1. What is the Asia Pacific Oligonucleotide Synthesis Market Overview – definition, scope, and significance?

The Asia Pacific Oligonucleotide Synthesis Market encompasses the production and supply of custom‑made DNA and RNA fragments, as well as the reagents, equipment, and services required for their synthesis. The scope includes all activities from design, automated synthesis, purification, and quality control to downstream applications in research, diagnostics, and therapeutics across the region. Its significance stems from the rapid expansion of genomic research, personalized medicine, and molecular diagnostics, all of which rely heavily on high‑quality oligonucleotides. The market’s strategic importance is amplified by strong governmental investments in biotech infrastructure and a growing number of academic and commercial laboratories seeking tailored nucleic‑acid solutions.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Oligonucleotide Synthesis Market?

Key drivers include escalating demand for nucleic‑acid‑based therapeutics, the surge in COVID‑19‑related diagnostic testing, and rising research funding in countries such as China, Japan, and South Korea. The region’s large talent pool and cost‑effective manufacturing base further accelerate growth. Restraints involve stringent regulatory requirements for clinical‑grade oligos and limited intellectual‑property frameworks in emerging economies. Challenges arise from the technical complexity of scaling up high‑fidelity synthesis and the need for continuous innovation to reduce error rates. Opportunities are evident in the adoption of novel enzymatic synthesis platforms, expansion of on‑site manufacturing for biotech clusters, and the development of next‑generation diagnostic assays that demand specialized oligonucleotide designs.

3. Which growth trends are currently influencing the Asia Pacific Oligonucleotide Synthesis Market?

Several trends are redefining the market landscape. First, the shift from traditional phosphoramidite chemistry to enzymatic and microarray‑based synthesis is gaining momentum, promising faster turnaround and lower waste. Second, the integration of AI‑driven sequence design tools is shortening development cycles for therapeutics and diagnostics. Third, collaborations between academic institutes and biotech firms are fostering co‑development of disease‑specific oligo libraries. Finally, the emergence of “lab‑on‑a‑chip” diagnostic platforms is creating niche demand for ultra‑short, high‑purity oligonucleotides.

4. How has COVID‑19 impacted the Asia Pacific Oligonucleotide Synthesis Market, and what is the recovery trajectory?

The pandemic triggered an unprecedented spike in demand for diagnostic primers and probes, prompting many manufacturers to expand capacity and adopt rapid‑scale production lines. While the initial disruption affected supply chains for raw materials, the market rebounded quickly as governments prioritized testing. Post‑pandemic, the momentum has transitioned into sustained growth, with many companies retaining the expanded infrastructure to serve broader applications beyond infectious disease testing, thereby establishing a robust recovery trajectory.

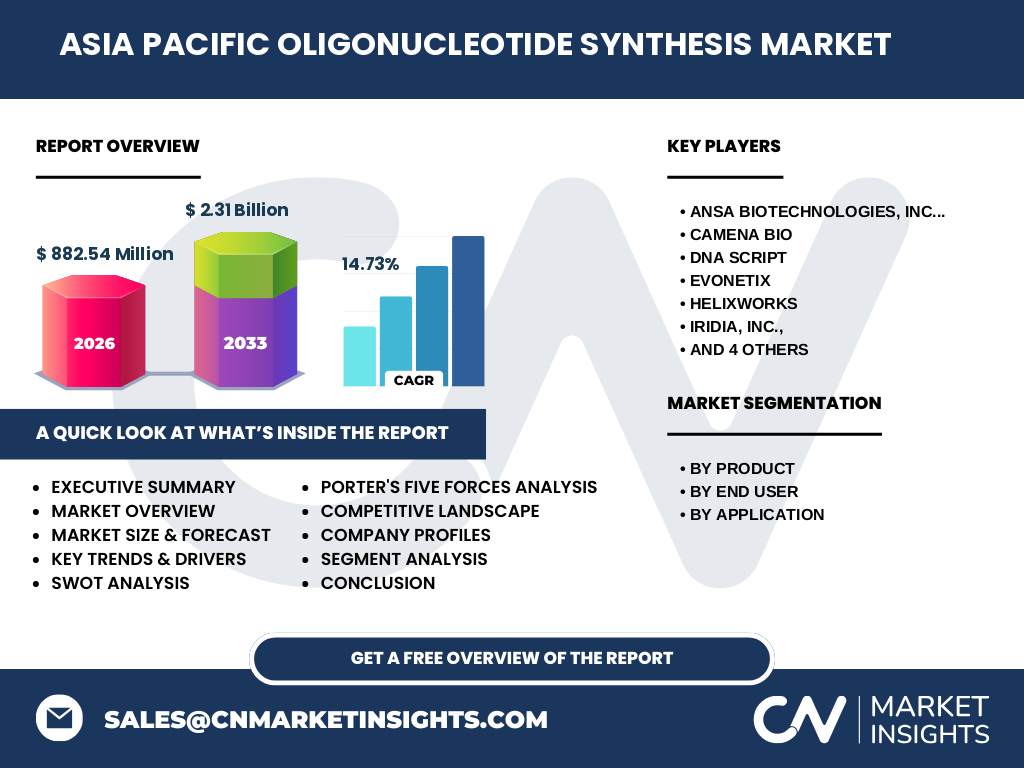

5. Who are the major competitors, and what does the competitive landscape look like in the Asia Pacific Oligonucleotide Synthesis Market?

