What is the Vendor Management Software Market Overview - Definition, scope, and significance?

Vendor Management Software (VMS) is a digital solution that enables organizations to automate, monitor, and optimize the entire vendor lifecycle—from selection and onboarding to performance evaluation and contract renewal. The market encompasses solutions delivered via cloud and on‑premise models, serving a range of enterprise sizes (large enterprises and SMEs) across verticals such as retail, manufacturing, BFSI, IT, and telecom. VMS is significant because it reduces procurement costs, improves compliance, enhances risk visibility, and drives strategic sourcing decisions in increasingly complex supply‑chain ecosystems.

What are the Vendor Management Software Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the growing need for supply‑chain transparency, rising regulatory scrutiny, and the acceleration of digital transformation initiatives that demand real‑time vendor data. Restraints stem from budget constraints in SMEs and integration complexities with legacy ERP systems. Challenges involve data security concerns and the talent gap for managing sophisticated analytics. Opportunities arise from the expansion of cloud‑based VMS, AI‑enabled risk scoring, and the emergence of niche solutions for high‑growth sectors such as fintech and e‑commerce.

What are the Vendor Management Software Market Growth Trends?

Current trends feature a shift toward cloud deployment, driven by scalability and lower upfront costs, while on‑premise solutions retain niche appeal for highly regulated industries. AI and machine‑learning modules are being embedded to predict vendor risk and automate contract compliance. Moreover, the market is witnessing increased adoption of modular, API‑first architectures that allow seamless integration with procurement, ERP, and spend‑analysis platforms, creating a more connected vendor ecosystem.

How has COVID‑19 impacted the Vendor Management Software Market?

The pandemic forced organizations to reassess supplier resilience, prompting a surge in demand for VMS tools that provide real‑time visibility into vendor health and supply‑chain disruptions. Remote work accelerated cloud migration, boosting cloud‑based VMS subscriptions. Recovery has been steady, with companies continuing to invest in digital vendor oversight as part of broader post‑pandemic risk‑management strategies.

What does the Vendor Management Software Market Competitive Landscape look like?

The market is moderately consolidated, with several established players holding strong footholds. Key competitors such as Coupa Software, SAP SE, IBM Corporation, and LogicManager offer end‑to‑end suites, while niche firms like Gatekeeper, HICX Solutions, and Intelex Technologies focus on specific functionalities or industry verticals. Recent years have seen strategic partnerships and acquisitions aimed at expanding AI capabilities and geographic reach.

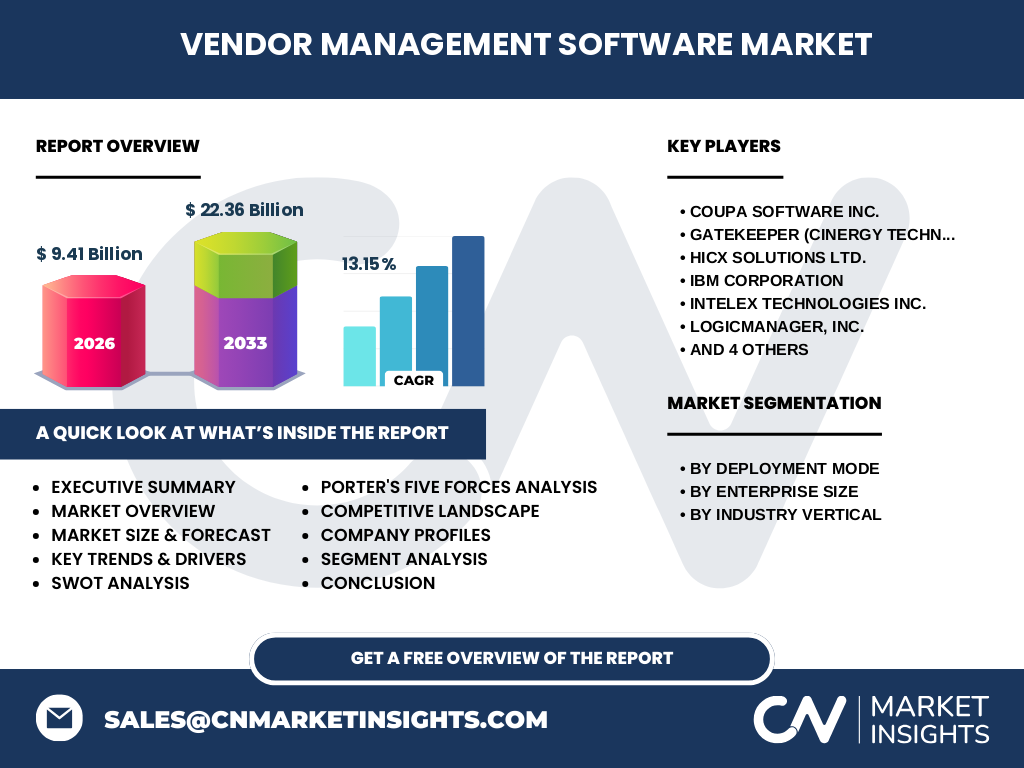

What are the main points of the Executive Summary?

The Vendor Management Software market is valued at $9.41 billion in 2026 and is projected to reach $22.36 billion by 2033, reflecting a robust CAGR of 13.15 %. Growth is driven by digital transformation, regulatory pressure, and the need for supply‑chain resilience. Cloud adoption is outpacing on‑premise, and AI‑enhanced analytics are becoming differentiators. Leading vendors are consolidating through acquisitions and expanding into emerging verticals, positioning the market for sustained expansion.

What are the Vendor Management Software Market Forecasts for 2025‑2032?

