What is the Fall Protection Equipment Market Overview – definition, scope, and significance?

The Fall Protection Equipment Market comprises products designed to prevent work‑site injuries or fatalities caused by falls from height. Its scope includes soft goods (lanyards, webbing), hard goods (anchors, railings), rescue kits, body belts, and full‑body harnesses, serving sectors such as construction, transportation, oil & gas, mining, energy & utilities, and telecom. Ensuring worker safety and complying with occupational health regulations make this market strategically vital for employers and regulators worldwide.

What are the market drivers, restraints, challenges, and opportunities?

Key drivers include stricter safety legislation, rising construction activity, and heightened awareness of fall‑related risks. Restraints stem from high equipment costs and limited skilled personnel for proper installation. Challenges involve maintenance of aging infrastructure and geographic variations in compliance enforcement. Opportunities arise from technological advances in lightweight, ergonomic designs, and growing demand for integrated rescue solutions in emerging economies.

What are the current growth trends shaping the market?

Recent trends feature a shift toward smart, sensor‑enabled harnesses that monitor user vitals and location. Manufacturers are expanding modular product lines that combine fall arrest and rescue functions. Sustainable materials are gaining traction, and digital marketplaces are simplifying procurement for contractors. Additionally, after‑market services such as inspection, certification, and training are becoming bundled revenue streams.

How did COVID‑19 impact the Fall Protection Equipment Market and what is the recovery trajectory?

The pandemic caused temporary project delays and supply‑chain disruptions, slowing equipment orders in 2020. However, as construction resumed and safety protocols intensified, demand rebounded sharply. Recovery has been reinforced by heightened emphasis on worker health, leading to accelerated adoption of reliable fall protection solutions and a trajectory that now aligns with pre‑pandemic growth momentum.

What does the competitive landscape look like and are there signs of market consolidation?

The market is moderately fragmented, with a mix of global manufacturers and niche specialists. Leading players such as 3M, Honeywell International, MSA Safety, and Tritech Fall Protection dominate due to broad product portfolios and extensive distribution networks. Recent years have seen strategic alliances and selective acquisitions aimed at expanding technology capabilities and geographic reach, indicating a gradual consolidation trend.

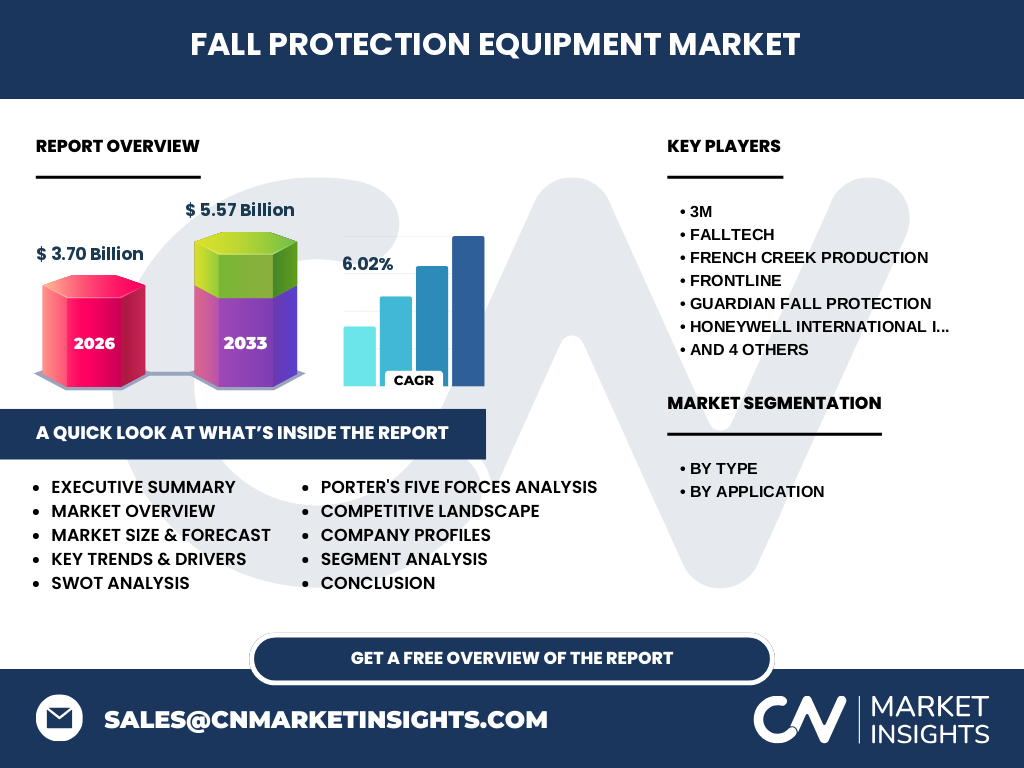

What are the high‑level findings in the executive summary?

The Fall Protection Equipment Market is projected to expand from a 2026 size of $3.70 billion to $5.57 billion by 2033, reflecting a 6.02 % CAGR. Growth is propelled by regulatory pressure, infrastructure development, and innovation in safety gear. The market offers robust opportunities for vendors that can deliver cost‑effective, technologically advanced, and compliance‑ready solutions across diverse applications.

