1. North America Data Center Cooling Market Overview - Definition, scope, and significance?

The North America Data Center Cooling Market encompasses all technologies, solutions, and services used to manage thermal loads in data centers across the United States, Canada, and Mexico. It includes room‑based, row‑based, and rack‑based cooling systems, serving enterprise, colocation, wholesale, and hyperscale facilities. Efficient cooling is critical for maintaining equipment reliability, minimizing downtime, and supporting the exponential growth of digital workloads, making it a cornerstone of the region’s ICT infrastructure.

2. North America Data Center Cooling Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the surge in cloud adoption, high‑performance computing, and AI workloads that elevate power densities, thereby increasing cooling demand. Strong capital investment in hyperscale and enterprise data centers further fuels growth. Restraints stem from high upfront CAPEX for advanced cooling solutions and stringent regulatory standards on energy consumption. Challenges involve managing heat in legacy facilities and balancing cooling efficiency with sustainability goals. Opportunities arise from emerging liquid‑cooling technologies, AI‑driven cooling management, and renewable‑energy‑aligned cooling designs.

3. North America Data Center Cooling Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a shift from traditional CRAC units to modular, high‑efficiency IAQ systems and the adoption of liquid‑direct cooling for high‑density racks. Edge data center proliferation is prompting compact, micro‑cooling solutions. Sustainable practices are driving the integration of free‑cooling, heat‑reuse, and renewable‑energy‑powered chillers. Moreover, AI‑based predictive analytics for dynamic temperature control is rapidly gaining traction among leading operators.

