1. North America Biodegradable Plastic Market Overview - Definition, scope, and significance?

The North America biodegradable plastic market encompasses all polymeric materials that can decompose naturally by microbial activity, returning to carbon dioxide, water, and biomass under defined conditions. The scope includes production, processing, and end‑use applications of biodegradable polymers such as polyhydroxyalkanoates (PHA), polylactic acid (PLA), starch blends, and biodegradable polyesters. This market is significant because it addresses mounting environmental concerns related to conventional petroleum‑based plastics, aligns with stringent regulatory frameworks on waste reduction, and meets growing consumer demand for sustainable packaging and products across various industries.

2. North America Biodegradable Plastic Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include heightened environmental awareness, supportive government policies (e.g., bans on single‑use plastics), and corporate sustainability commitments that push manufacturers toward biodegradable alternatives. The market also benefits from technological advances that improve material performance and cost competitiveness. Primary restraints are the higher price point of biodegradable polymers compared with traditional plastics and limited infrastructure for industrial composting. Challenges involve ensuring consistent biodegradability across diverse climate conditions and meeting stringent food‑contact safety standards. Opportunities arise from expanding applications in agriculture (mulch films), consumer goods, and emerging sectors like textile fibers, as well as from strategic partnerships that can accelerate scale‑up and lower production costs.

3. North America Biodegradable Plastic Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a steady shift from conventional plastics to PLA and starch‑based blends in food packaging, driven by retailer commitments to zero‑waste packaging. Emerging trends include the rise of PHA as a high‑performance biodegradable polymer for medical and food‑service applications, and the integration of biodegradable polymers into circular economy models through take‑back and composting programs. Additionally, there is an increasing focus on hybrid materials that combine biodegradable polymers with nano‑reinforcements to enhance barrier properties while maintaining compostability.

4. COVID-19 Impact on the North America Biodegradable Plastic Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic temporarily disrupted supply chains, causing short‑term shortages of feedstock for biodegradable polymers. However, heightened use of single‑use packaging for safety heightened awareness of plastic waste, prompting many brands to adopt biodegradable alternatives post‑pandemic. Recovery has been robust, with demand rebounding in 2022 and accelerating as companies integrate sustainability into their brand strategies, contributing to a strong trajectory toward the projected market size of $4.60 billion by 2033.

5. North America Biodegradable Plastic Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape features a mix of multinational chemical companies and specialized bioplastic firms. Key players such as BASF S.E., NatureWorks LLC., and Total Corbion PLA dominate the PLA segment, while companies like Novamont S.p.A. and Green Dot Bioplastics focus on starch blends and PHA. Recent consolidation includes strategic acquisitions to expand product portfolios and geographic reach, exemplified by larger firms acquiring niche technology startups to accelerate entry into high‑growth segments like agricultural films.

