What is the Railway Cybersecurity Market Overview – Definition, scope, and significance?

The Railway Cybersecurity Market encompasses solutions, services, and technologies designed to protect rail transport systems from cyber threats. It covers both Operational Technology (OT) such as signaling and train control, and Information Technology (IT) including passenger information and ticketing platforms. The market’s significance stems from the growing digitization of rail networks, the critical safety implications of cyber‑attacks, and the need to safeguard high‑value data and uninterrupted service.

What are the Railway Cybersecurity Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising cyber‑crime sophistication, increased deployment of IoT sensors on trains, and stringent regulatory mandates for safety and data protection. Restraints involve high implementation costs and legacy systems that are difficult to integrate. Major challenges are talent shortages in cybersecurity and the complex, multi‑vendor environment of railway infrastructure. Opportunities arise from the expanding demand for managed security services, AI‑based threat detection, and cross‑border standardization initiatives.

What are the current Railway Cybersecurity Market Growth Trends?

Emerging trends feature a shift toward unified OT‑IT security platforms, the adoption of cloud‑native security services, and greater reliance on endpoint protection for on‑board devices. Vendors are increasingly offering bundled solution‑service packages, while rail operators are piloting AI‑driven anomaly detection to anticipate attacks before they disrupt operations. The market also sees a rise in collaborative standards such as IEC 62443 specific to rail.

How has COVID‑19 impacted the Railway Cybersecurity Market and what is the recovery trajectory?

The pandemic accelerated digital transformation as operators sought remote monitoring and contact‑less ticketing, creating new attack surfaces. While short‑term budget constraints slowed some projects, overall spending rebounded quickly. Post‑COVID, rail agencies have prioritized resilient cyber frameworks, leading to a robust recovery and positioning the market for sustained growth through 2032.

Who are the major competitors in the Railway Cybersecurity Market and what is the level of market consolidation?

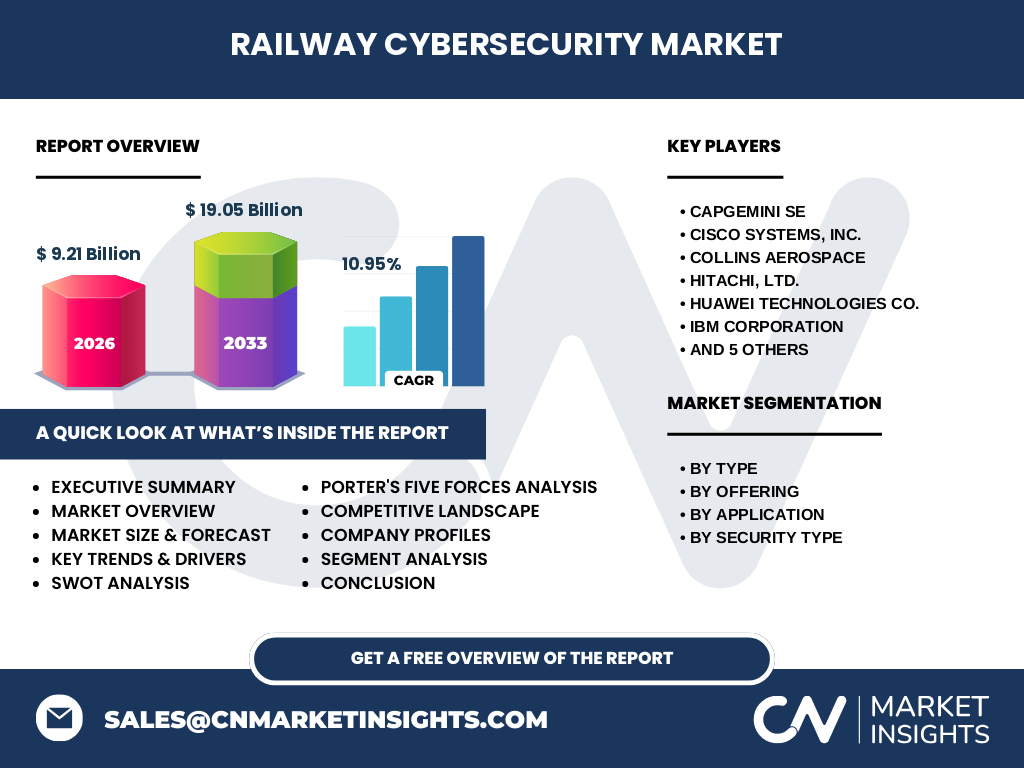

Leading players include CAPGEMINI SE, Cisco Systems, Collins Aerospace, Hitachi Ltd., Huawei Technologies, IBM Corporation, Nokia Corporation, Selectron Systems AG, Siemens AG, and Thales Group. The market displays moderate consolidation, with several multinational technology firms expanding their rail‑focused cyber portfolios through acquisitions and strategic partnerships, thereby intensifying competitive dynamics.

What are the key findings in the Executive Summary of the Railway Cybersecurity Market?

The market is projected to grow from a 2026 valuation of US$9.21 billion to US$19.05 billion by 2033, reflecting a 10.95 % CAGR. Growth is powered by digitalization, regulatory pressure, and the emergence of integrated OT‑IT security solutions. North America and Europe lead adoption, while Asia‑Pacific shows rapid uptake driven by new high‑speed rail projects. Service revenue is rising faster than pure solution sales, highlighting a shift toward managed security.

What is the Railway Cybersecurity Market forecast for 2025‑2032?

Based on the provided CAGR of 10.95 %, the market is expected to maintain double‑digit expansion throughout the forecast horizon. By 2032, annual revenues are anticipated to approach the upper half of the 2027‑2033 forecast range, driven by continued investment in AI‑enabled threat intelligence, lifecycle management of legacy assets, and increased spend on endpoint and network security for passenger and freight operations.

