1. Europe 5G in IoT Market Overview – Definition, scope, and significance?

The Europe 5G in IoT market refers to the deployment and commercialization of fifth‑generation (5G) mobile network technologies that enable a broad spectrum of Internet‑of‑Things (IoT) applications across the continent. It encompasses hardware (short‑range and wide‑range IoT devices), network architectures (5G NR Standalone and Non‑Standalone), and services tailored for verticals such as manufacturing, energy, government, healthcare, transportation, logistics, and mining. The market is significant because 5G delivers ultra‑low latency, massive device connectivity, and enhanced reliability, unlocking new business models, improving operational efficiency, and driving digital transformation throughout European economies.

2. Europe 5G in IoT Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include the EU’s ambitious digital agenda, strong demand for smart manufacturing and Industry 4.0 solutions, and the rollout of private 5G networks for critical infrastructure. Sustainability goals stimulate IoT adoption in energy optimization and smart grids. Restraints stem from high upfront investment costs, fragmented spectrum allocation, and regulatory complexities. Challenges involve ensuring cybersecurity across massive device fleets and addressing skill gaps in 5G deployment. Opportunities arise from emerging use cases such as autonomous logistics, tele‑medicine, and cross‑border 5G‑enabled supply chains that can capitalize on the projected 23.44% CAGR.

3. Europe 5G in IoT Market Growth Trends – Current and emerging trends shaping the market?

Current trends show a rapid shift from public‑network‑centric IoT to private 5G deployments within factories and campuses, driven by the need for ultra‑reliable low‑latency communication. Edge computing integration is emerging to process data locally, reducing latency and bandwidth costs. Another trend is the convergence of AI and 5G IoT, enabling predictive maintenance and real‑time decision making. Finally, the adoption of 5G NR Standalone architecture is accelerating, offering dedicated slices for IoT traffic and improving network efficiency.

4. COVID‑19 Impact on the Europe 5G in IoT Market – Pandemic effects and recovery trajectory?

The pandemic initially slowed physical network roll‑outs due to lockdowns and supply‑chain disruptions. However, remote work, tele‑health, and increased demand for contactless logistics accelerated interest in robust 5G IoT solutions. By 2022, recovery was evident as governments prioritized digital resilience, leading to renewed investment in 5G infrastructure. The market’s resilience is reflected in the strong forecast growth, indicating a post‑COVID bounce‑back that is fueling accelerated deployments across key verticals.

