1. What is the definition, scope, and significance of the E‑Commerce Automotive Aftermarket Market?

The E‑Commerce Automotive Aftermarket Market encompasses online platforms and digital channels that facilitate the sale, distribution, and servicing of automotive replacement parts, accessories, and related services post‑vehicle sale. Its scope includes a broad product portfolio—braking systems, steering & suspension components, hub assemblies, universal joints, gaskets, filters, spark plugs—and serves both B2B (repair shops, distributors) and B2C (individual vehicle owners) segments. Significance stems from the shift toward convenience‑driven purchasing, the ability to reach fragmented customer bases globally, and the potential to accelerate parts turnover, thereby supporting vehicle longevity, safety compliance, and aftermarket revenue streams.

2. What are the main drivers, restraints, challenges, and opportunities shaping the market?

Key drivers include rapid internet penetration, increasing vehicle age, and growing consumer preference for online price transparency and doorstep delivery. Digital logistics advancements and integration of AI‑powered recommendation engines also boost buying confidence. Restraints involve concerns over part authenticity, high return rates, and complex regulatory environments governing automotive safety standards. Challenges arise from fragmented supply chains, the need for robust warranty and reverse‑logistics infrastructure, and intense price competition. Opportunities are abundant in expanding omni‑channel strategies, leveraging data analytics for predictive inventory, and tapping emerging economies where vehicle parc growth fuels aftermarket demand.

3. Which growth trends are currently influencing the E‑Commerce Automotive Aftermarket Market?

Current trends feature the rise of subscription‑based parts kits, the adoption of augmented‑reality tools for part identification, and the proliferation of marketplace ecosystems that aggregate multiple sellers (e.g., Alibaba, Amazon, eBay). Sustainable part sourcing—re‑manufactured and recyclable components—is gaining traction, as are mobile‑first shopping experiences tailored to on‑the‑go technicians. Additionally, the integration of IoT data from connected vehicles enables just‑in‑time part ordering, reducing inventory holding costs.

4. How has COVID‑19 impacted the market, and what is the recovery trajectory?

The pandemic accelerated digital adoption as lockdowns limited brick‑and‑mortem access to parts stores. Online transactional volumes surged, especially in B2C channels where DIY repairs rose due to reduced travel. Supply‑chain disruptions highlighted the need for resilient e‑commerce networks, prompting many retailers to localize inventory hubs. Recovery is strong; post‑pandemic consumer confidence and continued remote work have cemented e‑commerce as the preferred purchase route, sustaining the market’s upward momentum.