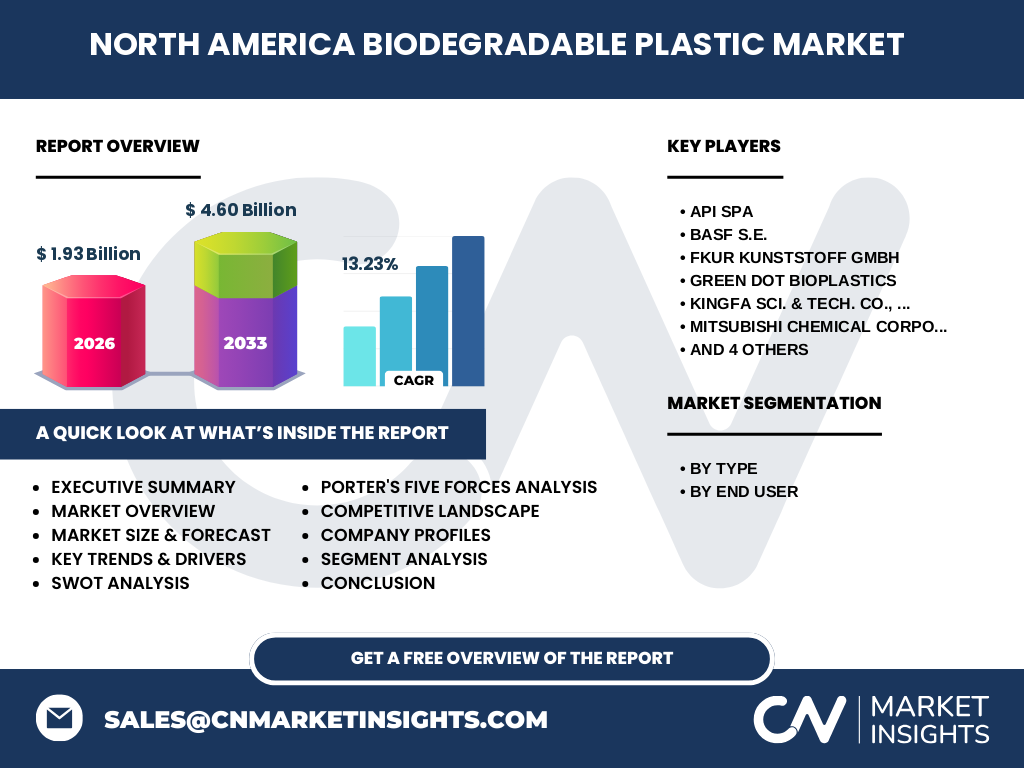

6. Executive Summary - High-level overview and key findings about North America Biodegradable Plastic Market?

The North America biodegradable plastic market was valued at $1.93 billion in 2026 and is projected to reach $4.60 billion by 2033, expanding at a robust 13.23 % CAGR. Growth is propelled by regulatory pressure, consumer demand for sustainable packaging, and technical improvements in polymer performance. While cost and composting infrastructure remain hurdles, expanding end‑use applications and strategic collaborations offer substantial upside. The market is fragmented, with several leading firms leveraging innovation and acquisitions to strengthen their positions.

7. North America Biodegradable Plastic Market Forecast - Projections for 2025‑2032 period?

Based on the provided CAGR of 13.23 %, the market is expected to maintain a strong upward trajectory from 2025 through 2032. By 2027, the market value will approach $2.9 billion, crossing the $4 billion mark by 2030, and reaching the forecasted $4.60 billion by 2033. This growth underscores sustained adoption across packaging, agriculture, consumer goods, and textile sectors, supported by ongoing policy initiatives and corporate sustainability targets.

8. North America Biodegradable Plastic Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by type includes PHA, PLA, starch blends, and biodegradable polyesters. PLA currently commands the largest share due to its established supply chain and suitability for food‑contact packaging. Starch blends capture a strong position in low‑cost applications such as agricultural films. PHA, while still a smaller share, is rapidly gaining traction for its superior barrier and tensile properties. Biodegradable polyesters hold niche roles in specialty applications like medical devices. End‑user segmentation shows packaging and bags as the dominant category, followed by agriculture and horticulture, consumer goods, and textile applications.

9. Global North America Biodegradable Plastic Market Size and Share by Region - Geographic distribution?

Within North America, the United States accounts for the majority of market activity, driven by its large consumer base, extensive packaging industry, and progressive waste‑management policies. Canada contributes a smaller yet growing share, particularly in the agricultural sector where biodegradable mulch films are gaining acceptance. The overall regional distribution reflects higher adoption rates in the U.S., with emerging opportunities in Canadian provinces that have enacted plastic‑reduction legislation.

10. Regional Analysis of the North America Biodegradable Plastic Market - Detailed regional market performance?

The United States exhibits strong performance across all segments, with notable growth in PLA packaging for fresh produce and PHA applications in medical disposables. The West Coast leads in regulatory adoption, influencing early market penetration of compostable products. The Midwest shows robust demand in agriculture for starch‑based mulch, while the Southeast is emerging in consumer‑goods applications due to expanding retail partnerships. Canada’s market is driven by provincial bans on single‑use plastics and supportive funding for composting infrastructure, positioning it for accelerated growth in the next five years.

11. Leading Company Profiles in the North America Biodegradable Plastic Market - Industry players and strategies?

Key companies include:

• API SpA – focuses on PHA production with an emphasis on high‑purity grades for medical use.

• BASF S.E. – leverages its global R&D network to develop cost‑effective PLA blends for packaging.

• FKuR Kunststoff GmbH – specializes in biodegradable polyesters targeting automotive interior parts.

• Green Dot Bioplastics – provides starch‑based solutions for agricultural films and low‑cost packaging.

• Kingfa Sci. & Tech. Co., Ltd. – expands its North American presence through joint ventures for PLA manufacturing.

• Mitsubishi Chemical Corporation – integrates biodegradable polymers into its existing petrochemical portfolio to offer hybrid solutions.

• NatureWorks LLC. – the leading PLA producer, emphasizing renewable sourcing and large‑scale capacity.

• Novamont S.p.A. – pioneers in starch‑blend technologies and collaborates with food retailers for compostable packaging.

• Plantic Technologies Limited – develops specialty PHA grades for high‑performance applications.

• Total Corbion PLA – combines bio‑based feedstock with advanced polymerization to deliver low‑carbon PLA for flexible packaging.

