Asia Pacific Waste Heat Boiler Market Overview - Definition, scope, and significance?

The Asia Pacific Waste Heat Boiler Market comprises technologies that capture residual heat from industrial processes and convert it into useful steam or power. The scope includes design, manufacturing, installation, and servicing of boilers that recover heat from sources such as engine exhaust, gas turbines, incinerators, and kilns across diverse end‑users. Its significance lies in improving energy efficiency, reducing carbon emissions, and lowering operating costs, making it a strategic component of sustainability initiatives in fast‑growing Asian economies.

Asia Pacific Waste Heat Boiler Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers are stringent environmental regulations, rising energy prices, and government incentives for energy‑saving projects. Industrial expansion in China, India, Japan, and Southeast Asia fuels demand for waste‑heat recovery. Restraints include high upfront capital costs, limited awareness in smaller enterprises, and the technical complexity of integrating boilers with existing plants. Challenges revolve around varying fuel qualities and maintenance skill gaps, while opportunities emerge from digital monitoring solutions, modular boiler designs, and growing interest in carbon‑neutral manufacturing.

Asia Pacific Waste Heat Boiler Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward high‑efficiency, ultra‑high temperature boilers that can handle diverse waste‑heat streams. Manufacturers are adopting advanced materials to extend lifespan under corrosive conditions. Emerging trends include IoT‑enabled performance analytics, hybrid systems that combine waste‑heat boilers with renewable power sources, and increased adoption of vertical orientation designs for space‑constrained sites. Collaborative projects between OEMs and utilities are also accelerating market penetration.

COVID-19 Impact on the Asia Pacific Waste Heat Boiler Market - Pandemic effects and recovery trajectory?

The pandemic caused temporary project postponements due to lockdowns and supply‑chain disruptions, reducing new installations in 2020‑2021. However, the slowdown prompted many firms to reassess energy costs, leading to accelerated retrofits once operations normalized. Recovery has been steady, with a resurgence of capital spending in 2022‑2023, supported by stimulus packages that emphasize green technologies. The market is now on a clear upward trajectory toward pre‑pandemic growth rates.

Asia Pacific Waste Heat Boiler Market Competitive Landscape - Major competitors and market consolidation?