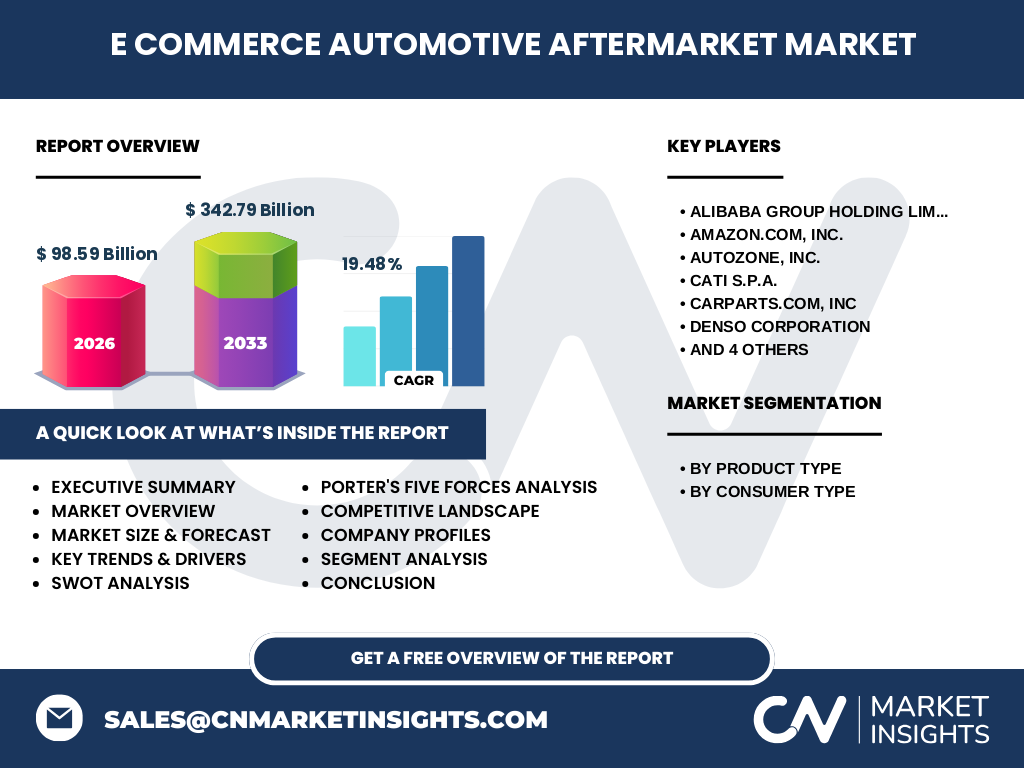

5. Who are the major competitors and what is the state of market consolidation?

Market leadership is dominated by global e‑commerce giants and specialized automotive retailers: Alibaba Group Holding Limited, Amazon.com, Inc., eBay Inc., and regional platforms such as Shopee. Traditional aftermarket distributors like AutoZone, Inc., LKQ Corporation, and Denso Corporation have invested heavily in digital channels to protect market share. Consolidation is moderate; strategic acquisitions—e.g., larger distributors acquiring niche parts marketplaces—aim to broaden product assortments and strengthen logistics capabilities, yet the sector remains relatively fragmented due to the sheer number of part SKUs.

6. What are the high‑level takeaways and key findings about the market?

The E‑Commerce Automotive Aftermarket Market is valued at $98.59 billion in 2026 and is projected to reach $342.79 billion by 2033, reflecting a robust CAGR of 19.48 %. Growth is underpinned by digital buying habits, expanding vehicle age, and a widening product mix that serves both B2B and B2C customers. Competitive dynamics feature a blend of pure‑play e‑commerce platforms and legacy distributors transitioning online. Key risks include part authentication and logistic complexities, while opportunities lie in data‑driven inventory, sustainability, and regional expansion.

7. What are the market forecasts for 2025‑2032?

Based on the stated CAGR of 19.48 %, the market is expected to maintain a high growth trajectory throughout 2025‑2032, moving from the 2026 baseline of $98.59 billion toward the 2033 forecast of $342.79 billion. This translates into consistent year‑over‑year expansion, driven by continued e‑commerce adoption, increasing vehicle parc size, and innovation in digital sales‑enablement tools.

8. How is the market sized and shared by product and consumer type segments?

Product‑type segmentation divides the market across braking, steering & suspension, hub assemblies, universal joints, gaskets, filters, and spark plugs. Each segment benefits from online‑driven demand for exact‑fit replacements and quick replenishment. Consumer‑type segmentation shows a dual‑track: B2B channels dominate volume sales for repair shops and fleet operators, while B2C channels capture the growing DIY segment, especially for routine maintenance items such as filters and spark plugs. Exact monetary shares are not disclosed, but the breadth of product categories underscores a diversified revenue base.

9. What is the geographical distribution of the global market?

The market exhibits a worldwide footprint, with major contributions from North America, Europe, Asia‑Pacific, and emerging regions in Latin America and the Middle East. E‑commerce infrastructure maturity and vehicle density drive higher market shares in North America and Asia‑Pacific, where leading platforms such as Amazon, Alibaba, and Shopee operate. European markets benefit from stringent safety regulations that encourage online sourcing of certified parts.

10. What does regional analysis reveal about market performance?

North America leads in transaction volume, leveraging well‑established logistics networks and a large B2B repair ecosystem. Asia‑Pacific shows the fastest growth rate, propelled by expanding middle‑class car ownership, mobile‑first commerce habits, and aggressive platform expansion by Alibaba and Shopee. Europe maintains steady growth, with a strong emphasis on compliance and premium aftermarket parts. Latin America and the Middle East present nascent but promising opportunities as internet penetration improves and local distributors digitize.

