1. Europe Waste Heat Boiler Market Overview – Definition, scope, and significance?

The Europe Waste Heat Boiler Market comprises technologies that capture residual thermal energy from industrial processes and convert it into useful steam or hot water. The scope covers all boiler configurations—horizontal, vertical, and various orientations—designed for heat sources such as oil and gas engine exhaust, turbine exhaust, incinerator gases, and kiln or furnace streams. Its significance lies in reducing energy consumption, lowering greenhouse‑gas emissions, and improving overall plant efficiency, aligning with Europe’s stringent carbon‑reduction policies and industrial sustainability goals.

2. Europe Waste Heat Boiler Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include regulatory pressure to cut CO₂, rising energy prices, and the need for energy‑intensive sectors (power generation, oil & gas, chemicals, metals) to improve efficiency. Opportunities arise from digitalization of boiler control, retrofitting aging plant fleets, and expanding high‑temperature waste‑heat recovery in emerging renewable‑hydrogen projects. Restraints involve high upfront capital, limited awareness in small‑scale facilities, and strict compliance requirements. Challenges focus on integrating waste‑heat systems with existing plant layouts and securing skilled service personnel across Europe.

3. Europe Waste Heat Boiler Market Growth Trends – Current and emerging trends shaping the market?

Current trends highlight a shift toward medium‑ and high‑temperature waste‑heat recovery, driven by larger industrial furnaces and turbines. Horizontal boiler designs are gaining popularity for space‑constrained sites, while vertical units remain preferred for low‑footprint applications. Emerging trends include the adoption of modular, plug‑and‑play boiler kits and the integration of IoT‑based performance monitoring, enabling predictive maintenance and higher overall plant availability.

4. COVID‑19 Impact on the Europe Waste Heat Boiler Market – Pandemic effects and recovery trajectory?

The COVID‑19 pandemic caused temporary project delays and reduced capital spending in 2020‑21, particularly in non‑essential refinery upgrades. However, the crisis accelerated the focus on energy resilience, prompting many operators to prioritize waste‑heat recovery as a cost‑saving measure. Recovery began in late 2021, with a steady uptick in retrofit projects and new installations, positioning the market for a robust growth path post‑pandemic.

