1. What is the Infertility Treatment Devices and Equipment Market, and why is it significant?

The Infertility Treatment Devices and Equipment Market comprises medical hardware and systems used to diagnose, assist, and treat reproductive disorders. It spans devices for fertility surgery, assisted reproductive technologies (ART), and artificial insemination, including sperm separation tools, ovum aspiration pumps, micromanipulators, incubators, and analysis systems. The market’s significance stems from rising global infertility rates, increased awareness of reproductive health, and technological advances that improve success rates of procedures such as in‑vitro fertilization (IVF). These factors drive demand for sophisticated, reliable equipment, positioning the market as a critical component of modern reproductive medicine.

2. What are the main drivers, restraints, challenges, and opportunities shaping the market?

Key drivers include growing prevalence of infertility, higher disposable incomes in emerging economies, and supportive government policies that subsidize ART procedures. Technological innovation—particularly in miniaturized micro‑fluidic devices and AI‑enhanced imaging—creates opportunities for new product lines. Restraints involve high capital costs for advanced equipment and stringent regulatory approvals that can delay market entry. Challenges arise from limited skilled personnel in low‑resource regions and ethical debates around assisted reproduction. Opportunities exist in tele‑medicine integration, disposable device segments, and expansion into underserved geographic markets.

3. Which growth trends are currently influencing the market?

Current trends include the shift toward automation and digitalization of IVF labs, enabling higher throughput and reduced human error. Compact, modular incubators and closed‑system micromanipulators are gaining traction for their space efficiency and contamination control. There is also a notable rise in single‑embryo transfer protocols supported by precise embryo culture devices, which improve outcomes while lowering costs. Additionally, the adoption of point‑of‑care sperm analysis systems is accelerating, driven by demand for rapid, on‑site diagnostics.

4. How did COVID‑19 affect the Infertility Treatment Devices and Equipment Market, and what is the recovery outlook?

The pandemic caused temporary closures of fertility clinics and postponed elective procedures, leading to a short‑term dip in equipment sales. Supply‑chain disruptions affected component availability, particularly for semiconductor‑based imaging modules. However, the sector rebounded quickly as clinics resumed operations, bolstered by pent‑up demand. Recovery is now robust, with a clear trajectory toward accelerated adoption of remote monitoring tools and sterilizable, single‑use devices that align with heightened infection‑control standards.