How is the Railway Cybersecurity Market sized and shared by segmentation?

Segmentation by Type splits the market between Operational Technology and Information Technology, each receiving a substantial portion as rail systems depend equally on control and data layers. Offering segmentation differentiates Solution from Services, with Services gaining a higher growth rate due to recurring revenue models. Application segmentation covers Passenger Trains and Freight Trains, both critical but with Passenger Trains typically attracting more security spend because of safety and customer‑experience concerns. Security Type segmentation includes Application Security, Network Security, Data Protection, Endpoint Security, and System Administration, reflecting a comprehensive defense strategy.

What is the global Railway Cybersecurity Market size and share by region?

The market’s global footprint is anchored by North America and Europe, which together account for the majority of the 2026 US$9.21 billion valuation. Asia‑Pacific is emerging as a fast‑growing region, driven by large rail infrastructure projects and increasing cyber awareness. While specific regional monetary shares are not disclosed, the geographic distribution underscores a strong presence in developed markets with expanding opportunities in emerging economies.

What are the key findings of the Regional Analysis of the Railway Cybersecurity Market?

In North America, operators prioritize compliance with stringent safety standards, fostering early adoption of advanced network and endpoint security. Europe benefits from EU‑wide regulatory frameworks, leading to harmonized security solutions across borders. Asia‑Pacific’s rapid rail expansion creates a demand surge for scalable, cost‑effective security offerings, often supplied by regional vendors in partnership with global players. Latin America and the Middle East show modest yet steady growth as modernization initiatives take hold.

What are the leading company profiles and their strategies in the Railway Cybersecurity Market?

CAPGEMINI SE focuses on consulting‑driven managed services, leveraging its global delivery network. Cisco Systems capitalizes on its networking heritage to provide integrated firewall and intrusion‑prevention systems tailored for rail OT. Collins Aerospace offers niche aerospace‑grade security for signaling equipment. Hitachi Ltd. integrates cybersecurity into its rail automation platforms. Huawei and Nokia supply communication‑centric security for rail IoT. IBM provides AI‑powered threat analytics, while Siemens and Thales combine system integration expertise with cybersecurity modules. Selectron Systems AG specializes in hardware‑rooted security for critical rail components.

How does Porter’s Five Forces analysis apply to the Railway Cybersecurity Market?

Threat of new entrants is moderate due to high technical barriers and the need for domain expertise. Bargaining power of buyers is increasing as rail operators consolidate purchasing and demand integrated solutions. Supplier power is moderate; key hardware and software components are sourced from a limited set of technology firms. The threat of substitutes is low because rail safety cannot be compromised by generic IT security products. Rivalry among existing firms is intense, driven by innovation, service contracts, and strategic partnerships.

What are the SWOT insights for the Railway Cybersecurity Market?

Strengths: Critical safety relevance, high spending propensity, and strong regulatory push.

Weaknesses: Legacy system incompatibility and skilled‑personnel shortage.

Opportunities: AI‑driven detection, managed security services, and standards harmonization.

Threats: Sophisticated ransomware attacks targeting rail operations and geopolitical supply‑chain risks.

What does the Railway Cybersecurity Market value chain look like?

The value chain begins with research & development of security hardware and software, followed by system integration and validation specific to rail environments. Next comes deployment and configuration on OT/IT assets, then ongoing managed services, monitoring, and incident response. Finally, end‑users—rail operators and infrastructure owners—receive continuous compliance reporting and system upgrades, completing the loop.

What key investment insights can be drawn from the Railway Cybersecurity Market?

Investors should target companies offering integrated OT‑IT platforms and those with recurring‑revenue service models, as these provide stable cash flows. Partnerships that combine telecom expertise with rail‑specific security (e.g., Huawei with Siemens) present strategic upside. Funding for AI‑based threat intelligence and endpoint protection for rolling stock is likely to yield high returns given the projected market growth.

What conclusions can be drawn about the Railway Cybersecurity Market?

The market is on a decisive upward trajectory, underpinned by digitization, regulatory imperatives, and heightened cyber risk awareness. With a projected CAGR of 10.95 % leading to a 2033 valuation of US$19.05 billion, the sector offers considerable opportunities for solution providers, service firms, and investors. Emphasis on managed services, AI analytics, and standardized security frameworks will shape the competitive landscape.

How was the research methodology designed for this Railway Cyberseconds Market report?

The study employed a mixed‑methods approach, combining primary interviews with industry executives, secondary data from reputable databases, and quantitative modeling based on the provided market size and CAGR. Forecasts were derived using compounded annual growth calculations, while segmentation analysis relied on qualitative assessments of product and application categories.

What is the scope of the Railway Cybersecurity Market research?

The scope covers global market size, segmentation by type, offering, application, and security category, as well as regional distribution and competitive profiling of the listed key companies. It excludes detailed financial ratios, proprietary market share percentages, and any data beyond the supplied figures, focusing instead on strategic insights and growth dynamics.

Which key companies and recent developments are shaping the Railway Cybersecurity Market?

CAPGEMINI SE announced a global rail cybersecurity consulting practice expansion in 2024. Cisco launched a rail‑specific secure networking suite that integrates with existing OT protocols. Hitachi introduced a next‑generation secure train control system, while Siemens partnered with a cloud security provider to deliver scalable monitoring for high‑speed rail corridors. Thales unveiled a unified threat‑intelligence platform for passenger and freight networks, and Huawei released AI‑enabled intrusion detection for rail IoT devices.