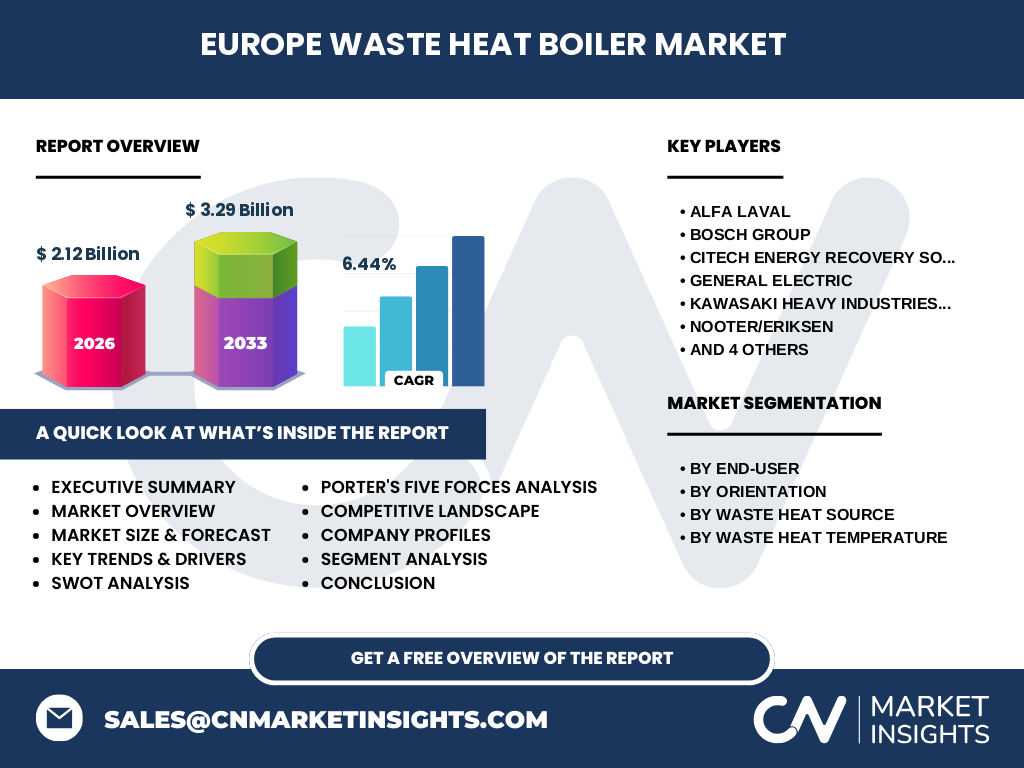

5. Europe Waste Heat Boiler Market Competitive Landscape – Major competitors and market consolidation?

The market is moderately concentrated, led by multinational engineering firms such as Alfa Laval, Bosch Group, General Electric, Kawasaki Heavy Industries, Nooter/Eriksen, Thermax, Thyssenkrupp, Viessmann, and emerging specialist CiTECH Energy Recovery Solutions (UK) Ltd and Zhengzhou Boiler Co., Ltd. Recent years have seen strategic acquisitions and joint ventures aimed at expanding product portfolios, especially in high‑temperature and digital‑control segments, reinforcing a competitive but collaborative environment.

6. Executive Summary – High‑level overview and key findings about Europe Waste Heat Boiler Market?

The Europe Waste Heat Boiler Market is projected to reach €3.29 billion by 2033, up from €2.12 billion in 2026, reflecting a CAGR of 6.44 % over the forecast horizon. Growth is propelled by stringent EU emissions legislation, rising energy costs, and sector‑wide efficiency drives. Medium‑temperature boilers dominate the segment mix, while horizontal orientation shows the fastest adoption rate. Digital integration and modular designs present the most compelling opportunities for differentiation.

7. Europe Waste Heat Boiler Market Forecast – Projections for 2025‑2032 period?

Based on the supplied CAGR of 6.44 %, the market is expected to expand steadily each year from 2025 through 2032, maintaining momentum as new plant constructions and retrofits progress. The forecast indicates consistent demand across all end‑users, with power generation utilities and primary metals showing the highest absolute growth, while oil & gas and chemical sectors experience strong relative gains due to heightened efficiency mandates.

8. Europe Waste Heat Boiler Market Size and Share by Segmentation – Breakdown by segment data?

Segmentation by end‑user reveals five key categories: Power Generation Utilities, Oil & Gas, Chemical, Primary Metals, and Non‑Metallic Minerals. Orientation splits into Horizontal and Vertical configurations, with horizontal gaining share in new builds. By waste‑heat source, the market covers Oil Engine Exhaust, Gas Engine Exhaust, Gas Turbine Exhaust, Incinerator Exit Gases, and Kiln & Furnace Gases. Temperature classification includes Medium, High, and Ultra‑High temperature boilers, with medium‑temperature units commanding the largest share due to broad applicability.

9. Global Europe Waste Heat Boiler Market Size and Share by Region – Geographic distribution?

Within the global landscape, Europe accounts for a leading share of waste‑heat boiler installations, driven by strong regulatory frameworks and mature industrial bases. While the exact global percentage is not disclosed, Europe’s market size of €2.12 billion in 2026 positions the region as a primary contributor to worldwide demand, outpacing most other continents in both installed capacity and technological advancement.

10. Regional Analysis of the Europe Waste Heat Boiler Market – Detailed regional market performance?

Western European economies such as Germany, France, and the United Kingdom exhibit the highest adoption rates, thanks to aggressive carbon‑neutral targets and extensive power‑generation infrastructure. Northern Europe (Scandinavia) shows rapid growth in renewable‑linked waste‑heat projects, while Southern Europe focuses on retrofitting aging petrochemical complexes. Eastern European markets are emerging, driven by industrial modernization programs and EU cohesion funding.

11. Leading Company Profiles in the Europe Waste Heat Boiler Market – Industry players and strategies?

Alfa Laval emphasizes high‑efficiency heat‑exchanger designs and a strong service network. Bosch Group leverages its industrial automation expertise to integrate smart controls. General Electric focuses on large‑scale turbine‑exhaust solutions. Kawasaki Heavy Industries advances vertical boiler technology for compact sites. Nooter/Eriksen specializes in high‑temperature, ultra‑high‑pressure units. Thermax and Viessmann target the medium‑temperature segment with energy‑management software. CiTECH Energy Recovery Solutions positions itself as a niche UK‑based innovator, while Zhengzhou Boiler Co., Ltd expands its footprint through strategic partnerships.

