What is the Autonomous Navigation Market overview – definition, scope, and significance?

The Autonomous Navigation Market encompasses technologies that enable vehicles, robots, and vessels to perceive their environment, plan routes, and move without human intervention. It covers hardware such as sensors and processing units, software algorithms, and integrated navigation systems for land, marine, and space platforms. The market’s significance lies in its ability to boost operational efficiency, reduce labor costs, enhance safety, and unlock new business models across commercial and defense sectors.

What are the market drivers, restraints, challenges, and opportunities?

Key drivers include rising demand for automation in logistics, growing investment in defense unmanned systems, and rapid advances in AI and sensor tech. Restraints involve high upfront costs, regulatory uncertainty, and cybersecurity concerns. Challenges stem from integration complexity across heterogeneous platforms and limited skilled talent. Opportunities arise from emerging applications in smart cities, autonomous shipping, and space exploration, as well as from collaborations between hardware manufacturers and software developers.

Which growth trends are currently shaping the Autonomous Navigation market?

Current trends feature convergence of 5G connectivity with navigation solutions, enabling real‑time data exchange for fleet coordination. Edge‑computing is increasingly embedded in processing units to lower latency. There is a shift toward modular, scalable architectures that support multi‑modal vehicles. Additionally, the adoption of digital twins for testing and validation accelerates product development cycles.

How did COVID‑19 impact the Autonomous Navigation market and what is the recovery trajectory?

The pandemic initially slowed supply chains and delayed capital projects, reducing short‑term orders for autonomous systems. However, heightened focus on contact‑less operations and e‑commerce logistics spurred demand for AGVs and delivery drones. Recovery has been robust, with a resurgence in investment and a clear upward trajectory that aligns with the market’s projected CAGR of 16.03% through 2032.

What does the competitive landscape look like and are there signs of market consolidation?

The market is moderately consolidated, featuring a mix of established aerospace firms, specialized robotics companies, and emerging AI startups. Major players such as Collins Aerospace, Thales Group, and Trimble Inc. hold strong positions in navigation hardware, while firms like Brain Corporation and KINEXON excel in software and processing solutions. Recent M&A activity indicates a trend toward vertical integration, as larger entities acquire niche technology providers to broaden their autonomous portfolios.

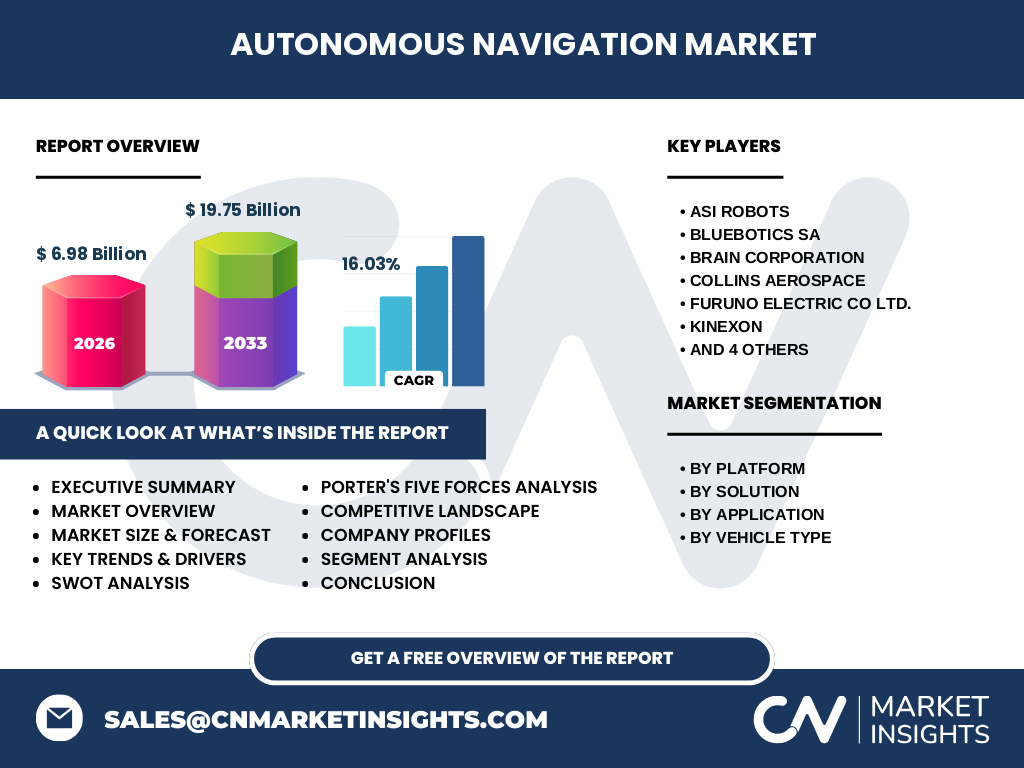

Can you provide an executive summary with the key findings?

The Autonomous Navigation market is valued at $6.98 billion in 2026 and is projected to reach $19.75 billion by 2033, delivering a 16.03% CAGR. Growth is driven by cross‑industry automation需求, advances in AI‑powered sensing, and expanding defense budgets. While cost and regulatory hurdles persist, opportunities in smart logistics, autonomous maritime transport, and space exploration promise sustained expansion. Competitive dynamics favor firms that combine hardware depth with software agility.

