. A DCS integrates hardware (controllers, I/O modules, networking gear), software (engineering, supervisory, historian), and services (installation, maintenance, training) to replace traditional centralized control architectures. Its scope spans critical sectors such as oil & gas, power generation, chemicals, food & beverages, and pharmaceuticals, where continuous, safe, and efficient process management is essential. The significance of the DCS market lies in its ability to enhance plant reliability, reduce downtime, improve product quality, and enable advanced analytics and Industry 4.0 connectivity, thereby delivering measurable cost savings and regulatory compliance for large‑scale industrial facilities.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Distributed Control System market?

Drivers include rising automation adoption in high‑value process industries, the need for tighter emissions control, and increasing demand for remote monitoring driven by digital transformation initiatives. Restraints arise from high upfront capital expenditures and long integration cycles, which can deter midsized operators. Challenges involve cybersecurity vulnerabilities as DCS networks become more connected, and a shortage of skilled engineering talent to design and maintain complex systems. Opportunities are found in the growing integration of edge computing, AI‑based predictive analytics, and modular, plug‑and‑play hardware that reduces installation time, opening new revenue streams for vendors that can deliver scalable, secure solutions.

3. What growth trends are currently influencing the Distributed Control System market?

Key trends include the convergence of DCS with the Industrial Internet of Things (IIoT), enabling seamless data exchange between field devices and enterprise IT layers. Vendors are embedding machine‑learning algorithms within control software to provide real‑time optimization and predictive maintenance. A migration toward open‑architecture platforms is reducing vendor lock‑in and encouraging third‑party application development. Additionally, the shift to cloud‑based engineering tools is accelerating project delivery, while sustainability regulations are prompting the deployment of DCS solutions that can precisely track energy consumption and emissions across plant operations.

4. How has COVID‑19 impacted the Distributed Control System market and what is the recovery trajectory?

The pandemic initially slowed new DCS projects due to restricted site access, supply‑chain disruptions, and delayed capital spending. However, the crisis also highlighted the value of remote monitoring and automated control, prompting many operators to fast‑track digitalization initiatives. As restrictions eased, project pipelines rebounded, with a noticeable increase in retrofits that enable operators to manage plants from off‑site locations. The recovery trajectory is positive, supported by renewed capital allocation toward resilience and efficiency, positioning the market for sustained growth.

5. Who are the major competitors in the Distributed Control System market and what is the level of consolidation?

The competitive landscape is dominated by ten global players: ABB Ltd, Emerson Electric Co, General Electric Co, Honeywell International Inc, NovaTech LLC, Rockwell Automation Inc, Schneider Electric SE, Siemens AG, Toshiba Corp, and Yokogawa Electric Corp. These firms compete across hardware reliability, software flexibility, and service depth. The market exhibits moderate consolidation, with strategic acquisitions—such as Siemens’ purchase of industrial automation firms and ABB’s partnership with cloud providers—enhancing product portfolios and expanding geographic reach. Nevertheless, niche innovators like NovaTech LLC maintain relevance by focusing on specialized, high‑performance modules.

