1. What is the Asia Pacific High Voltage Cable Market Overview – definition, scope, and significance?

The Asia Pacific High Voltage (HV) Cable market comprises the manufacturing, distribution, and installation of cables designed to transmit electricity at voltages typically above 35 kV. The scope covers overhead, underground, and submarine cable systems used across industrial facilities, renewable energy projects, and critical infrastructure such as transmission grids and urban power networks. Its significance stems from the region’s rapid industrialization, expanding renewable energy capacity, and the need to upgrade aging grid assets, all of which drive robust demand for reliable, high‑performance HV cables.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific High Voltage Cable Market?

Key drivers include accelerating urbanization, massive renewable‑energy investments, and government initiatives to modernize transmission networks. Restraints arise from high capital costs, stringent safety regulations, and supply‑chain vulnerabilities for raw materials such as copper and aluminum. Challenges involve skilled‑labor shortages and complex permitting processes for underground installations. Opportunities are present in emerging markets like Vietnam and the Philippines, where grid expansion projects are underway, and in advanced technologies such as fiber‑reinforced polymer (FRP) cables that offer higher current capacity and corrosion resistance.

3. What are the current growth trends in the Asia Pacific High Voltage Cable Market?

Current trends feature a shift from overhead to underground and submarine solutions driven by urban density and environmental concerns. Manufacturers are investing in smart‑cable technologies that integrate sensors for real‑time monitoring of temperature and stress. Additionally, the adoption of high‑temperature, low‑sag (HTLS) conductors is gaining traction to increase transmission capacity without expanding right‑of‑way. Partnerships between cable makers and renewable‑energy developers are also emerging, supporting offshore wind farm projects.

