1. What is the Outdoor Power Equipment Market and why is it significant?

The Outdoor Power Equipment (OPE) market comprises machines and tools designed for landscaping, lawn care, gardening, and property maintenance. It includes equipment such as lawn mowers, blowers, chainsaws, trimmers, hedge trimmers, sprayers, and mist dusters, powered by either electric or fuel sources. The market serves both commercial operators (e.g., grounds‑keeping firms, municipalities) and residential users who maintain private properties. Its significance stems from the essential role these tools play in property aesthetics, safety, and productivity, as well as from the steady demand driven by expanding urban green spaces and increasing consumer interest in home improvement.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Outdoor Power Equipment Market?

Key drivers include rising disposable income, growing awareness of landscape aesthetics, and regulatory pressure encouraging low‑emission electric equipment. Urbanization and the expansion of public parks also boost commercial demand. Restraints arise from volatile fuel prices, stricter emissions standards for fuel‑powered devices, and seasonal demand fluctuations. Challenges involve supply‑chain disruptions for electronic components and the need for skilled service technicians. Opportunities exist in the transition to battery‑electric power, smart connectivity features, and aftermarket services such as repair and rental platforms that can capture recurring revenue.

3. Which growth trends are currently influencing the Outdoor Power Equipment Market?

Current trends feature a rapid shift toward cordless, battery‑powered equipment, driven by improvements in lithium‑ion technology that enhance runtime and reduce weight. Connected or “smart” tools that integrate GPS, usage analytics, and maintenance alerts are gaining traction among professional users. Sustainability is another trend, with manufacturers adopting recyclable materials and offering take‑back programs. Additionally, there is a noticeable rise in rental and subscription models that lower upfront costs for both residential and commercial customers.

4. How did COVID‑19 affect the Outdoor Power Equipment Market and what is the recovery outlook?

The pandemic temporarily disrupted supply chains for electronic components and delayed production, leading to short‑term inventory shortages. However, lockdowns increased the amount of time people spent at home, sparking a surge in DIY landscaping and residential equipment purchases. Commercial projects slowed but rebounded as municipalities resumed maintenance activities. Recovery is now robust, with demand stabilizing and a continued focus on home improvement driving a positive trajectory toward pre‑pandemic levels.