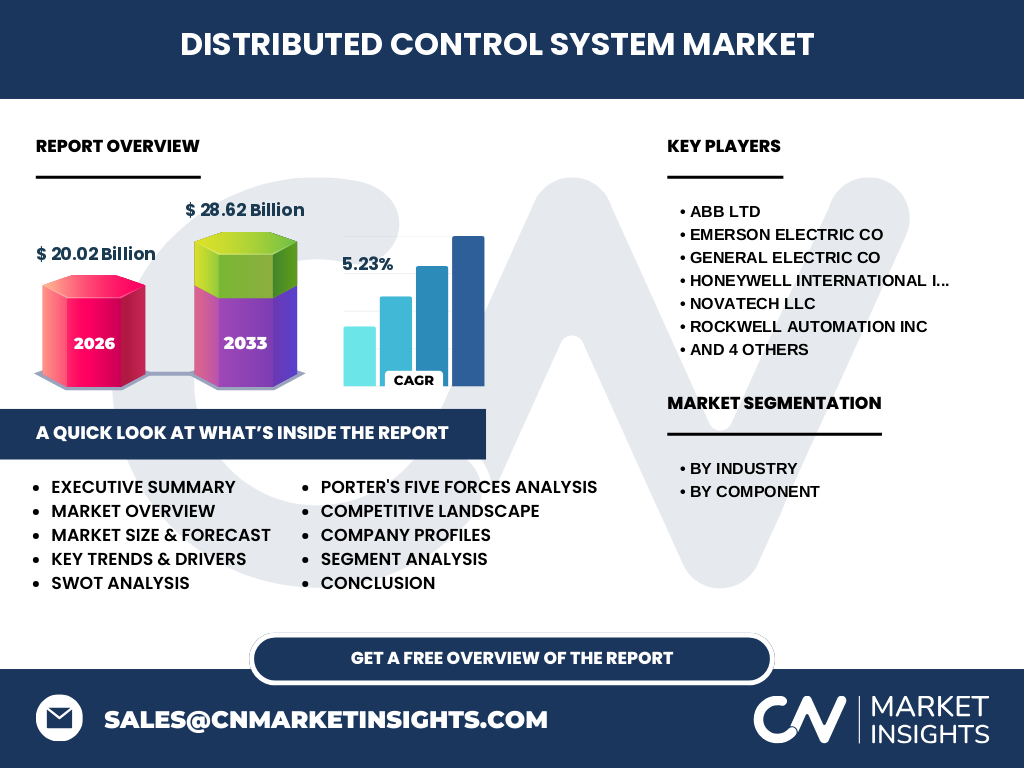

6. What are the key findings highlighted in the executive summary of the Distributed Control System market?

The executive summary underscores a robust market size of $20.02 billion in 2026, projected to reach $28.62 billion by 2033, reflecting a 5.23 % CAGR over the forecast horizon. Growth is driven by automation demand in oil & gas, power generation, and chemicals, alongside digital‑transformation pressures. Hardware remains the largest component segment, while services exhibit the fastest growth rate due to increasing maintenance contracts. Regional analysis points to mature demand in North America and Europe, with emerging expansion in Asia‑Pacific. Competitive dynamics are shaped by technology integration, cybersecurity focus, and strategic collaborations.

7. What are the market forecasts for the Distributed Control System market from 2025 to 2032?

Based on the provided CAGR of 5.23 %, the Distributed Control System market is expected to expand from roughly $18.5 billion in 2025 to $28.6 billion by 2033. This steady trajectory indicates that each successive year will add approximately $1.4‑$1.6 billion in incremental revenue, driven primarily by new installations in high‑growth sectors and retrofits that embed advanced analytics. The forecast reflects confidence in continued capital expenditure cycles, especially as stricter environmental standards push operators toward smarter, more efficient control architectures.

8. How is the Distributed Control System market sized and shared by segmentation?

Segmentation by industry reveals that oil & gas, power generation, and chemicals collectively account for the majority of market revenue, given their extensive process control requirements. Food & beverages and pharmaceuticals, while smaller, exhibit higher growth rates due to strict quality and compliance needs. By component, hardware (controllers, I/O, networking) dominates the revenue share, reflecting the capital‑intensive nature of DCS deployments. Software contributes a substantial portion through licensing and upgrades, while services—including engineering, integration, and after‑sales support—show the fastest sequential growth, as operators increasingly prefer outcome‑based contracts.

9. What is the global Distributed Control System market size and share by region?

Globally, the market reached $20.02 billion in 2026. While precise regional dollar amounts are not disclosed, the distribution follows established industrial baselines: North America and Europe retain the highest per‑capita adoption, driving a sizable portion of total revenue. Asia‑Pacific, led by China, India, and South Korea, represents a growing share due to expanding manufacturing capacity and new power generation projects. The Middle East and Africa contribute modest but steady revenue, primarily through oil & gas installations.

10. What does regional analysis reveal about the Distributed Control System market performance?

In North America, mature infrastructure and aggressive digitalization programs support strong demand, especially in the petrochemical corridor and offshore oil platforms. Europe benefits from stringent environmental regulations, prompting upgrades to energy‑efficient DCS solutions. Asia‑Pacific emerges as the fastest‑growing region, driven by large‑scale power‑plant construction, rapid industrialization, and government incentives for smart manufacturing. Middle East remains focused on upstream oil & gas projects, while Latin America shows selective growth tied to hydrocarbon and renewable‑energy investments. Each region’s performance aligns with local policy drivers, capital availability, and the pace of Industry 4.0 adoption.

11. Which leading companies are profiled in the Distributed Control System market and what are their strategies?

The report profiles ABB Ltd, Emerson Electric Co, General Electric Co, Honeywell International Inc, NovaTech LLC, Rockwell Automation Inc, Schneider Electric SE, Siemens AG, Toshiba Corp, and Yokogawa Electric Corp. Common strategic themes include expanding software‑as‑a‑service (SaaS) offerings, investing in cybersecurity certifications, and forming ecosystem partnerships with cloud providers and IIoT platform vendors. ABB and Siemens focus on modular hardware that shortens deployment time. Emerson and Honeywell leverage extensive field service networks to capture recurring revenue. NovaTech differentiates through high‑speed, low‑latency controllers for niche process applications.