The market is fragmented, featuring both global leaders and emerging regional specialists. Key players include Ansa Biotechnologies, Inc., Camena Bio, DNA Script, Evonetix, Helixworks, Iridia, Inc., Molecular Assemblies, Nuclera Nucleics Ltd, Synthomics, Inc., and Twist Bioscience. Competition centers on technology differentiation (e.g., enzymatic versus solid‑phase synthesis), portfolio breadth, pricing, and turnaround speed. Recent consolidation activity is modest, but strategic alliances and joint ventures are common as firms seek to combine synthesis expertise with distribution networks across Asia Pacific.

6. What are the high‑level findings and key takeaways presented in the Executive Summary?

The Executive Summary underscores a market valued at USD 882.54 million in 2026, projected to reach USD 2.31 billion by 2033 with a CAGR of 14.73 %. Growth is driven by therapeutic oligo pipelines, expanding diagnostic needs, and increased research funding. Technological innovation—especially enzymatic synthesis—emerges as a pivotal catalyst. While regulatory complexity poses a restraint, the region’s supportive policy environment and rising biotech clusters offer compelling opportunities for expansion and investment.

7. What are the forecasted market dynamics for the period 2025‑2032?

Forecasts indicate continued double‑digit expansion, maintaining an average CAGR close to 15 %. By 2032, the market is expected to exceed the USD 2 billion mark, propelled by broader adoption of oligonucleotide therapeutics, growth in personalized diagnostics, and the scaling of automated synthesis equipment. The forecast reflects confidence in both organic growth from existing customers and new demand from emerging biotech hubs within the region.

8. How is the market size and share distributed across product, end‑user, and application segments?

Segmentation reveals three primary product categories: Synthesized Oligonucleotides, Reagents, and Equipment. Synthesized Oligonucleotides constitute the largest share, driven by therapeutic and diagnostic orders. Reagents and Equipment follow, supporting the expanding synthesis capacity. End‑user segmentation shows Academic Research Institutes and Pharmaceutical & Biotechnology Companies as the dominant consumers, with Diagnostic Laboratories gaining traction as point‑of‑care testing expands. Application‑wise, Research remains the biggest driver, while Diagnostics and Therapeutics are the fastest‑growing segments, reflecting the market’s shift toward clinical and commercial use cases.

9. What is the geographic distribution of the market across the Asia Pacific region?

Geographically, China leads in absolute terms due to its massive research ecosystem and strong governmental biotech initiatives. Japan follows, leveraging its advanced medical device sector and mature pharmaceutical industry. South Korea and Australia present high‑value niches, particularly in diagnostic assay development and high‑precision synthesis equipment. Smaller economies such as Singapore and Taiwan contribute through specialized biotech clusters and favorable R&D tax regimes.

10. Can you provide a detailed regional analysis of market performance?

In China, market growth is fueled by national programs targeting gene‑editing therapies and large‑scale vaccine production, creating a robust pipeline for custom oligos. Japan’s performance is anchored by its aging population and demand for personalized medicine, prompting pharmaceutical firms to outsource oligo synthesis. South Korea distinguishes itself through strong collaborations between universities and contract manufacturing organizations, accelerating the commercialization of nucleic‑acid therapeutics. Australia’s growth is driven by its emphasis on translational research and government‑backed grants for diagnostic innovation. Each sub‑region demonstrates a unique mix of funding, regulatory pathways, and industry partnerships that shape local demand.

11. Which companies are leading the market, and what strategies are they employing?

Twist Bioscience leads with its silicon‑based high‑throughput synthesis platform, targeting large‑scale therapeutic contracts. DNA Script focuses on enzymatic synthesis, positioning itself as a rapid‑turnaround solution for COVID‑19 diagnostics and emerging mRNA therapeutics. Evonetix differentiates through its microfluidic synthesis technology, offering on‑demand, low‑volume production for research labs. Companies such as Ansa Biotechnologies and Camena Bio are expanding their presence via strategic partnerships with regional distributors, while Helixworks and Molecular Assemblies invest in automation to improve yield and reduce cost‑of‑goods. The overall strategic theme is technology leadership combined with geographic expansion.