4. COVID-19 Impact on the North America Data Center Cooling Market - Pandemic effects and recovery trajectory?

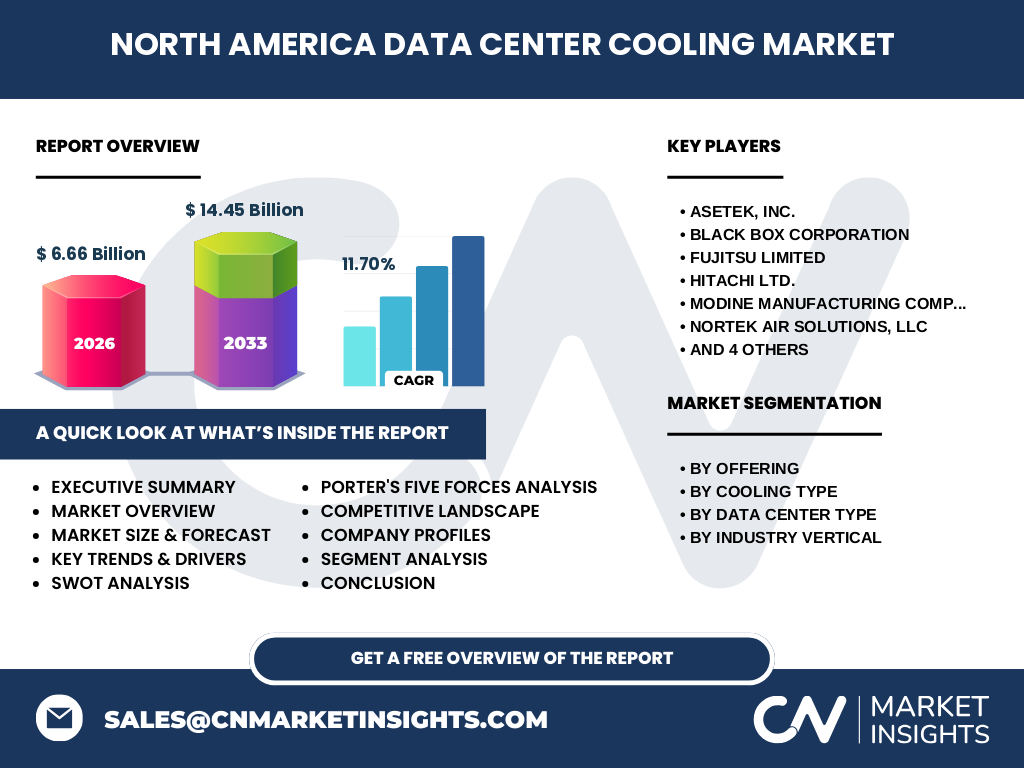

The pandemic accelerated digital transformation as remote work, e‑learning, and telehealth increased data traffic. This surge amplified cooling requirements, prompting short‑term capacity expansions. Although supply‑chain disruptions delayed some equipment deliveries, the market demonstrated resilience, with a swift rebound in 2021. The recovery trajectory remains robust, underpinned by sustained demand for cloud services and a projected CAGR of 11.70% through 2033.

5. North America Data Center Cooling Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena is led by diversified technology firms such as Schneider Electric, United Technologies (Carrier), and STULZ, alongside specialist providers like Asetek and Modine. Recent consolidation includes strategic acquisitions aimed at strengthening liquid‑cooling portfolios and expanding service capabilities. Partnerships between OEMs and system integrators are also common, enabling end‑to‑end cooling solutions that differentiate market leaders.

6. Executive Summary - High-level overview and key findings about North America Data Center Cooling Market?

The North America Data Center Cooling Market is valued at USD 6.66 billion in 2026 and is projected to reach USD 14.45 billion by 2033, delivering an 11.70% CAGR. Growth is driven by escalating data workloads, hyperscale expansion, and sustainability imperatives. Liquid‑cooling and AI‑enabled management are emerging as differentiators. Competitive dynamics feature strong incumbents, strategic M&A, and collaborative ecosystems that shape future market leadership.

7. North America Data Center Cooling Market Forecast - Projections for 2025‑2032 period?

While the exact 2025 baseline is not disclosed, the market is expected to maintain double‑digit growth through 2032, aligning with the overall 11.70% CAGR. Demand will be led by hyperscale facilities, followed by enterprise and colocation segments. Cooling‑type mix will shift toward row‑based and rack‑based solutions as data center density rises, while room‑based cooling will retain relevance in legacy and low‑density sites.

8. North America Data Center Cooling Market Size and Share by Segmentation - Breakdown by segment?

By Offering, the market is split between Solutions and Services, reflecting a balance of hardware sales and recurring maintenance contracts. Cooling Type segmentation comprises Room‑Based, Row‑Based, and Rack‑Based cooling, each catering to different density levels. Data Center Type segmentation includes Enterprise, Colocation, Wholesale, and Hyperscale, with hyperscale expected to capture the fastest growth share. Industry Vertical segmentation spans BFSI, Manufacturing, IT & Telecom, Media & Entertainment, Retail, Government & Defense, Healthcare, and Energy, with IT & Telecom and BFSI leading adoption.

9. Global North America Data Center Cooling Market Size and Share by Region - Geographic distribution?

North America accounts for the dominant share of the global data center cooling landscape, driven by the United States’ extensive cloud infrastructure and Canada’s growing data center footprint. While specific regional percentages are not disclosed, the market’s USD 6.66 billion valuation in 2026 underscores its leadership position relative to Europe and Asia‑Pacific, which are expanding but remain smaller in absolute terms.

10. Regional Analysis of the North America Data Center Cooling Market - Detailed regional market performance?

The United States leads the market with the highest concentration of hyperscale and enterprise data centers, attracting major investments from tech giants. Canada shows steady growth, primarily in colocation and edge facilities, supported by favorable renewable energy policies. Mexico’s market is nascent but gaining momentum through foreign direct investment and the establishment of regional disaster‑recovery sites, which will bolster cooling demand.

11. Leading Company Profiles in the North America Data Center Cooling Market - Industry players and strategies?

Schneider Electric focuses on integrated energy management platforms, leveraging its EcoStruxure architecture for intelligent cooling. United Technologies (Carrier) emphasizes high‑efficiency chillers and free‑cooling technologies. STULZ provides modular, AI‑enabled cooling units tailored for hyperscale clients. Asetek specializes in liquid‑cooling solutions for high‑performance racks. Fujitsu and Hitachi deliver comprehensive HVAC packages, while Modine and Nortek Air Solutions supply specialty air‑handling equipment. Each company pursues R&D, strategic alliances, and geographic expansion to capture market share.