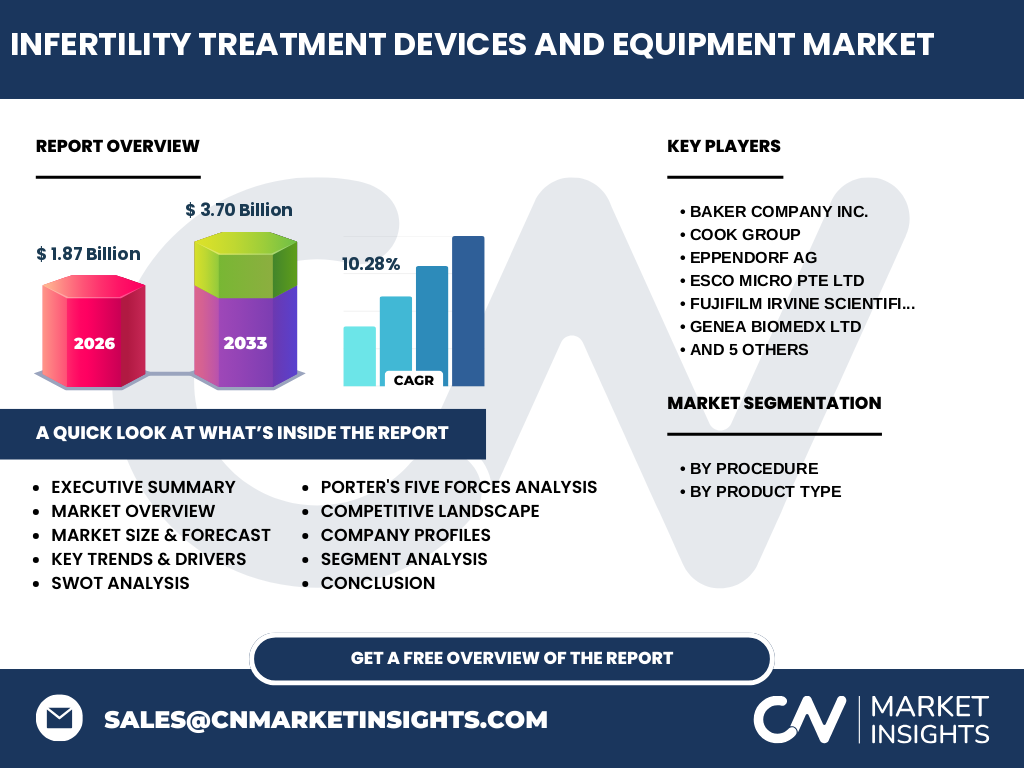

5. Who are the major competitors, and how is market consolidation evolving?

Key competitors include Baker Company INC., Cook Group, Eppendorf AG, Esco Micro Pte Ltd, FUJIFILM Irvine Scientific, Genea Biomedx Ltd, Hamilton Thorne Ltd., IVFtech APS, Rocket Medical Plc, Thermo Fisher Scientific, and Vitrolife. The competitive landscape features strategic collaborations and acquisitions aimed at broadening product portfolios—e.g., Thermo Fisher’s integration of advanced incubator technology with its existing lab‑automation suite. Consolidation is modest but trending toward niche specialization, where larger firms acquire innovative startups to secure cutting‑edge micro‑fluidic or AI‑driven solutions.

6. What are the high‑level takeaways from the market analysis?

The market is valued at US 1.87 billion in 2026 and is projected to reach US 3.70 billion by 2033, reflecting a robust CAGR of 10.28 %. Growth is propelled by rising infertility prevalence, expanding ART utilization, and rapid technological innovation. While cost and regulatory hurdles persist, emerging opportunities in automated lab platforms and emerging‑market penetration promise sustained expansion. Competitive dynamics are characterized by strategic partnerships and selective acquisitions, reinforcing a landscape that favors innovation‑driven players.

7. What are the forecast expectations for 2025‑2032?

Based on the provided CAGR of 10.28 %, the market is expected to continue its upward trajectory, roughly doubling its 2026 size by the early 2030s. This growth will be underpinned by increased demand for ART procedures, broader adoption of AI‑enabled devices, and expanding healthcare infrastructure in Asia‑Pacific and Latin America. The forecast period will also see heightened investment in R&D for next‑generation micromanipulation and incubation solutions, further expanding the market base.

8. How is the market sized and shared across product and procedure segments?

Segmentation by procedure includes Fertility Surgery, Assisted Reproductive Technology, and Artificial Insemination. By product type, the market comprises Sperm Separation Devices, Ovum Aspiration Pumps, Sperm Analyzer Systems, Micromanipulator Systems, and Incubators. While precise monetary shares are not disclosed, the Assisted Reproductive Technology segment typically commands the largest portion due to the extensive equipment required for IVF cycles. Among product types, Incubators and Micromanipulator Systems are high‑value categories, driving a substantial share of overall revenues.

9. What is the geographic distribution of market size and share?

The market exhibits a global footprint with strong presence in North America, Europe, and the Asia‑Pacific region. North America remains a mature market with high per‑procedure spending, while Europe offers steady growth backed by supportive public health policies. Asia‑Pacific is the fastest‑growing region, propelled by rising infertility rates, increasing disposable income, and expanding fertility clinic networks in countries such as China, India, and Japan. Exact regional monetary figures are aligned with the overall market valuation of US 1.87 billion (2026) and the projected US 3.70 billion (2033).

10. What are the detailed regional performance insights?

In North America, demand is driven by early adoption of automation and high‑budget clinics, resulting in premium‑price equipment sales. Europe’s market benefits from harmonized regulatory frameworks that facilitate cross‑border product placement, sustaining a balanced growth rate. Asia‑Pacific displays strong momentum due to government initiatives encouraging family planning and fertility treatments, combined with a surge in private clinic openings. Latin America and the Middle East show moderate growth, constrained by limited reimbursement but offset by increasing private healthcare investments.