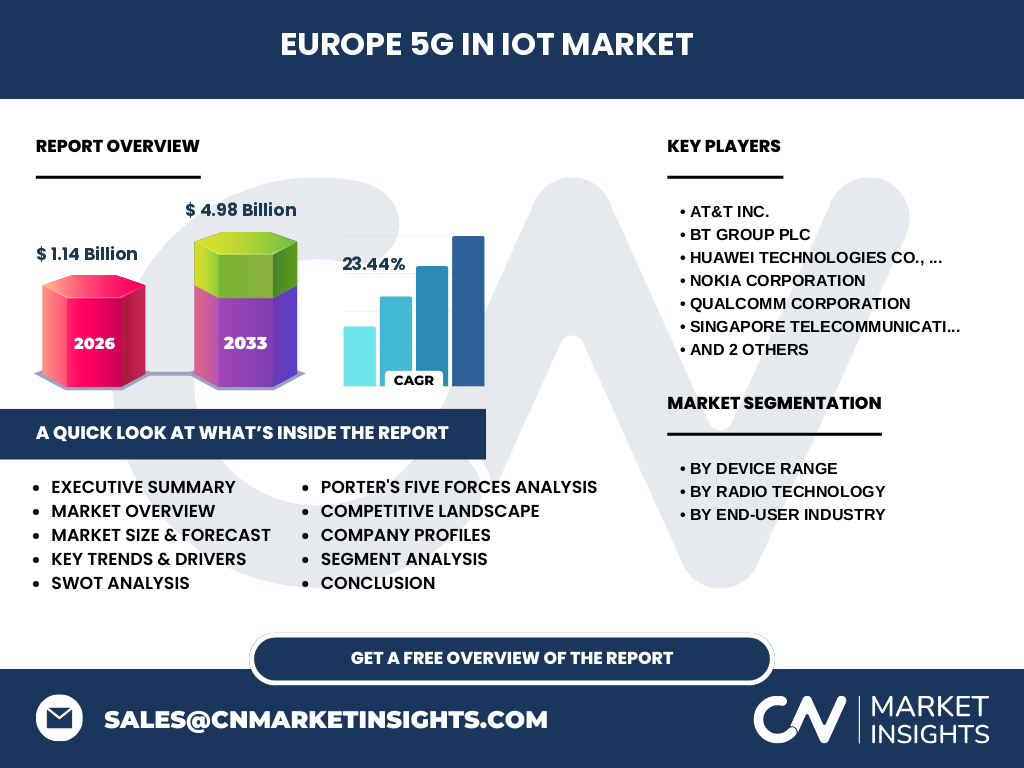

5. Europe 5G in IoT Market Competitive Landscape – Major competitors and market consolidation?

The competitive arena includes global telecom equipment leaders and network operators such as AT&T Inc., BT Group Plc, Huawei Technologies Co., Ltd, Nokia Corporation, Qualcomm Corporation, Singapore Telecommunications Limited (Singtel), Telef, and Telefonaktiebolaget LM Ericsson. These players compete on infrastructure solutions, device integration, and end‑to‑end services. Recent consolidation activities involve strategic partnerships and joint ventures to co‑develop private 5G networks, highlighting a trend toward collaborative ecosystems rather than pure acquisition‑driven consolidation.

6. Executive Summary – High‑level overview and key findings about Europe 5G in IoT Market?

The Europe 5G in IoT market is projected to expand from a 2026 valuation of €1.14 billion to €4.98 billion by 2033, reflecting a robust 23.44% CAGR. Growth is propelled by strong policy support, rising demand for smart manufacturing, and the emergence of private 5G networks. While investment costs and regulatory fragmentation pose challenges, opportunities in AI‑enabled IoT, edge computing, and cross‑industry collaborations promise sustained momentum. Leading vendors are intensifying partnerships to capture share in this high‑growth segment.

7. Europe 5G in IoT Market Forecast – Projections for 2025‑2032 period?

Based on the provided data, the market is expected to maintain its 23.44% compound annual growth rate throughout the forecast horizon. Starting from the 2026 base of €1.14 billion, the market will reach approximately €4.98 billion by the end of 2033. This trajectory suggests a steady increase each year, with demand accelerating as more verticals adopt private 5G solutions and as the ecosystem matures.

8. Europe 5G in IoT Market Size and Share by Segmentation – Breakdown by device range, radio technology, and end‑user industry?

Segmentation is organized into three primary dimensions. By device range, the market is divided between Short‑Range IoT Devices—typically used for indoor asset tracking and industrial sensor networks—and Wide‑Range IoT Devices that support broader coverage such as smart city deployments. By radio technology, the split is between 5G NR Standalone Architecture, offering dedicated IoT slices, and 5G NR Non‑Standalone Architecture, which leverages existing LTE cores. End‑user industry segmentation includes Manufacturing, Energy & Utilities, Government, Healthcare, Transportation & Logistics, and Mining, each leveraging 5G IoT for specific operational enhancements.

9. Global Europe 5G in IoT Market Size and Share by Region – Geographic distribution?

While the focus is on Europe, the market’s global context positions Europe as a leading adopter of 5G‑enabled IoT, driven by mature regulatory frameworks and strong industrial bases. The European share contributes significantly to the overall global 5G IoT landscape, reflecting its role as a testbed for advanced private‑network deployments and cross‑border interoperability initiatives.

10. Regional Analysis of the Europe 5G in IoT Market – Detailed regional market performance?

Within Europe, Northern and Western regions such as Germany, the United Kingdom, Sweden, and the Netherlands exhibit the highest adoption rates due to advanced manufacturing clusters and supportive government incentives. Southern and Eastern markets are accelerating, benefitting from EU funding programs aimed at digital infrastructure upgrades. Regional performance varies by vertical, with manufacturing dominance in Germany and logistics growth in the Benelux corridor.