12. Porter's Five Forces Analysis of the North America Data Center Cooling Market - Competitive forces assessment?

• Threat of New Entrants: Moderate – high capital requirements and technical expertise create barriers, though niche liquid‑cooling startups can enter. • Bargaining Power of Suppliers: Low to moderate – component suppliers are diversified, but specialized refrigerants and high‑efficiency compressors can command premium pricing. • Bargaining Power of Buyers: Increasing – large cloud operators negotiate volume discounts and demand customized, energy‑efficient solutions. • Threat of Substitutes: Low – alternative cooling methods (e.g., natural ventilation) are limited by data center density. • Industry Rivalry: High – intense competition among established OEMs, driven by technology differentiation and service contracts.

13. SWOT Analysis of the North America Data Center Cooling Market - Strengths, weaknesses, opportunities, threats?

Strengths: Mature infrastructure, high capital availability, strong innovation ecosystem. Weaknesses: Elevated upfront costs for advanced cooling, legacy facility retrofits. Opportunities: Expansion of liquid‑cooling, AI‑driven thermal management, heat‑reuse for district heating. Threats: Regulatory pressure on energy usage, supply‑chain constraints for critical components, and potential market saturation in low‑density segments.

14. North America Data Center Cooling Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers (copper, refrigerants), progresses to component manufacturers (compressors, fans), then to system integrators that assemble cooling units. OEMs sell solutions and services to data center owners, who may engage third‑party service providers for installation, monitoring, and maintenance. End‑users generate feedback that drives R&D, completing the loop. Strategic partnerships at the integration and service layers enhance value capture.

15. Key Investment Insights in the North America Data Center Cooling Market - Strategic investment recommendations?

Investors should prioritize companies with strong IP in liquid‑cooling and AI‑enabled controls, as these technologies address density and sustainability challenges. Look for firms executing M&A to broaden service portfolios and for partnerships that unlock access to hyperscale customers. Funding R&D projects focused on heat‑recovery and renewable‑powered cooling can yield long‑term differentiated returns.

16. North America Data Center Cooling Market Conclusion - Summary and key takeaways?

The market is on a rapid growth trajectory, moving from USD 6.66 billion in 2026 to USD 14.45 billion by 2033. Drivers such as cloud expansion, high‑density workloads, and sustainability imperatives are compelling operators to adopt advanced cooling solutions. Competitive dynamics favor innovators in liquid‑cooling and AI‑based management, while strategic investments in these areas are likely to deliver superior returns.

17. Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with senior executives from leading cooling vendors, data center operators, and industry analysts, with secondary research from company filings, market reports, and regulatory databases. Quantitative data were validated through cross‑checking with third‑party financial sources, and forecasting employed compound annual growth rate (CAGR) modeling based on historical trends and projected demand drivers.

18. Research Scope - Coverage and limitations?

The scope covers the entire North American region, encompassing the United States, Canada, and Mexico, and examines all cooling types, offerings, data center categories, and industry verticals listed. Limitations include the exclusion of proprietary pricing data and the reliance on publicly available market estimates for the forecast horizon.

19. Key Companies and Recent Developments in the North America Data Center Cooling Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Schneider Electric announced an expanded EcoStruxure™ Power Monitoring suite tailored for hyperscale cooling efficiency. Carrier unveiled a next‑generation free‑cooling chiller with 30% lower energy consumption. STULZ launched modular AI‑powered coolant distribution units for row‑based deployments. Asetek introduced a new liquid‑to‑air heat exchanger targeting high‑density rack applications. Fujitsu and Hitachi jointly released a hybrid HVAC platform integrating renewable energy sources. Modine announced a partnership with a major colocation provider to retrofit legacy facilities with high‑efficiency air‑handling units. These developments illustrate a market focused on performance, sustainability, and strategic collaboration.