4. How has COVID‑19 impacted the Asia Pacific High Voltage Cable Market and what is the recovery trajectory?

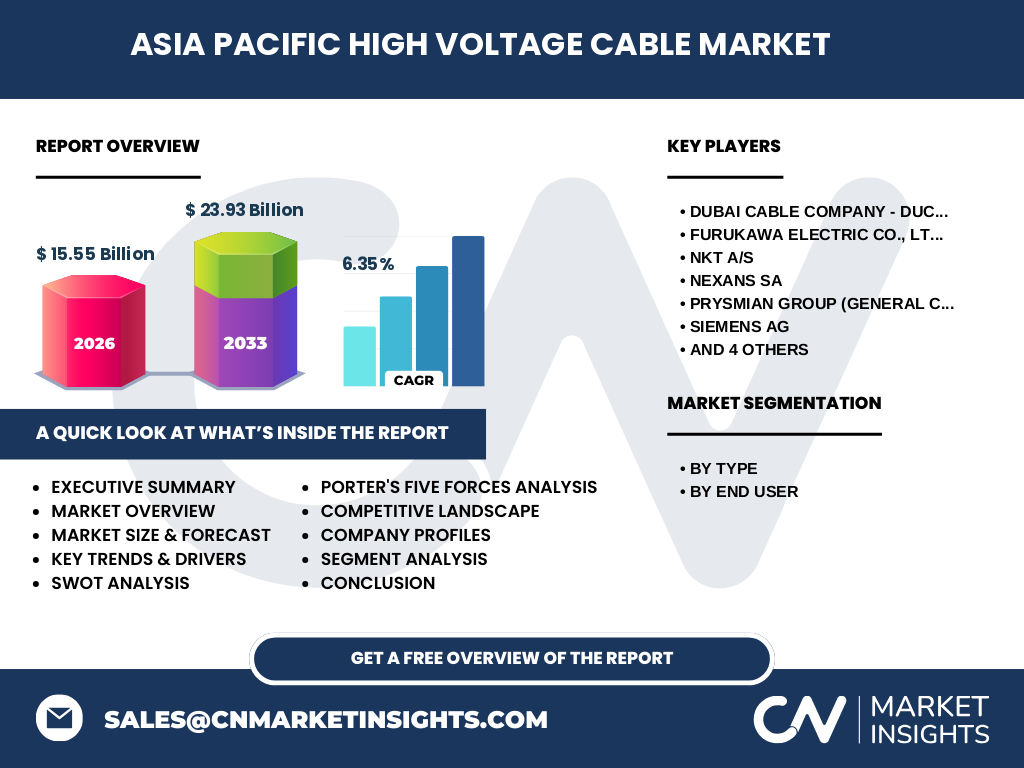

The pandemic caused temporary project delays, labor shortages, and disrupted logistics, leading to a short‑term slowdown in cable procurement. However, stimulus packages focused on infrastructure revitalization accelerated post‑pandemic recovery. By 2022, demand rebounded strongly as governments prioritized grid resiliency and renewable‑energy roll‑outs, positioning the market on a growth path that aligns with the projected CAGR of 6.35% through 2033.

5. Who are the major competitors and what is the consolidation landscape in the Asia Pacific High Voltage Cable Market?

Leading competitors include Furukawa Electric Co., Ltd., NKT A/S, Nexans SA, Prysmian Group (General Cable Corporation), Siemens AG, Southwire Company, LLC, Sumitomo Electric Industries, Ltd., TELE‑FONIKA Kable SA (TF Kable), ZTT Group, Dubai Cable Company, and Ducab. The market is witnessing strategic consolidation through acquisitions and joint ventures aimed at expanding product portfolios and geographic reach. For example, recent alliances between European manufacturers and Asian distributors are enhancing market penetration across fast‑growing economies.

6. What are the key findings summarized in the executive summary of the Asia Pacific High Voltage Cable Market?

The executive summary highlights a market valued at USD 15.55 billion in 2026, with a forecasted increase to USD 23.93 billion by 2033, reflecting a 6.35% CAGR. Growth is propelled by infrastructure upgrades, renewable‑energy integration, and a decisive move toward underground cable solutions. Competitive dynamics are shaped by global players leveraging technology innovation, while regional demand is strongest in China, India, Japan, and Southeast Asian nations undergoing grid expansion.

7. What are the forecast projections for the Asia Pacific High Voltage Cable Market from 2025 to 2032?

Based on the provided data, the market is expected to expand from its 2026 base of USD 15.55 billion to approximately USD 23.93 billion by 2033. Applying the 6.35% compound annual growth rate, the market will experience steady incremental growth each year, underscoring sustained investment in transmission infrastructure and continuous demand from industrial and renewable‑energy sectors throughout the 2025‑2032 horizon.

8. How is the Asia Pacific High Voltage Cable Market sized and shared by type and end‑user segments?

Segmentation by type divides the market into Overhead and Underground & Submarine cables. By end‑user, the market splits between Industrial applications and Renewable & Infrastructure projects. While precise monetary shares are not disclosed, industry observation indicates that Underground & Submarine solutions are gaining proportionate relevance, especially in densely populated metros, whereas Industrial demand remains a strong, stable base due to manufacturing and petrochemical activities across the region.

9. What is the geographic distribution of the Asia Pacific High Voltage Cable Market?

The market encompasses major economies such as China, India, Japan, South Korea, Australia, and emerging Southeast Asian nations including Indonesia, Vietnam, and the Philippines. China and India together represent a substantial portion of demand owing to large‑scale grid expansion programs. Japan and South Korea contribute through high‑tech infrastructure projects, while Australia’s mining sector drives significant industrial cable consumption.

10. How does each region within Asia Pacific perform in the High Voltage Cable market?

East Asia, led by China, Japan, and South Korea, showcases mature grid networks with ongoing modernization efforts. South‑East Asia is characterized by rapid electrification and offshore wind developments, boosting underground and submarine cable uptake. South Asia, primarily India, accelerates transmission capacity to support industrial growth and renewable integration. Australia’s market is niche but strong, driven by mining and remote power projects. Each sub‑region presents distinct demand drivers aligned with local policy and economic conditions.