12. How does Porter’s Five Forces assessment characterize market competitiveness?

• Threat of New Entrants: Moderate; high capital investment in synthesis equipment and IP barriers limit newcomers, yet the rise of low‑cost enzymatic kits lowers entry hurdles for niche players.

• Bargaining Power of Suppliers: Low to moderate; raw‑material suppliers for phosphoramidites are concentrated, but alternative chemistries diversify sourcing.

• Bargaining Power of Buyers: Increasing; large pharmaceutical contracts demand competitive pricing and quality guarantees.

• Threat of Substitutes: Low; few alternatives to custom oligonucleotides for molecular biology applications.

• Competitive Rivalry: High; firms compete on speed, accuracy, cost, and technology breadth, driving continuous innovation.

13. What are the Strengths, Weaknesses, Opportunities, and Threats identified in the SWOT analysis?

Strengths: Rapidly expanding biotech ecosystem, robust R&D funding, and advanced manufacturing capabilities.

Weaknesses: Complex regulatory pathways for clinical‑grade oligos and fragmented supply chains for specialty reagents.

Opportunities: Enzymatic synthesis breakthroughs, growth of personalized diagnostics, and increasing outsourcing of therapeutic oligo production.

Threats: Potential trade restrictions on key raw materials, intellectual‑property disputes, and the risk of price compression as more players achieve scale.

14. How is the value chain structured for the Asia Pacific Oligonucleotide Synthesis Market?

The value chain begins with raw‑material suppliers (phosphoramidites, enzymes, purification media), proceeds to design and bioinformatics services that generate target sequences, moves to contract manufacturing and in‑house synthesis facilities where automated or enzymatic platforms produce the oligos, followed by purification and quality‑control laboratories ensuring compliance with specifications. Downstream, distribution networks deliver finished products to end users, while post‑sale support (technical assistance, data analysis) adds value. Integration points such as combined design‑synthesis platforms are emerging as differentiators.

15. What investment insights can be derived for stakeholders interested in this market?

Investors should prioritize companies with proprietary enzymatic synthesis technologies, as these are expected to capture a larger share of the fast‑growing diagnostic segment. Strategic funding of regional contract manufacturing organizations can yield stable cash flows, given the sustained demand from pharma and biotech firms. Partnerships with academic institutions provide early access to innovative oligo applications, mitigating R&D risk. Finally, monitoring regulatory developments in China and Japan will be critical to time market entry and scale‑up investments effectively.

16. What are the concluding remarks and key takeaways from this research?

The Asia Pacific Oligonucleotide Synthesis Market is on a strong growth trajectory, supported by a solid base of research activity, expanding therapeutic pipelines, and heightened diagnostic needs. With a projected market size of USD 2.31 billion by 2033 and a 14.73 % CAGR, the region offers attractive opportunities for technology innovators, contract manufacturers, and investors. Success will depend on mastering regulatory compliance, investing in next‑generation synthesis platforms, and leveraging regional partnerships to capture emerging demand.

17. How was the research conducted and what methodology was applied?

The study employed a mixed‑method approach, combining primary interviews with senior executives from leading oligonucleotide suppliers, end‑user laboratories, and regulatory bodies, with secondary data extraction from industry reports, scientific publications, and government databases. Quantitative forecasts were generated using time‑series analysis anchored to the 2026 market size of USD 882.54 million and extrapolated with a CAGR of 14.73 % through 2033. Qualitative insights were cross‑validated across multiple sources to ensure reliability.

18. What is the scope of this research and what limitations, if any, should readers be aware of?

The scope covers the full spectrum of oligonucleotide synthesis activities in the Asia Pacific, including product, end‑user, and application segmentation, as well as competitive, regulatory, and technological aspects. Limitations stem from the confidential nature of some contract values, which restricts precise market‑share quantification. Additionally, rapid technological shifts—particularly in enzymatic synthesis—may alter competitive dynamics faster than the annual update cycle.

19. Which key companies are highlighted and what recent developments have they announced?

Key players include Ansa Biotechnologies, Camena Bio, DNA Script, Evonetix, Helixworks, Iridia, Molecular Assemblies, Nuclera Nucleics, Synthomics, and Twist Bioscience. Recent developments feature DNA Script’s launch of a rapid COVID‑19 detection kit leveraging its enzymatic platform, Twist Bioscience’s expansion of a silicon‑based high‑throughput facility in Shanghai, and Evonetix’s partnership with a Japanese biotech consortium to co‑develop microfluidic synthesis for mRNA vaccines. Camena Bio announced a collaboration with a South Korean university to create custom CRISPR guide RNAs, while Helixworks introduced an automated purification system aimed at reducing time‑to‑market for therapeutic oligos.