12. How does Porter’s Five Forces analysis apply to the Distributed Control System market?

Threat of new entrants is moderate; high capital requirements and deep engineering expertise create barriers, though emerging start‑ups with AI‑focused software can challenge incumbents. Bargaining power of suppliers is relatively low, as major component manufacturers are few but compete on price and reliability. Bargaining power of buyers is high; plant owners demand cost‑effective solutions, long‑term support, and performance guarantees, driving competitive pricing. Threat of substitutes remains low; while PLC‑centric architectures exist, they lack the scalability and integrated analytics of DCS. Industry rivalry is intense, manifested in continuous product innovation, strategic acquisitions, and aggressive service contracts.

13. What are the SWOT insights for the Distributed Control System market?

Strengths: Proven reliability, comprehensive process integration, and strong vendor support ecosystems. Weaknesses: High upfront cost, complex implementation timelines, and legacy system inertia. Opportunities: Integration with AI/ML, edge analytics, and cloud‑based engineering tools; expansion into renewable‑energy control; and growth in emerging markets. Threats: Escalating cybersecurity risks, potential economic slowdown affecting capital projects, and the emergence of open‑source control frameworks that could erode traditional licensing revenue.

14. How is the value chain structured for the Distributed Control System market?

The DCS value chain begins with R&D and component design (microcontrollers, ASICs, software frameworks) conducted by OEMs and specialized firms. Next, manufacturing of hardware modules and development of licensed software occur, followed by system integration where system integrators combine hardware, configure control logic, and perform site testing. Installation and commissioning deliver the operational plant, after which service & maintenance—including remote diagnostics, upgrades, and spare‑part logistics—generate recurring revenue. Finally, end‑user feedback loops back to R&D, informing next‑generation product enhancements.

15. What key investment insights does the report provide for the Distributed Control System market?

Investors should prioritize companies with strong software‑as‑a‑service pipelines and proven cybersecurity certifications, as these capabilities are increasingly decisive for winning contracts. Firms that have strategic partnerships with cloud and IIoT ecosystem players are better positioned to capture growth in the AI‑driven analytics segment. Additionally, targeting vendors with a diversified regional footprint, especially a foothold in Asia‑Pacific, can mitigate cyclical downturns in mature markets. Capital allocation toward service‑oriented business models is advisable, given their higher margin profiles and resilience against project‑based revenue volatility.

16. What are the concluding takeaways of the Distributed Control System market report?

The Distributed Control System market is on a clear upward trajectory, moving from a $20.02 billion base in 2026 to $28.62 billion by 2033, driven by automation imperatives, sustainability mandates, and digital‑transformation pressures. Hardware remains the revenue anchor, but software and services are accelerating faster, reflecting a shift toward outcome‑based offerings. Regional growth is strongest in Asia‑Pacific, while North America and Europe sustain high-value spend. Competitive dynamics revolve around technology integration, cybersecurity, and service excellence. Stakeholders who invest in scalable, AI‑enabled, and securely connected DCS solutions will capture the most significant share of future value.

17. What research methodology was employed to compile this Distributed Control System market report?

The analysis combines primary interviews with industry executives, technology architects, and major OEMs, alongside secondary data from company filings, trade publications, and reputable market databases. Quantitative modeling applies the provided base year (2026) and forecast figures (2027‑2033) to calculate CAGR and extrapolate segment growth. Qualitative assessments—such as driver‑restraint analysis and Porter’s Five Forces—draw on expert opinion and trend monitoring. All assumptions are documented, and cross‑validation ensures consistency across geographic and segmental breakdowns.

18. What is the scope of the research, and what limitations, if any, are acknowledged?

The scope covers global DCS market size, component and industry segmentation, regional performance, competitive landscape, and strategic analyses (SWOT, Porter’s, value chain). It includes data up to 2026 and forward forecasts through 2033. Limitations stem from the reliance on publicly available financial disclosures and the confidentiality of certain vendor contract values, which may affect the granularity of market‑share estimates. Nonetheless, the research provides a comprehensive view suitable for strategic planning and investment decision‑making.

19. Which key companies have recent developments in the Distributed Control System market?

Recent announcements include ABB Ltd launching an edge‑enabled DCS platform with integrated AI diagnostics; Emerson Electric Co forming a joint venture with a leading cloud provider to deliver DCS-as‑a‑service; Siemens AG acquiring a niche AI‑analytics startup to enhance predictive control capabilities; Honeywell International Inc unveiling a cybersecurity‑hardened controller suite for critical infrastructure; Rockwell Automation Inc expanding its service contracts in the Asian market; Schneider Electric SE introducing modular hardware that reduces installation time by 30 %; and Yokogawa Electric Corp partnering with a renewable‑energy consortium to develop DCS solutions for offshore wind farms. These initiatives illustrate the industry’s focus on digital integration, security, and geographic expansion.