11. Which companies lead the market, and what are their strategic approaches?

Thermo Fisher Scientific leads with an integrated portfolio spanning incubators to analytics, leveraging its global distribution network. FUJIFILM Irvine Scientific focuses on high‑precision micromanipulators and culture media, emphasizing R&D collaborations with academic centers. Genea Biomedx Ltd. specializes in IVF‑specific devices, pursuing market share through targeted clinician education programs. Other notable players—Baker Company INC., Cook Group, and Vitrolife—employ strategies such as product diversification, regional expansion, and strategic partnerships to strengthen their market positions.

12. How do Porter’s Five Forces affect the market?

Threat of new entrants is moderate; high capital requirements and regulatory barriers deter many newcomers, yet niche innovators can enter via specialized micro‑fluidic devices. Bargaining power of suppliers is limited, as key components (optics, electronics) are sourced from multiple vendors. Bargaining power of buyers—fertility clinics and hospitals—remains strong, driving demand for cost‑effective, high‑performance equipment. Threat of substitutes is low, given the specialized nature of infertility devices. Competitive rivalry is intense, with continuous product innovation and strategic alliances shaping the landscape.

13. What are the market’s strengths, weaknesses, opportunities, and threats?

Strengths: Strong demand growth, high clinical necessity, and fast‑advancing technology. Weaknesses: High upfront costs and reliance on skilled operators. Opportunities: Expansion into emerging economies, development of disposable single‑use devices, and integration of AI for personalized treatment. Threats: Regulatory delays, ethical controversies surrounding ART, and potential economic downturns that could limit discretionary healthcare spending.

14. How does the value chain of the market operate?

The value chain begins with raw‑material suppliers (optics, micro‑electronics), proceeds to device manufacturers that perform design, R&D, and assembly. Next are regulatory compliance and certification bodies ensuring safety standards. Distribution follows via global medical‑device distributors and direct sales teams. End‑users—fertility clinics, hospitals, and research labs—install, operate, and maintain the equipment, often supported by after‑sales service providers. Feedback loops from clinicians drive iterative product improvements and new‑generation development.

15. What investment insights should stakeholders consider?

Investors should prioritize companies with strong pipelines in automation and AI‑enhanced diagnostics, as these areas promise higher margins. Partnerships with leading fertility centers can accelerate product adoption and provide valuable clinical data. Funding for emerging‑market expansion—particularly in Asia‑Pacific—offers attractive upside due to untapped demand. Finally, evaluating a firm’s regulatory expertise and ability to navigate regional approval processes is essential for long‑term value creation.

16. What conclusions can be drawn from the analysis?

The Infertility Treatment Devices and Equipment Market is on a rapid growth path, supported by a clear increase in global infertility cases and a drive toward technologically sophisticated treatments. Despite cost and regulatory challenges, the market’s resilience is evident from its strong CAGR and expanding geographic reach. Companies that innovate, streamline regulatory pathways, and address emerging‑market needs will capture the most significant share of the projected US 3.70 billion market by 2033.

17. How was the research conducted?

The study employed a mixed‑method approach, combining secondary data from industry reports, peer‑reviewed journals, and reputable market databases with primary insights gathered through interviews with key opinion leaders in reproductive medicine. Trend analysis, financial modeling, and competitive benchmarking were applied to generate forecasts and strategic assessments.

18. What is the scope of this research?

The scope covers global market sizing, segmentation by procedure and product type, regional performance, competitive dynamics, and forward‑looking forecasts through 2033. It excludes detailed pricing analysis and does not quantify market shares for individual companies beyond the aggregate figures provided.

19. Which key companies have announced recent developments?

Thermo Fisher Scientific recently launched a next‑generation incubator with integrated temperature and gas monitoring, targeting high‑throughput IVF labs. FUJIFILM Irvine Scientific unveiled a compact micromanipulator system designed for single‑embryo transfer workflows. Genea Biomedx Ltd. announced a partnership with a leading Asian fertility network to distribute its ovum aspiration pumps across the region. Additionally, Vitrolife introduced a new line of culture media optimized for blastocyst development, complementing its existing device portfolio.