11. Which companies are leading the market and what strategies are they pursuing?

Alibaba Group Holding Limited leverages its massive marketplace ecosystem and cross‑border logistics to capture both B2B and B2C demand. Amazon.com, Inc. focuses on Prime delivery speed and AI‑driven part recommendations. AutoZone, Inc. and LKQ Corporation invest in proprietary online portals and integrated inventory management for repair shops. Denso Corporation emphasizes OEM‑grade part authenticity through digital verification. eBay Inc. continues to grow its specialized automotive classifieds, while Shopee expands its presence in Southeast Asia with localized payment solutions. Strategic moves include acquisitions of niche parts retailers, partnerships with logistics providers, and the launch of subscription kits.

12. How do Porter’s Five Forces affect the market?

• Threat of New Entrants – Moderate; low entry barriers for niche marketplaces but high capital requirements for logistics and OEM partnerships deter many. • Bargaining Power of Suppliers – Moderate; manufacturers control part quality, yet the breadth of suppliers dilutes individual power. • Bargaining Power of Buyers – High; price transparency and alternative platforms increase buyer leverage. • Threat of Substitutes – Low; specific automotive parts have limited substitutes, though remanufactured options compete on price. • Industry Rivalry – Intense; numerous players vie on price, delivery speed, and part authenticity, driving continual innovation.

13. What are the SWOT highlights for the market?

Strengths: Strong growth momentum, broad product portfolio, global digital reach.

Weaknesses: Complex verification of part authenticity, high logistics cost for bulky items.

Opportunities: Expansion into emerging economies, AI‑enabled inventory, sustainable remanufactured parts.

Threats: Counterfeit part proliferation, regulatory changes, heightened price competition.

14. What does the value chain of the market look like?

Value chain stages include: part manufacturers → wholesale distributors → digital marketplace platforms (e.g., Alibaba, Amazon) → last‑mile logistics providers → end customers (repair shops or vehicle owners). Supporting services such as warranty management, AI‑driven fitment tools, and reverse logistics for returns add value and differentiate platform offerings.

15. What investment insights can be drawn for stakeholders?

Investors should prioritize companies with strong logistics networks, proven authentication mechanisms, and data analytics capabilities. Funding digital transformation initiatives of traditional distributors offers upside as they migrate online. High‑growth regions, particularly Asia‑Pacific, present attractive entry points. Sustainability‑focused remanufactured parts and subscription‑based models are emerging sub‑segments worth monitoring for early‑stage venture opportunities.

16. What are the concluding takeaways from the research?

The E‑Commerce Automotive Aftermarket Market is on a decisive growth path, driven by digital adoption, an aging vehicle fleet, and expanding product offerings. With a projected market size of $342.79 billion by 2033 and a 19.48 % CAGR, the sector promises substantial revenue potential. Success hinges on mastering part authenticity, optimizing logistics, and capitalizing on regional expansion, especially in fast‑growing Asia‑Pacific economies.

17. How was the research conducted?

The study combined primary interviews with industry experts, secondary data from company reports, market databases, and trade publications. Trend analysis employed historical sales data, while forward‑looking forecasts applied the disclosed CAGR of 19.48 % to extrapolate future market size. Competitive profiling integrated financial statements and strategic announcements of the key companies listed.

18. What is the scope of the research and its limitations?

The scope covers global online automotive parts sales, segmented by product type and consumer type, and includes major geographic regions. Limitations arise from the unavailability of granular regional revenue figures; therefore, analysis relies on qualitative assessment and known macro trends. Proprietary company data beyond public disclosures were not incorporated.

19. Which key companies have announced recent developments and what are they?

Alibaba Group Holding Limited expanded its cross‑border logistics hub in Southeast Asia, reducing delivery times for automotive parts. Amazon.com, Inc. launched an AI‑driven “Fit‑Finder” tool that improves part matching accuracy. AutoZone, Inc. introduced a B2B subscription service for routine filter and spark‑plug deliveries. CATI S.p.A. announced a partnership with e‑logistics provider to enhance reverse‑logistics for warranty returns. CarParts.com, Inc. rolled out a mobile app featuring augmented‑reality part visualization. Denso Corporation released a line of certified remanufactured filters, emphasizing sustainability. LKQ Corporation completed the acquisition of a regional e‑commerce marketplace, broadening its B2C footprint. Shopee intensified its automotive category with localized payment solutions and faster courier agreements. The Pep Boys opened its first fully digital retail outlet, integrating in‑store pickup with online ordering. eBay Inc. updated its platform to include blockchain‑based part provenance tracking, addressing counterfeit concerns.