11. Leading Company Profiles in the Europe 5G in IoT Market – Industry players and strategies?

Key players include AT&T Inc., BT Group Plc, Huawei Technologies, Nokia, Qualcomm, Singtel, Telef, and Ericsson. Their strategies focus on offering end‑to‑end 5G IoT solutions, developing private network platforms, investing in R&D for low‑power wide‑area devices, and forming ecosystem partnerships with cloud providers and system integrators. Many are targeting vertical‑specific bundles, such as Nokia’s Industry Cloud for manufacturing or Qualcomm’s chipset solutions for wide‑range IoT devices.

12. Porter’s Five Forces Analysis of the Europe 5G in IoT Market – Competitive forces assessment?

Threat of New Entrants: Moderate, due to high capital requirements and spectrum regulation. Bargaining Power of Suppliers: Concentrated, as key chipsets and radio components are supplied by a few manufacturers. Bargaining Power of Buyers: Increasing, as enterprises demand customized private‑network solutions. Threat of Substitutes: Low, because 5G offers unique latency and capacity advantages over legacy LPWAN or LTE IoT. Industry Rivalry: High, driven by aggressive innovation and partnership formation among the leading vendors.

13. SWOT Analysis of the Europe 5G in IoT Market – Strengths, weaknesses, opportunities, threats?

Strengths: Strong policy support, mature industrial base, advanced telecom infrastructure. Weaknesses: High deployment costs, fragmented spectrum allocation. Opportunities: Private 5G networks, AI‑driven IoT analytics, cross‑border smart logistics, sustainability‑focused IoT solutions. Threats: Cybersecurity risks, regulatory delays, potential supply‑chain constraints for critical components.

14. Europe 5G in IoT Market Value Chain Analysis – Industry structure and value flow?

The value chain starts with component manufacturers (chipsets, RF modules), followed by device assemblers producing short‑range and wide‑range IoT hardware. Network operators and infrastructure providers then deploy 5G NR Standalone or Non‑Standalone architectures. System integrators add middleware and edge‑computing platforms, while vertical solution providers deliver industry‑specific applications. End users—manufacturers, utilities, governments, healthcare providers, logistics firms, and mining companies—consume the final integrated service.

15. Key Investment Insights in the Europe 5G in IoT Market – Strategic investment recommendations?

Investors should prioritize companies offering private 5G network platforms and those with strong IP in low‑power wide‑area IoT device design. Partnerships that combine telecom infrastructure with edge‑computing and AI analytics present high upside. Funding initiatives aligned with EU sustainability and digital‑transformation programmes can de‑risk capital exposure. Monitoring regulatory developments around spectrum allocation will help identify early‑stage opportunities.

16. Europe 5G in IoT Market Conclusion – Summary and key takeaways?

The Europe 5G in IoT market is on a rapid growth path, projected to reach €4.98 billion by 2033 with a 23.44% CAGR. Strong policy backing, demand from manufacturing and logistics, and the shift toward private 5G networks drive this expansion. While cost and regulatory hurdles exist, the ecosystem’s momentum, combined with the emergence of AI‑enabled IoT and edge solutions, creates a compelling landscape for stakeholders and investors.

17. Research Methodology – How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry experts, surveys of key enterprises, and secondary data collection from EU publications, vendor reports, and financial disclosures. Market sizing used the provided 2026 baseline of €1.14 billion and applied the disclosed 23.44% CAGR to forecast future values. Segmentation analysis leveraged the defined device, technology, and industry categories.

18. Research Scope – Coverage and limitations?

The scope covers the European region, focusing on 5G‑enabled IoT devices, network architectures, and end‑user verticals listed in the segmentation. It includes market size, growth forecast, competitive landscape, and strategic insights. The analysis does not extend to non‑European markets or detailed financial breakdowns beyond the supplied figures.

19. Key Companies and Recent Developments in the Europe 5G in IoT Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Leading firms have announced several notable initiatives. Nokia introduced a private‑network suite targeting manufacturing clusters in Germany. Ericsson partnered with a major European logistics provider to pilot 5G‑enabled autonomous warehouse robots. Qualcomm released next‑generation low‑power IoT chipsets optimized for 5G NR Standalone. Huawei expanded its 5G IoT portfolio with a focus on smart‑city deployments in Scandinavia. BT Group launched a managed private‑5G service for government agencies, while AT&T began offering cross‑border 5G IoT solutions for multinational enterprises operating in Europe. These developments underscore the rapid commercialization and collaborative momentum shaping the market.