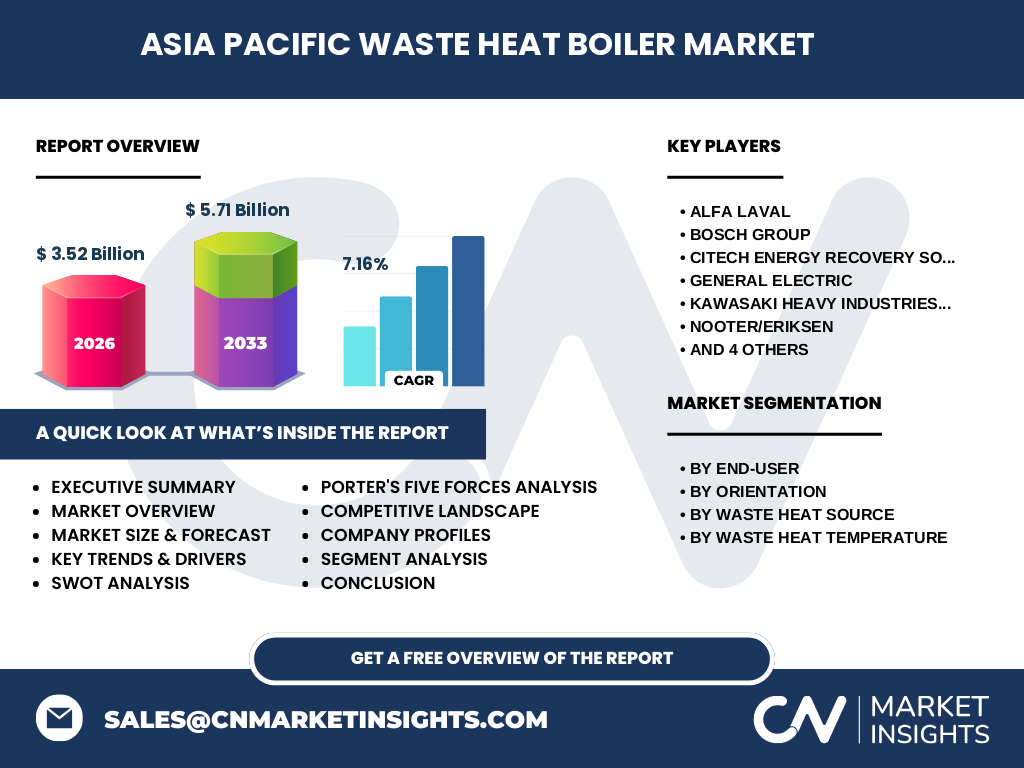

The competitive arena features global leaders such as Alfa Laval, Bosch Group, General Electric, Kawasaki Heavy Industries, Nooter/Eriksen, Thermax, Thyssenkrupp, Viessmann, and regional players like Zhengzhou Boiler Co. Consolidation is evident through strategic acquisitions and joint ventures aimed at expanding product portfolios and regional reach. Partnerships with local engineering firms help larger OEMs navigate regulatory environments and tailor solutions to specific end‑users.

Executive Summary - High-level overview and key findings about Asia Pacific Waste Heat Boiler Market?

The Asia Pacific Waste Heat Boiler Market is valued at USD 3.52 billion in 2026 and is forecast to reach USD 5.71 billion by 2033, expanding at a CAGR of 7.16 %. Growth is driven by regulatory pressure, rising energy costs, and industrial modernization. Segmental analysis shows strong demand from power generation utilities and oil & gas, while horizontal and vertical orientations cater to varied plant footprints. The market is poised for continued expansion, with technology innovation and financing mechanisms identified as critical success factors.

Asia Pacific Waste Heat Boiler Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 7.16 %, the market is expected to progress from the 2026 baseline of USD 3.52 billion to approximately USD 5.71 billion by 2033. This trajectory implies steady annual increments, reflecting expanding industrial capacity, heightened sustainability commitments, and increasing adoption of advanced boiler configurations across the region.

Asia Pacific Waste Heat Boiler Market Size and Share by Segmentation - Breakdown by segmentData?

Segmentation by end‑user highlights Power Generation Utilities, Oil & Gas, Chemical, Primary Metals, and Non‑Metallic Minerals as primary adopters, with utilities leading due to large‑scale steam requirements. Orientation splits between Horizontal and Vertical designs, each serving distinct space and process constraints. Waste‑heat source categories—Oil Engine Exhaust, Gas Engine Exhaust, Gas Turbine Exhaust, Incinerator Exit Gases, and Kiln & Furnace Gases—show diversified applicability. Temperature classes (Medium, High, Ultra‑High) dictate technology choice, with Ultra‑High gaining traction in high‑pressure petrochemical plants.

Global Asia Pacific Waste Heat Boiler Market Size and Share by Region - Geographic distribution?

The Asia Pacific region accounts for the entire market under study, encompassing major economies such as China, India, Japan, South Korea, and the ASEAN bloc. Within this geography, China and India together represent the largest share, driven by extensive manufacturing bases and aggressive energy‑efficiency policies. Southeast Asian nations contribute incremental growth through emerging petrochemical and cement sectors.

Regional Analysis of the Asia Pacific Waste Heat Boiler Market - Detailed regional market performance?

East Asia (China, Japan, South Korea) shows mature adoption with a focus on high‑temperature boilers for steel and chemical complexes. South Asia (India, Bangladesh) is characterized by rapid expansion of power‑generation capacity and oil & gas infrastructure, prompting medium‑temperature solutions. Southeast Asia (Indonesia, Vietnam, Malaysia) demonstrates growing interest in waste‑heat recovery from incinerators and biomass plants, supported by government incentives for clean energy.

Leading Company Profiles in the Asia Pacific Waste Heat Boiler Market - Industry players and strategies?

Alfa Laval emphasizes integrated heat‑exchange solutions and digital monitoring. Bosch Group leverages its strong engineering base to offer modular boiler kits. CiTECH Energy focuses on bespoke recovery systems for the UK‑Asia corridor. General Electric combines waste‑heat boilers with its broader power‑generation portfolio. Kawasaki Heavy Industries stresses robust vertical designs for space‑limited plants. Nooter/Eriksen specializes in high‑temperature, high‑pressure units. Thermax and Viessmann target cost‑effective medium‑temperature boilers for SMEs. Thyssenkrupp provides turnkey projects, while Zhengzhou Boiler Co. offers competitive pricing for large‑scale installations.