Based on the provided CAGR of 13.15 %, the market is expected to more than double its 2026 size by the early 2030s. This trajectory suggests consistent year‑over‑year growth, underpinned by increasing enterprise budgets for vendor risk management and the scaling of cloud platforms. The forecast period anticipates heightened adoption across both large enterprises and SMEs, with particular momentum in high‑growth verticals such as IT and telecom.

How is the Vendor Management Software Market Size and Share segmented?

Segmentation is defined across three dimensions. By deployment mode, the market splits between Cloud and On‑premise solutions, with Cloud gaining share due to flexibility and cost efficiency. By enterprise size, Large Enterprises dominate owing to complex supplier networks, while SMEs represent a fast‑growing segment seeking affordable, scalable VMS options. By industry vertical, the market serves Retail, Manufacturing, BFSI, IT, and Telecom, each requiring tailored vendor oversight capabilities.

What is the Global Vendor Management Software Market Size and Share by Region?

The global market totals $9.41 billion in 2026, with growth expected across all major regions. While specific regional monetary values are not disclosed, the market’s expansion reflects strong demand in North America, Europe, and Asia‑Pacific, driven by mature procurement functions and regulatory environments. Emerging markets are beginning to adopt cloud‑based VMS as digital infrastructure improves.

What does the Regional Analysis of the Vendor Management Software Market reveal?

North America leads adoption due to high enterprise spending on risk management and early cloud uptake. Europe follows, emphasizing data‑privacy compliance that fuels VMS investment. Asia‑Pacific shows the fastest growth rate, propelled by rapid industrialization, expanding manufacturing bases, and increasing IT spend. Latin America and the Middle East exhibit moderate growth, with SMEs driving much of the demand for cost‑effective cloud solutions.

Who are the leading companies in the Vendor Management Software Market and what are their strategies?

Key players include Coupa Software Inc., SAP SE, IBM Corporation, LogicManager, Inc., and MasterControl Inc. Their strategies center on expanding AI analytics, strengthening partner ecosystems, and pursuing vertical‑specific solutions. Smaller innovators such as Gatekeeper, HICX Solutions, and Intelex Technologies focus on niche compliance modules and integration capabilities. Acquisitions and joint ventures are common tactics to broaden product portfolios and accelerate market penetration.

How does Porter’s Five Forces analysis apply to the Vendor Management Software Market?

• Threat of new entrants – Moderate; high development costs and the need for integration expertise create barriers, yet cloud platforms lower entry thresholds. • Bargaining power of buyers – High; enterprises can negotiate pricing across multiple vendors and demand extensive customization. • Bargaining power of suppliers – Low; most VMS providers develop core software in‑house, with limited reliance on third‑party components. • Threat of substitutes – Low to moderate; traditional manual vendor management remains a substitute but lacks scalability. • Industry rivalry – Intense; major players vie on AI features, cloud pricing models, and industry‑specific compliance tools.

What are the SWOT insights for the Vendor Management Software Market?

Strengths: Strong growth momentum, clear value proposition for risk reduction, and increasing cloud adoption. Weaknesses: Integration challenges with legacy systems and varying maturity across SMEs. Opportunities: AI‑driven risk analytics, expansion into under‑served verticals, and geographic growth in APAC. Threats: Cybersecurity concerns, potential economic slowdowns affecting IT budgets, and regulatory changes that may require rapid product adaptation.

What does the Vendor Management Software Market Value Chain look like?

The value chain begins with research & development of core VMS platforms, followed by cloud infrastructure provisioning or on‑premise installation services. Next, vendors deliver integration consulting, customization, and training to end‑users. Ongoing support, data analytics, and compliance updates constitute post‑implementation services, creating recurring revenue streams through subscriptions, maintenance contracts, and add‑on modules.

What key investment insights can be drawn from the Vendor Management Software Market?

Investors should focus on companies with strong cloud SaaS models, robust AI capabilities, and proven integration frameworks. Firms expanding into high‑growth verticals such as IT and telecom, or those forging strategic alliances with ERP providers, present attractive upside. Monitoring M&A activity can reveal consolidation trends that may open avenues for partnership or acquisition.

What are the main conclusions of the Vendor Management Software Market analysis?

The Vendor Management Software market is on a steep growth trajectory, driven by digital transformation, regulatory pressure, and the need for resilient supply chains. Cloud adoption and AI‑enhanced risk analytics are reshaping competitive dynamics. While integration and security remain challenges, the market offers substantial opportunities for vendors that can deliver scalable, compliant, and intelligent solutions across diverse industries.

What research methodology was employed for this market study?

The analysis combined primary interviews with industry experts, secondary data collection from reputable market reports, and financial modeling based on the provided market size, forecast, and CAGR. Segmentation frameworks were applied to categorize deployment modes, enterprise sizes, and verticals, while trend analysis leveraged macro‑economic and technology adoption indicators.

What is the scope of this research?

The study covers global Vendor Management Software offerings across cloud and on‑premise deployments, addressing large enterprises and SMEs in retail, manufacturing, BFSI, IT, and telecom sectors. It excludes detailed regional revenue breakdowns beyond the provided aggregate figures and does not quantify market share percentages for individual vendors.

Which key companies and recent developments are shaping the Vendor Management Software Market?

Leading firms such as Coupa Software, SAP SE, and IBM Corporation have announced AI‑driven risk scoring modules and expanded partner networks with major ERP providers. Ncontracts introduced a new compliance dashboard targeting BFSI clients, while LogicManager launched a cloud‑first suite for telecom operators. Recent product launches include Gatekeeper’s on‑premise security module and MasterControl’s integration with manufacturing execution systems, underscoring the market’s focus on vertical customization and advanced analytics.