What are the forecast projections for 2025‑2032?

Based on the provided CAGR of 16.03%, the market is expected to maintain strong upward momentum, moving from roughly $6 billion in the mid‑2020s to close to $20 billion by the early 2030s. Annual growth will be driven by incremental adoption across land, marine, and space platforms, with the commercial sector contributing the bulk of volume and the defense sector providing higher‑margin contracts.

How is the market sized and shared by segmentation?

Segmentation spans platform, solution, application, and vehicle type. Platform-wise, land solutions dominate due to extensive AGV and mobile robot deployments, followed by marine and space niches. Solution categories are led by sensing systems and navigation systems, with processing units and software gaining share as AI integration deepens. Application is split between commercial and defense, with commercial driving volume. Vehicle‑type breakdown highlights AGVs and mobile robots as primary revenue generators, while UUVs and drones capture growing niche markets.

What is the global market size and share by region?

The market is globally distributed, reflecting strong adoption in North America, Europe, and the Asia‑Pacific. While exact regional monetary values are not disclosed, these regions collectively account for the majority of the $6.98 billion 2026 valuation, driven by robust logistics networks, advanced aerospace programs, and supportive regulatory frameworks.

What does regional analysis reveal about market performance?

North America leads in defense contracts and autonomous vehicle testing, backed by substantial R&D investment. Europe shows a balanced mix of commercial automation in manufacturing and maritime autonomous projects. Asia‑Pacific registers rapid growth due to large‑scale manufacturing, smart‑city initiatives, and expanding marine trade routes. Emerging economies in the region are poised for accelerated adoption as infrastructure modernizes.

Which companies are leading and what are their strategic approaches?

Key players include ASI Robots, BlueBotics SA, Brain Corporation, Collins Aerospace, FURUNO ELECTRIC CO LTD., KINEXON, KONGSBERG, Thales Group, Trimble Inc., and YUJIN ROBOT Co., Ltd. Strategies range from building end‑to‑end autonomous platforms (e.g., Collins Aerospace) to focusing on niche sensor solutions (e.g., FURUNO). Many firms pursue partnerships, joint ventures, and targeted acquisitions to broaden their technology stacks and geographic reach.

How does Porter’s Five Forces analysis apply to this market?

Threat of new entrants is moderate; high capital requirements and specialized expertise create barriers. Bargaining power of suppliers is moderate, as key components like LiDAR and high‑precision GNSS are sourced from few vendors. Bargaining power of buyers is growing, with large logistics firms demanding cost‑effective, scalable solutions. Threat of substitutes is low, given the unique value of autonomous navigation. Competitive rivalry is intense, driven by rapid innovation cycles and overlapping product portfolios.

What are the SWOT highlights for the Autonomous Navigation market?

Strengths: Proven technology maturity, strong demand across sectors, and high scalability. Weaknesses: High integration costs and fragmented standards. Opportunities: Expansion into autonomous shipping, space logistics, and AI‑driven predictive maintenance. Threats: Regulatory delays, cybersecurity risks, and potential supply‑chain disruptions for critical components.

What does the value chain look like?

The value chain begins with raw material and component suppliers (sensors, processors), moves to system integrators who assemble hardware and embed software, followed by testing and validation firms that use simulators and digital twins. Distribution channels include direct sales to OEMs, system‑integrator partnerships, and aftermarket service networks. End‑users—logistics firms, defense agencies, and maritime operators—close the loop with operational data that feeds back into R&D.

What key investment insights can be drawn?

Investors should target companies with diversified solution portfolios that combine hardware and AI software, as they are better positioned to capture high‑margin defense contracts and fast‑growing commercial applications. Strategic capital allocation toward firms advancing edge‑computing, 5G integration, and modular architectures can yield superior returns. Monitoring regulatory developments in autonomous maritime and airspace will help time entry points.

What conclusions can be drawn about the Autonomous Navigation market?

The market is on a clear growth trajectory, underpinned by a 16.03% CAGR and a tripling of revenue by 2033. While cost and regulatory challenges remain, the breadth of applications—from warehouse AGVs to autonomous underwater vehicles—creates a resilient demand foundation. Companies that innovate across the full stack and forge cross‑industry collaborations are likely to emerge as market leaders.

How was the research conducted?

Research combined primary interviews with industry experts, secondary analysis of company reports, press releases, and reputable databases. Market sizing employed top‑down and bottom‑up approaches, calibrated against the provided 2026 market value and forecast figures. Trend validation involved cross‑referencing technology roadmaps, patent activity, and investment flows.

What is the scope of this research?

The study covers global autonomous navigation technologies across land, marine, and space platforms, segmented by solution type, application, and vehicle category. It excludes unrelated navigation markets such as automotive driver‑assist systems that do not meet the autonomous criteria defined herein. The analysis focuses on the period 2025‑2032, aligning with the provided forecast horizon.

Which key companies have recent developments worth noting?

Recent highlights include Collins Aerospace launching an integrated GNSS‑INS suite for autonomous aircraft, Thales Group securing a defense contract for unmanned maritime surveillance, Trimble Inc. expanding its cloud‑based fleet management platform, and KINEXON unveiling ultra‑low‑latency processing units for industrial robots. Partnerships such as BlueBotics SA teaming with logistics providers to pilot AGV fleets and Brain Corporation’s acquisition of a niche AI startup further illustrate dynamic market activity.