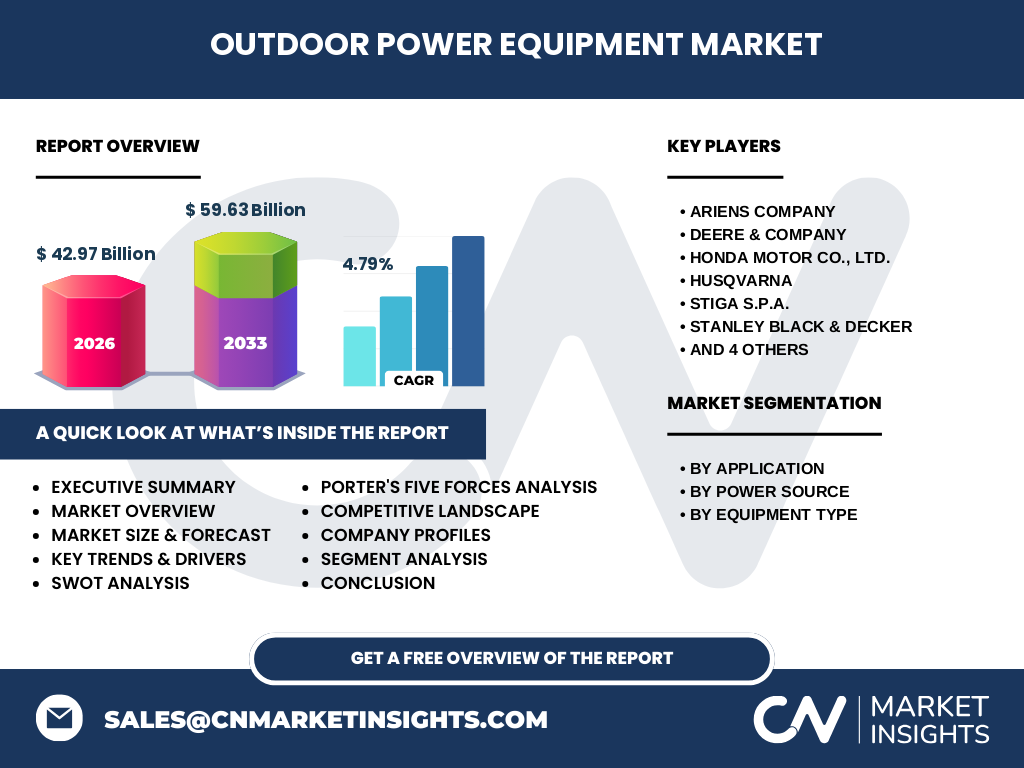

5. Who are the major competitors in the Outdoor Power Equipment Market and what is the level of consolidation?

The market is dominated by a mix of long‑standing manufacturers and innovative newcomers. Key players include Ariens Company, Deere & Company, Honda Motor Co., Ltd., Husqvarna, STIGA S.p.A., Stanley Black & Decker, Stihl, Techtronic Industries Co. Ltd., The Toro Company, and YAMABIKO Corporation. Consolidation has intensified through strategic acquisitions—particularly in the electric‑tool segment—allowing larger firms to broaden product portfolios and leverage economies of scale. Nonetheless, a vibrant pool of regional brands continues to compete on price and niche specialization.

6. What are the high‑level findings of the Outdoor Power Equipment Market?

The market was valued at $42.97 billion in 2026 and is projected to reach $59.63 billion by 2033, reflecting a compound annual growth rate (CAGR) of 4.79 %. Growth is fueled by increasing residential spending on landscaping, a shift toward environmentally friendly electric equipment, and expanding commercial infrastructure. Competitive dynamics are shaped by technology innovation, brand reputation, and geographic reach, while opportunities lie in battery advancements, smart connectivity, and service‑oriented business models.

7. What are the forecast expectations for the Outdoor Power Equipment Market from 2025 to 2032?

Based on the stated CAGR of 4.79 %, the market is expected to maintain steady expansion throughout the 2025‑2032 horizon. By 2027 the market size will exceed $45 billion, moving toward the forecast peak of $59.63 billion in 2033. The forecast assumes continued consumer confidence, ongoing urban greening initiatives, and sustained investment in electric power‑train technology across both residential and commercial segments.

8. How is the Outdoor Power Equipment Market sized and shared across its main segments?

Segmentation is based on application, power source, and equipment type. Application‑wise, the market splits between commercial and residential users, each driving distinct product preferences. Power‑source segmentation distinguishes electric‑powered from fuel‑powered units, with electric gaining share due to emissions regulations. Equipment‑type segmentation includes lawn mowers, blowers, tillers & cultivators, chainsaws, trimmers, hedge trimmers, sprayers, and mist dusters, each addressing specific task requirements. While precise monetary shares are not disclosed, all categories collectively contribute to the overall market valuation of $42.97 billion in 2026.

9. What is the geographic distribution of the Outdoor Power Equipment Market?

The market is globally dispersed, with strong demand in North America, Europe, and the Asia‑Pacific region. Developed economies exhibit higher per‑capita ownership of premium electric equipment, whereas emerging markets show robust growth in fuel‑powered tools due to lower upfront costs. Regional sales collectively support the global figure of $42.97 billion in 2026, and geographic diversification helps smooth seasonal variations across hemispheres.

10. How does the Outdoor Power Equipment Market perform in each major region?

North America leads in adoption of battery‑electric models, driven by stringent emissions policies and high consumer spending on home improvement. Europe mirrors this trend, with additional growth from government incentives for low‑emission tools. The Asia‑Pacific region displays rapid expansion, propelled by urbanization, rising middle‑class incomes, and large-scale commercial landscaping projects. Latin America and the Middle East contribute incremental growth, primarily through fuel‑powered equipment used in commercial agriculture and municipal services.

11. Which companies are leading the Outdoor Power Equipment Market and what strategies are they pursuing?

Leading firms such as Deere & Company and Husqvarna focus on expanding their electric‑tool line‑ups and leveraging advanced battery technology. Honda emphasizes hybrid power‑train solutions that bridge fuel and electric capabilities. Ariens and The Toro Company invest in retail partnerships and after‑sales service networks. Techtronic Industries pursues aggressive R&D in cordless performance, while Stanley Black & Decker integrates smart connectivity across its product portfolio. Across the board, companies are pursuing mergers, joint ventures, and strategic acquisitions to capture emerging market niches.

