What is the Industrial Hose Market Overview – definition, scope, and significance?

The Industrial Hose Market comprises flexible conduit solutions used to transport fluids, gases, and solids across a wide range of manufacturing and process environments. Its scope covers hoses made from rubber, PVC, polyurethane, and silicone, serving sectors such as automotive, water and wastewater, oil and gas, chemicals, infrastructure, food and beverages, agriculture, and mining. The market is significant because reliable hose performance underpins operational safety, efficiency, and compliance with stringent industry standards, making it a critical component of global industrial infrastructure.

What are the key drivers, restraints, challenges, and opportunities shaping the Industrial Hose Market?

Key drivers include rising industrial automation, expanding water‑treatment projects, and growing demand for high‑performance materials in harsh environments. Restraints stem from volatile raw‑material prices and stringent regulatory compliance costs. Challenges involve maintaining product durability under extreme temperature and pressure conditions while meeting evolving safety standards. Opportunities arise from the adoption of advanced polymer blends, increasing retrofit projects in aging infrastructure, and the push for environmentally friendly hose designs that reduce hazardous waste.

What growth trends are currently influencing the Industrial Hose Market?

Current trends feature a shift toward lightweight yet high‑strength polyurethane and silicone hoses, driven by the need for improved chemical resistance and temperature tolerance. Manufacturers are also integrating IoT‑enabled monitoring sensors into hoses for real‑time pressure and leak detection. Another emerging trend is the development of reusable, recyclable hose systems that align with circular‑economy goals, especially in the water and wastewater sector.

How did COVID‑19 impact the Industrial Hose Market and what is the recovery trajectory?

The pandemic caused temporary supply‑chain disruptions and reduced capital‑expenditure in several downstream industries, leading to a short‑term slowdown in hose orders. However, recovery accelerated as the automotive and oil‑and‑gas sectors rebounded, and stimulus‑driven infrastructure projects resumed. The market is now on a robust upward path, supported by pent‑up demand and accelerated digital‑monitoring solutions that enhance operational resilience.

What does the Competitive Landscape of the Industrial Hose Market look like?

The market is moderately consolidated, led by global players such as ALFA GOMMA Spa, Eaton Corporation, Gates Corporation, Parker Hannifin Corp, and Semperit AG Holding. These firms compete on material innovation, extensive distribution networks, and strategic acquisitions. Recent consolidation activities include joint ventures and technology partnerships aimed at broadening product portfolios and strengthening regional presence, especially in emerging economies.

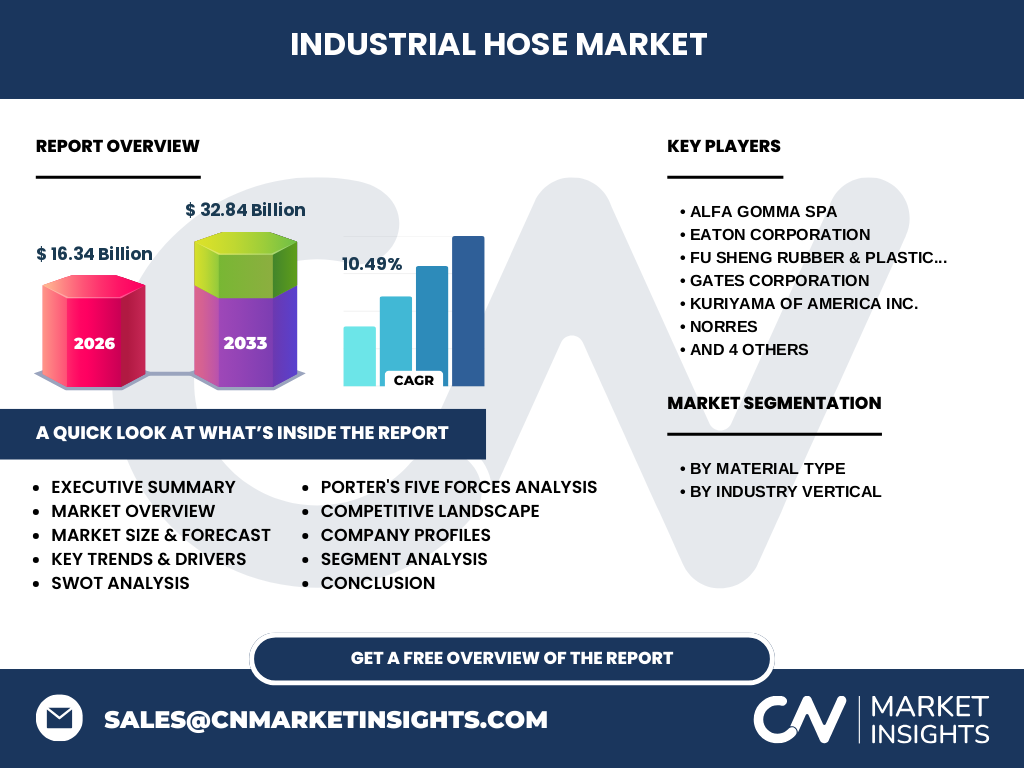

What are the high‑level insights presented in the Executive Summary?

The Industrial Hose Market is projected to reach USD 32.84 billion by 2033, growing at a CAGR of 10.49% from 2027 onward. Strong demand across multiple verticals, coupled with material‑technology advancements, drives this expansion. Key findings highlight the dominance of rubber and PVC hoses, rising importance of polyurethane and silicone for specialty applications, and the strategic emphasis on sustainability and digital integration among leading manufacturers.

What are the forecast expectations for the Industrial Hose Market from 2025‑2032?