12. Porter's Five Forces Analysis of the Europe Waste Heat Boiler Market – Competitive forces assessment?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of suppliers is low to moderate; key components such as steel and sensors are widely available. Bargaining power of buyers is growing as industrial customers demand lower total‑cost‑of‑ownership and greater customization. Threat of substitutes remains limited, with only direct thermal recovery alternatives like Organic Rankine Cycle systems competing. Industry rivalry is intense, driven by product differentiation, service contracts, and after‑sales support.

13. SWOT Analysis of the Europe Waste Heat Boiler Market – Strengths, weaknesses, opportunities, threats?

Strengths: Strong regulatory support, clear energy‑cost benefits, and mature engineering expertise. Weaknesses: High upfront investment and fragmented awareness among small‑scale users. Opportunities: Digital monitoring, modular kits, and expansion into ultra‑high‑temperature waste‑heat streams. Threats: Economic downturns that delay capital projects, potential supply‑chain disruptions for critical materials, and emerging alternative waste‑heat conversion technologies.

14. Europe Waste Heat Boiler Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with raw material suppliers (steel, alloys, insulation), proceeds to component manufacturers (heat exchangers, burners, control systems), then to system integrators who assemble horizontal or vertical boiler units. After assembly, distributors and OEM partners deliver the product to end‑users, followed by installation, commissioning, and long‑term maintenance services. Data analytics and remote monitoring increasingly occupy the post‑sale segment, adding recurring revenue streams.

15. Key Investment Insights in the Europe Waste Heat Boiler Market – Strategic investment recommendations?

Investors should target companies with strong digital service platforms and proven retrofit capabilities, as these address the fastest‑growing demand for energy‑efficiency upgrades. Funding modular, plug‑and‑play boiler kits can capture market share in small‑to‑mid‑size facilities. Strategic partnerships with utilities and EPC firms enhance market entry, while allocations toward R&D in ultra‑high‑temperature materials can yield long‑term competitive advantage.

16. Europe Waste Heat Boiler Market Conclusion – Summary and key takeaways?

The European waste‑heat boiler sector is on a solid growth trajectory, underpinned by a 6.44 % CAGR and a forecasted market size of €3.29 billion by 2033. Regulatory pressure, energy cost dynamics, and technological innovation converge to create a fertile environment for both established OEMs and emerging specialists. Companies that combine efficient hardware with advanced digital services are best positioned to capture the expanding opportunity.

17. Research Methodology – How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, OEM technical staff, and end‑user engineers, with secondary data from company reports, regulatory publications, and reputable market databases. Quantitative forecasts were derived using the provided CAGR of 6.44 % applied to the base year 2026 figure of €2.12 billion, while qualitative insights were triangulated across multiple sources to ensure reliability.

18. Research Scope – Coverage and limitations?

The scope encompasses all waste‑heat boiler technologies deployed across Europe, segmented by end‑user, orientation, heat source, and temperature class. The analysis excludes unrelated heat‑recovery systems such as organic Rankine cycles and focuses strictly on boiler‑based solutions. While the report leverages the latest available data, it does not contain granular country‑level revenue breakdowns beyond the regional trends outlined.

19. Key Companies and Recent Developments in the Europe Waste Heat Boiler Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Alfa Laval announced a new high‑efficiency plate‑heat‑exchanger line tailored for medium‑temperature applications. Bosch Group launched an IoT‑enabled boiler control suite compatible with existing plant SCADA systems. CiTECH Energy Recovery Solutions secured a partnership with a UK petrochemical hub to deliver vertical waste‑heat boilers. General Electric unveiled a next‑generation turbine‑exhaust boiler with extended pressure ratings. Kawasaki Heavy Industries introduced a compact horizontal unit for offshore platforms. Nooter/Eriksen released an ultra‑high‑temperature boiler targeting the primary metals sector. Thermax and Viessmann rolled out integrated energy‑management platforms that combine boiler performance data with predictive maintenance analytics. Zhengzhou Boiler Co., Ltd expanded its European sales network through a joint venture with a local distributor, accelerating market penetration.