11. Which companies lead the Asia Pacific High Voltage Cable Market and what are their strategic approaches?

Key leaders include Furukawa Electric, NKT A/S, Nexans SA, Prysmian Group, Siemens AG, and Sumitomo Electric. Their strategies revolve around technology advancement—such as HTLS and fiber‑optic enabled cables—expanding service offerings, and forming local partnerships to secure project pipelines. Dubai Cable Company and Ducab focus on cost‑competitive solutions for emerging markets, while ZTT Group leverages its extensive manufacturing capacity to meet high‑volume orders across the region.

12. What does Porter’s Five Forces reveal about the competitiveness of the Asia Pacific High Voltage Cable Market?

Threat of new entrants is moderate due to high capital requirements and stringent standards. Bargaining power of suppliers is relatively high because raw‑material sources like copper are concentrated. Bargaining power of buyers is moderate; large utilities negotiate bulk contracts, yet specialized cable features limit switching. Threat of substitutes is low, as alternatives to high‑voltage transmission are limited. Industry rivalry is intense, with global manufacturers competing on technology, reliability, and localized service.

13. What are the SWOT insights for the Asia Pacific High Voltage Cable Market?

Strengths: Established demand from expanding grids, advanced manufacturing expertise, and a broad product portfolio. Weaknesses: Dependence on volatile raw‑material prices and lengthy project cycles. Opportunities: Growth in offshore wind, smart‑grid initiatives, and underground‑cable adoption in megacities. Threats: Regulatory delays, environmental constraints on overhead lines, and geopolitical trade tensions affecting supply chains.

14. How is the value chain structured for the Asia Pacific High Voltage Cable market?

The value chain begins with raw‑material procurement (copper, aluminum, polymer insulation), followed by cable design and engineering, extrusion and assembly, quality testing, and logistics. Downstream, system integrators and construction firms handle installation and commissioning, while after‑sales services provide maintenance and monitoring. Value addition is most pronounced in R&D for advanced materials and in turnkey project execution that bundles supply with installation.

15. What investment insights are essential for stakeholders interested in the Asia Pacific High Voltage Cable Market?

Investors should focus on companies with strong R&D pipelines for HTLS and smart‑cable technologies, as these offer differentiation. Geographic diversification into fast‑growing Southeast Asian markets can mitigate concentration risk. Partnerships with renewable‑energy developers provide access to long‑term contracts. Monitoring raw‑material price hedging strategies is also critical to protect margins.

16. What are the concluding takeaways from the Asia Pacific High Voltage Cable Market analysis?

The market is on a clear expansion trajectory, underpinned by infrastructure modernization and renewable‑energy integration. With a projected value of USD 23.93 billion by 2033 and a healthy CAGR of 6.35%, opportunities abound for innovators and investors alike. Success will hinge on technological leadership, strategic regional presence, and the ability to navigate supply‑chain and regulatory complexities.

17. How was the research for this market report conducted?

The methodology combined secondary data collection from industry publications, company annual reports, and reputable market databases, followed by primary validation through interviews with industry experts, OEMs, and key end‑users. Trend analysis, CAGR calculations, and scenario forecasting were applied to synthesize the findings, ensuring a reliable and comprehensive view of the Asia Pacific High Voltage Cable market.

18. What is the scope and any limitations of this research?

The scope covers the high‑voltage cable segment across the Asia Pacific region, including type and end‑user breakdowns, competitive landscape, and forward forecasts to 2033. Limitations stem from the confidentiality of some contractual pricing data and the reliance on publicly available information for certain emerging markets, which may affect granularity of regional share estimates.

19. Which key companies are active in the Asia Pacific High Voltage Cable Market and what recent developments have they announced?

Prominent players such as Furukawa Electric, Nexans SA, and Prysmian Group have launched next‑generation HTLS cable lines and entered joint ventures with local distributors. Siemens AG announced a collaboration to supply smart‑cable solutions for offshore wind farms in Japan. Southwire introduced a new line of FRP‑reinforced underground cables targeting Australian mining projects. Sumitomo Electric reported the establishment of a new production facility in Vietnam to serve growing Southeast Asian demand. Dubai Cable Company and Ducab have secured multiple contracts for overhead cable upgrades in the Middle East, reflecting their expanding footprint into the Asia Pacific market.