Porter's Five Forces Analysis of the Asia Pacific Waste Heat Boiler Market - Competitive forces assessment?

Threat of New Entrants: Moderate; high capital requirements and technical expertise limit newcomers. Bargaining Power of Suppliers: Low to moderate, as raw‑material suppliers are fragmented. Bargaining Power of Buyers: Increasing, because large utilities can negotiate pricing and demand customized solutions. Threat of Substitutes: Limited; alternative energy‑efficiency measures exist but do not fully replace waste‑heat recovery. Industry Rivalry: High, driven by several well‑established global and regional firms competing on technology, service, and price.

SWOT Analysis of the Asia Pacific Waste Heat Boiler Market - Strengths, weaknesses, opportunities, threats?

Strengths: Strong environmental drivers, proven cost‑savings, and mature technology base. Weaknesses: High upfront investment and variable technical expertise across the region. Opportunities: Expansion into emerging sectors (e.g., renewable‑hybrid plants), digitalization of performance analytics, and government‑backed financing schemes. Threats: Economic slowdowns, fluctuating energy prices, and potential regulatory changes that could affect subsidy structures.

Asia Pacific Waste Heat Boiler Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material suppliers (steel, alloys, sensors), proceeds to component manufacturers (heat exchangers, burners), then to OEMs that assemble complete boiler systems. System integration firms add control and monitoring software, followed by installation contractors who commission the plants. After‑sale services—including maintenance, spare parts, and performance optimization—complete the chain, creating recurring revenue streams for manufacturers.

Key Investment Insights in the Asia Pacific Waste Heat Boiler Market - Strategic investment recommendations?

Investors should prioritize companies with strong R&D pipelines in ultra‑high temperature technology and robust service networks. Partnerships with local utilities can de‑risk project execution. Funding mechanisms that bundle capital expenditure with energy‑saving performance guarantees are attractive. Additionally, focus on firms expanding modular product lines to serve small‑ and medium‑size enterprises, a segment currently under‑penetrated.

Asia Pacific Waste Heat Boiler Market Conclusion - Summary and key takeaways?

The market is on a solid growth path, propelled by regulatory pressure, cost‑reduction imperatives, and technological advances. With a projected CAGR of 7.16 % leading to a USD 5.71 billion market size by 2033, opportunities abound across all segments. Companies that innovate in efficiency, digital monitoring, and flexible financing will capture the greatest share, while investors can benefit from the sector’s stability and long‑term revenue potential.

Research Methodology - How this research was conducted?

The study employed a combination of primary interviews with industry experts, secondary data collection from reputable sources, and quantitative modeling. Market sizing used a bottom‑up approach, aggregating known project values and capacity forecasts. Trend analysis incorporated technology adoption rates and policy reviews. All figures were cross‑checked against publicly available financial reports and governmental statistics.

Research Scope - Coverage and limitations?

The scope encompasses the entire Asia Pacific region, covering all major end‑users, boiler orientations, waste‑heat sources, and temperature categories listed. It excludes unrelated boiler technologies such as biomass‑only systems. While the analysis captures major market dynamics, granular country‑level financial data beyond the provided aggregate figures were not incorporated.

Key Companies and Recent Developments in the Asia Pacific Waste Heat Boiler Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Alfa Laval announced a new ultra‑high temperature series targeting petrochemical clusters in China. Bosch Group launched a digital twin platform for real‑time boiler performance monitoring. CiTECH Energy secured a partnership with an Indian conglomerate to supply customized waste‑heat solutions for cement plants. General Electric introduced a hybrid waste‑heat boiler that integrates with its gas‑turbine portfolio. Kawasaki Heavy Industries unveiled a space‑saving vertical boiler for offshore platforms. Nooter/Eriksen announced a joint venture with a Southeast Asian EPC firm to expand its high‑pressure offerings. Thermax released a cost‑effective medium‑temperature boiler line for small manufacturers. Thyssenkrupp completed a turnkey waste‑heat recovery project for a Japanese steel mill. Viessmann expanded its service network in India, and Zhengzhou Boiler Co. reported a significant increase in export orders to Vietnam and Indonesia.