12. Porter's Five Forces Analysis of the North America Biodegradable Plastic Market - Competitive forces assessment?

• Threat of new entrants: Moderate – high capital requirements and technology barriers limit newcomers, but niche bioplastic startups can enter through strategic partnerships.

• Bargaining power of suppliers: Low to moderate – feedstock (e.g., corn, sugarcane) is abundant, though price volatility can affect margins.

• Bargaining power of buyers: High – large retailers and food manufacturers demand cost‑effective, certified compostable solutions, pressuring suppliers to lower prices.

• Threat of substitutes: Moderate – conventional plastics remain cheaper, while emerging recycling technologies could compete with biodegradability claims.

• Rivalry among existing competitors: High – intense competition on product performance, price, and sustainability credentials drives continuous innovation and occasional consolidation.

13. SWOT Analysis of the North America Biodegradable Plastic Market - Strengths, weaknesses, opportunities, threats?

Strengths: Strong regulatory support, growing consumer demand for eco‑friendly packaging, and a diversified product portfolio across polymer types.

Weaknesses: Higher production costs, limited composting infrastructure, and variability in biodegradation performance under different conditions.

Opportunities: Expansion into high‑value end‑uses such as medical devices and textile fibers, development of cost‑competitive PHA, and partnerships with waste‑management firms to close the composting loop.

Threats: Potential policy shifts favoring recycling over composting, price competition from low‑cost petrochemical plastics, and the risk of green‑washing allegations if certifications are not rigorously maintained.

14. North America Biodegradable Plastic Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material sourcing (e.g., renewable sugars, bio‑based monomers), progresses to polymer synthesis (fermentation for PHA, polymerization for PLA), followed by compounding and formulation to tailor material properties. Downstream steps include extrusion, injection molding, and film blowing for packaging, as well as conversion into agricultural films or textile fibers. Distribution channels comprise direct sales to large OEMs, partnerships with packaging converters, and supply agreements with agricultural equipment manufacturers. End‑of‑life management involves industrial composting facilities and, increasingly, municipal organic waste programs that feed back into the renewable feedstock cycle.

15. Key Investment Insights in the North America Biodegradable Plastic Market - Strategic investment recommendations?

Investors should prioritize companies with scalable PLA and PHA production capacity, robust R&D pipelines, and established partnerships with major end‑users. Allocation toward firms advancing cost‑reduction technologies—such as bio‑catalytic processes or waste‑derived feedstock—offers upside as price parity with conventional plastics approaches. Additionally, funding projects that develop composting infrastructure can create synergistic value, enhancing demand for biodegradable polymers while meeting regulatory targets.

16. North America Biodegradable Plastic Market Conclusion - Summary and key takeaways?

The North America biodegradable plastic market is on a rapid growth path, propelled by sustainability mandates, consumer preferences, and continuous material innovation. With a projected CAGR of 13.23 % and a market size of $4.60 billion by 2033, the sector presents compelling opportunities despite cost and infrastructure challenges. Success will depend on strategic collaborations, technology advancements, and alignment with evolving waste‑management policies.

17. Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data collection from company reports, regulatory filings, and reputable market databases. Quantitative analysis utilized historical market figures and the provided CAGR to model forward projections. Qualitative insights were derived from trend observation, competitive benchmarking, and stakeholder feedback to ensure a holistic view of market dynamics.

18. Research Scope - Coverage and limitations?

The scope encompasses the biodegradable plastic market in North America, covering polymer types (PHA, PLA, starch blends, biodegradable polyesters) and end‑use sectors (packaging, agriculture, consumer goods, textile). The analysis focuses on market size, growth drivers, competitive landscape, and forecast through 2033. Limitations include reliance on publicly available financial data and the exclusion of proprietary pricing or margin information not disclosed in the source material.

19. Key Companies and Recent Developments in the North America Biodegradable Plastic Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include:

• NatureWorks LLC. announced a new high‑clarity PLA grade aimed at fresh‑food packaging, coupled with a partnership with a major U.S. grocery chain to pilot compostable containers.

• Total Corbion PLA launched a low‑carbon PLA film for flexible snack packaging, supported by a joint venture with a North American converters network.

• Green Dot Bioplastics entered a strategic alliance with a leading agricultural equipment manufacturer to supply starch‑based mulch films for the Midwest market.

• API SpA secured a funding round to expand its PHA production facility in the United States, targeting medical‑device manufacturers.

• Mitsubishi Chemical Corporation introduced a hybrid biodegradable polyester that blends bio‑based monomers with recycled PET, aiming to capture the automotive interior segment.

These initiatives reflect the broader industry trend of leveraging innovation and partnership to accelerate market penetration and address cost and performance challenges.