Based on the provided CAGR of 10.49%, the market is expected to more than double its 2026 size of USD 16.34 billion by the early 2030s, reaching the forecasted USD 32.84 billion for the 2027‑2033 horizon. This growth reflects continued sectoral investments, especially in water‑treatment infrastructure, renewable‑energy‑linked oil‑and‑gas projects, and the expansion of automated manufacturing lines that require high‑performance hose solutions.

How is the Industrial Hose Market sized and shared by material type and industry vertical?

Segmentation by material type includes rubber, PVC, polyurethane, and silicone hoses, each serving distinct performance needs. By industry vertical, the market serves automotive, water and wastewater, oil and gas, chemicals, infrastructure, food and beverages, agriculture, and mining. While exact shares are not disclosed, rubber and PVC remain the volume leaders, whereas polyurethane and silicone capture higher‑margin niche segments requiring superior resistance to chemicals and temperature extremes.

What is the geographical distribution of the Global Industrial Hose Market?

The market exhibits a worldwide footprint, with strong demand in North America, Europe, and Asia‑Pacific. These regions benefit from mature industrial bases, ongoing infrastructure upgrades, and robust automotive and oil‑and‑gas activities. Emerging economies in Latin America and the Middle East also contribute to growth, driven by expanding water‑treatment projects and mining operations that require reliable hose solutions.

What does the Regional Analysis reveal about Industrial Hose Market performance?

North America leads in technology adoption, emphasizing smart‑sensor‑enabled hoses for predictive maintenance. Europe focuses on compliance with stringent environmental regulations, prompting a shift toward recyclable materials. Asia‑Pacific shows the fastest growth rate due to rapid industrialization, large‑scale infrastructure development, and burgeoning automotive production. Each region’s regulatory landscape and sectoral priorities shape product demand and innovation trajectories.

Which companies are leading the Industrial Hose Market and what are their strategic approaches?

Key players include ALFA GOMMA Spa, Eaton Corporation, Fu Sheng Rubber & Plastic Ind. Co., Ltd., Gates Corporation, Kuriyama of America Inc., Norres, Novaflex Inc., Parker Hannifin Corp, Semperit AG Holding, and Sinopulse. Strategies revolve around expanding product lines with high‑performance polymers, investing in R&D for smart‑hose technologies, pursuing geographic expansion through local partnerships, and adapting to sustainability mandates via recyclable designs.

How does Porter’s Five Forces analysis apply to the Industrial Hose Market?

Competitive rivalry is moderate, with several multinational firms vying on innovation and service. Threat of new entrants is low due to high capital requirements and stringent certification processes. Bargaining power of suppliers is moderate, as raw‑material pricing can be volatile. Bargaining power of buyers is relatively high, given the availability of multiple suppliers and price sensitivity in large‑scale contracts. Threat of substitutes remains low, as few alternatives match the flexibility and durability of engineered industrial hoses.

What are the main strengths, weaknesses, opportunities, and threats identified in the SWOT analysis?

Strengths include a broad material portfolio, critical role in essential industries, and ongoing innovation. Weaknesses involve dependence on fluctuating raw‑material costs and complex regulatory compliance. Opportunities arise from digital‑monitoring integration, sustainability‑focused product development, and expanding infrastructure projects in emerging markets. Threats encompass economic downturns affecting capital spending, increasing competition from low‑cost manufacturers, and tightening environmental legislation.

What does the value chain of the Industrial Hose Market look like?

The value chain starts with raw‑material sourcing (rubber, PVC, polymers), followed by formulation and compound mixing. Next are extrusion and molding processes that produce hose cores and reinforcements. Subsequent stages include quality testing, certification, and finishing (braiding, coating). Distribution occurs through specialized industrial distributors and direct OEM channels, culminating in end‑user installation and maintenance services, often accompanied by after‑sales support and monitoring solutions.

What key investment insights can be drawn for the Industrial Hose Market?

Investors should focus on companies with strong R&D pipelines in polyurethane and silicone technologies, as these segments command higher margins. Strategic value also lies in firms that have established digital‑monitoring capabilities, providing recurring revenue through service contracts. Geographic diversification into fast‑growing Asia‑Pacific markets and partnerships with water‑treatment and renewable‑energy projects can enhance long‑term returns.

What conclusions can be drawn about the Industrial Hose Market?

The Industrial Hose Market is on a decisive growth trajectory, projected to double in size by the early 2030s. Material innovation, sustainability, and digital integration are the primary catalysts. While raw‑material volatility and regulatory pressures pose challenges, leading manufacturers are well‑positioned to capture opportunities through advanced product offerings and strategic geographic expansion.

How was the research methodology designed for this report?

The study combined primary interviews with industry experts, secondary data from reputable market databases, and company annual reports. Trend analysis employed compound‑annual‑growth calculations based on the provided CAGR of 10.49%, while segmentation insights were derived from product catalogues and vertical‑specific demand patterns. Cross‑validation ensured consistency with publicly available financial figures.

What is the scope of this research and its limitations?

The scope covers global industrial hose demand across eight material types and eight industry verticals, focusing on the 2026 baseline and the 2027‑2033 forecast horizon. Limitations include the exclusion of country‑level breakouts and the unavailability of precise market‑share percentages for individual segments, which are not disclosed in the source data.

Which key companies have recent developments in the Industrial Hose Market?

Recent announcements include ALFA GOMMA Spa’s launch of a high‑temperature silicone hose line, Eaton Corporation’s acquisition of a specialty polymer supplier, Gates Corporation’s partnership with a leading IoT platform for smart‑hose monitoring, and Parker Hannifin’s rollout of recyclable PVC hose systems. Semperit AG Holding introduced a new polyurethane hose designed for aggressive chemicals, while Sinopulse expanded its distribution network across Southeast Asia.