12. What does Porter’s Five Forces analysis reveal about the Outdoor Power Equipment Market?

• Threat of new entrants is moderate; high capital requirements for R&D and brand establishment pose barriers, yet niche electric‑tool startups can enter via crowdfunding. • Bargaining power of suppliers is moderate, especially for lithium‑ion battery cells, where few suppliers dominate. • Bargaining power of buyers is strong; residential customers can switch brands easily, prompting manufacturers to differentiate through technology and service. • Threat of substitutes is low; few alternative solutions replace the core functions of mowing, trimming, or cutting. • Industry rivalry is intense, driven by product innovation, pricing pressure, and brand loyalty.

13. What are the key strengths, weaknesses, opportunities, and threats for the Outdoor Power Equipment Market?

Strengths: Established demand across residential and commercial segments; broad product portfolio; growing acceptance of electric technology.

Weaknesses: Seasonal demand cycles; reliance on volatile raw‑material prices for batteries and engines.

Opportunities: Expansion of battery‑electric range, smart‑tool integration, rental/subscription services, and emerging markets with expanding green‑space initiatives.

Threats: Stringent environmental regulations for fuel‑powered devices, supply‑chain constraints for semiconductor components, and potential economic downturns affecting discretionary spending.

14. How is value created and transferred in the Outdoor Power Equipment value chain?

The value chain begins with raw‑material suppliers (steel, plastics, lithium‑ion cells) and component manufacturers (engines, electric motors). These feed into original equipment manufacturers (OEMs) that design, assemble, and test the final tools. Distribution follows through wholesale distributors, specialty retailers, and e‑commerce platforms. After‑sale services—maintenance, parts, and refurbishment—add further value, especially for commercial fleets. Emerging rental platforms and subscription services create a service‑oriented layer that monetizes usage rather than ownership.

15. What investment insights are most relevant for stakeholders considering the Outdoor Power Equipment Market?

Investors should prioritize companies with a clear roadmap for electrification and strong IP in battery management. Firms that have diversified distribution channels—including digital sales—and robust aftermarket service networks are positioned for higher margin growth. Strategic investments in battery‑technology partnerships or joint ventures with semiconductor providers can mitigate supply‑chain risk. Finally, targeting emerging economies through localized production can capture growth without excessive exposure to currency or tariff volatility.

16. What are the concluding takeaways from the Outdoor Power Equipment Market analysis?

The OPE market is on a solid growth trajectory, moving from a $42.97 billion base in 2026 toward $59.63 billion by 2033, driven by a 4.79 % CAGR. Electrification, smart connectivity, and service‑based business models are reshaping the competitive landscape. While fuel‑powered tools retain relevance, especially in cost‑sensitive regions, the long‑term trend favors electric solutions. Companies that invest in battery technology, after‑sales services, and regional expansion are likely to reap the greatest benefits.

17. How was the market research conducted for this report?

The methodology combined primary interviews with industry executives, surveys of commercial and residential users, and secondary analysis of company financials, regulatory filings, and trade publications. Data triangulation ensured consistency across sources, while trend extrapolation employed the disclosed CAGR of 4.79 % to project future market size. All figures reflect the latest publicly available information as of 2026.

18. What is the scope of this research and its limitations?

The scope covers global market dynamics, segmentation by application, power source, and equipment type, and regional performance across major continents. It includes competitive profiling of the ten listed companies and an assessment of macro‑economic influences. Limitations arise from reliance on publicly disclosed data; proprietary sales figures and exact regional market shares are not disclosed, so the analysis focuses on qualitative insights and aggregate financial estimates.

19. Which key companies have made notable recent developments in the Outdoor Power Equipment Market?

Recent highlights include Ariens launching a new line of high‑capacity cordless mowers, Deere & Company expanding its partnership with battery manufacturers to accelerate electric tractor offerings, and Husqvarna unveiling a connected ecosystem for professional landscaping tools. Honda introduced hybrid engine models that blend fuel efficiency with electric assist. STIGA rolled out a subscription‑based rental service in Europe, while Stanley Black & Decker acquired a smart‑sensor startup to embed usage analytics into its power tools. Techtronic Industries released a next‑generation brushless motor platform, and The Toro Company announced a joint venture aimed at developing lightweight battery packs for residential equipment. YAMABIKO focused on expanding its distribution network in Southeast Asia, targeting growing commercial landscaping demand.