What are the market forecasts for 2025‑2032?

Based on current trajectories, the market will continue to grow at a steady pace, maintaining the 6 % CAGR through 2032. Anticipated drivers include expanding construction projects in Asia‑Pacific, increasing safety standards in oil & gas, and rising adoption of integrated rescue kits. Companies that invest in digital monitoring and lightweight materials are positioned to capture a larger share of this expanding market.

How is the market sized and shared by type and application?

By type, the market is segmented into soft goods, hard goods, rescue kits, body belts, and full‑body harnesses, each addressing distinct safety functions. By application, the primary segments are construction, transportation, oil & gas, mining, energy & utilities, and telecom. While precise numeric splits are proprietary, construction remains the largest demand driver, followed by oil & gas and mining, with soft goods and full‑body harnesses representing the core product categories.

What is the geographic distribution of market size and share?

The market exhibits a global footprint with strong presence in North America, Europe, and the Asia‑Pacific region. North America leads due to mature regulatory frameworks, while Europe follows with stringent safety directives. Rapid infrastructure growth fuels demand in Asia‑Pacific, positioning it as the fastest‑growing region. Emerging markets in Latin America and the Middle East contribute incremental volume as safety standards evolve.

What does the regional analysis reveal about market performance?

North America benefits from high compliance enforcement and substantial construction spending, driving steady volume growth. Europe’s market is characterized by advanced product adoption and frequent retro‑fitting projects. Asia‑Pacific shows the highest growth rate, propelled by large‑scale urbanization, industrial expansion, and increasing awareness of occupational safety. Latin America and the Middle East display emerging potential as local regulations tighten.

Which companies lead the market and what are their key strategies?

Key players include 3M, Falltech, French Creek Production, Frontline, Guardian Fall Protection, Honeycomb International, Kee Safety, KwikSafety, MSA Safety, and Tritech Fall Protection. Strategies focus on expanding product portfolios, investing in R&D for ergonomic designs, pursuing certification partnerships, and leveraging digital sales channels. Several firms are also targeting acquisitions to integrate complementary technologies and broaden geographic coverage.

How does Porter’s Five Forces model apply to this market?

Threat of new entrants is moderate due to high certification costs and established brand loyalty. Supplier power is limited as raw materials are commoditized, though specialized synthetic fibers can command premium pricing. Buyer power is strong because large contractors negotiate volume discounts and demand high-quality, compliant gear. Substitutes are minimal, given the regulatory requirement for dedicated fall protection solutions. Competitive rivalry is intense, driven by product innovation and service differentiation.

What are the SWOT highlights for the Fall Protection Equipment Market?

Strengths: essential safety function, regulatory backing, and ongoing technological innovation. Weaknesses: high unit costs and dependence on skilled installation. Opportunities: growth in emerging economies, integration of IoT sensors, and expansion of rescue‑kit offerings. Threats: economic downturns affecting construction budgets and potential supply‑chain constraints for specialized materials.

What does the value chain of the market look like?

The value chain begins with raw material suppliers (fibers, metal alloys), followed by component manufacturers that produce anchors, webbing, and buckles. These components are assembled into final products by manufacturers. Distribution channels include direct sales to large contractors, distributors, and e‑commerce platforms. After‑sales services—inspection, certification, and training—complete the chain, adding recurring revenue and enhancing product lifecycle management.

What key investment insights can be drawn?

Investors should focus on companies with strong R&D pipelines for smart and lightweight gear, robust distribution networks, and diversified application exposure. Targeting firms that offer bundled services (inspection, training) can yield higher margins. Geographic diversification, especially into high‑growth Asia‑Pacific markets, presents attractive upside, while monitoring regulatory changes can help anticipate demand spikes.

What is the overall conclusion of the market analysis?

The Fall Protection Equipment Market is on a clear growth trajectory, underpinned by safety regulations and expanding infrastructure projects. With a projected CAGR of over 6 % and a market value set to exceed $5.5 billion by 2033, the sector offers compelling opportunities for innovators and investors alike. Companies that combine compliance, technology, and service excellence will lead the market.

How was the research methodology designed?

The study employed a mix of primary interviews with industry experts, secondary data from company reports, regulatory publications, and market databases. Forecasts were generated using compound annual growth rate calculations based on the provided 2026 market size of $3.70 billion and the 2027‑2033 projection of $5.57 billion, applying a 6.02 % CAGR.

What is the scope of the research and its limitations?

The research covers global market dynamics, segmentation by type and application, and regional performance across major territories. It excludes granular market share percentages and country‑level revenue breakdowns due to data constraints. The analysis focuses on publicly available information and validated expert input, ensuring relevance while acknowledging that proprietary sales figures remain undisclosed.

Which key companies have recent developments, product launches, or partnerships?

Recent activities include 3M’s launch of a next‑generation lightweight harness, Honeywell International’s partnership with a digital safety platform for real‑time monitoring, and MSA Safety’s introduction of an integrated rescue kit for the oil & gas sector. Tritech Fall Protection announced an acquisition of a niche rescue‑equipment firm to broaden its service portfolio, while Guardian Fall Protection unveiled a new line of eco‑friendly soft‑goods using recycled polymers.