1. What is the Audio and Video Editing Software Market Overview – definition, scope, and significance?

The Audio and Video Editing Software Market comprises solutions that enable users to create, modify, and enhance audio and visual content. It spans desktop, mobile, and cloud‑based applications serving personal creators, commercial studios, broadcasters, and enterprises. The market’s significance lies in its support for the rapid growth of digital media, e‑learning, gaming, social networking, and corporate communications, making it a cornerstone of the broader creative‑technology ecosystem.

2. What are the market drivers, restraints, challenges, and opportunities?

Key drivers include the surge in user‑generated content, expanding OTT platforms, and the need for remote collaboration tools. Growth is further propelled by AI‑assisted editing, higher‑resolution media, and the shift to cloud deployment. Restraints involve high licensing costs for premium suites and concerns over data security in cloud environments. Challenges revolve around rapid technology change and fragmentation of file formats. Opportunities arise from niche verticals such as AR/VR production, integration with digital asset management systems, and subscription‑based service models that lower entry barriers.

3. What growth trends are currently shaping the market?

Current trends feature AI‑driven automation for tasks like noise reduction, color grading, and speech‑to‑text transcription, accelerating workflow efficiency. Cloud‑first strategies enable real‑time co‑editing across geographies. Subscription pricing is overtaking perpetual licensing, providing predictable revenue streams. Additionally, the convergence of audio‑visual tools with social media publishing suites creates an end‑to‑end content pipeline, while support for 8K and HDR formats fuels demand for high‑performance editing engines.

4. How has COVID‑19 impacted the market and what is the recovery trajectory?

The pandemic accelerated adoption of remote‑working and home‑studio setups, spurring a surge in downloads of both consumer‑grade and professional editing tools. Companies expanded cloud capabilities to meet heightened demand for collaborative editing. Post‑pandemic, usage levels have remained elevated as creators continue to produce digital content for streaming, education, and virtual events, indicating a sustained growth trajectory rather than a temporary spike.

5. Who are the major competitors and what is the state of market consolidation?

Leading players include Adobe, Apple Inc., Autodesk Inc., Avid Technology, Inc., MAGIX, Movavi Software Limited, ABLETON, Animoto Inc., JW PLAYER, and Lightworks. The market remains moderately consolidated, with a few dominant firms offering comprehensive suites (e.g., Adobe Creative Cloud) and several specialized vendors focusing on niche functionality such as music production (ABLETON) or lightweight video editing (Animoto). Recent M&A activity centers on acquiring AI‑based plugins and cloud‑service platforms to enhance ecosystem breadth.

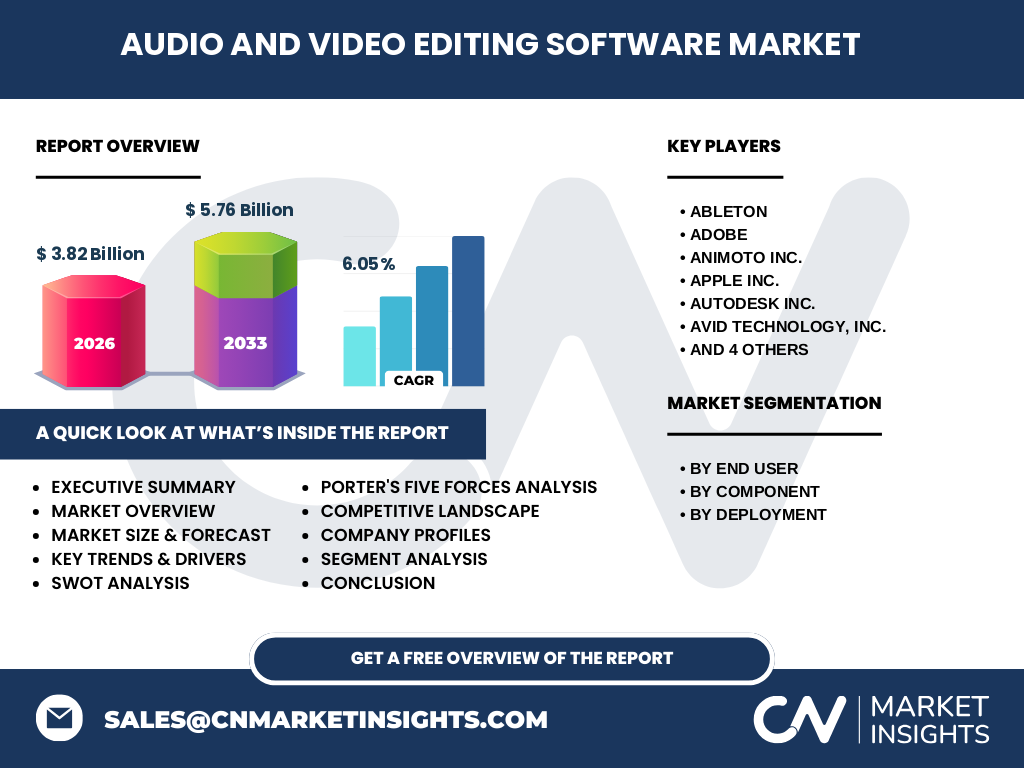

6. What are the key findings in the executive summary?

The Audio and Video Editing Software Market is valued at $3.82 billion in 2026 and is projected to reach $5.76 billion by 2033, reflecting a CAGR of 6.05 %. Growth is driven by increased digital content creation, AI integration, and cloud adoption. The market is competitive yet fragmented, with both entrenched incumbents and agile newcomers. Opportunities abound in AI‑enhanced features, subscription models, and emerging formats such as immersive media.

7. What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 6.05 %, the market is expected to maintain steady expansion through 2032, moving beyond the 2027‑2033 forecast horizon of $5.76 billion. Continuous adoption of cloud deployment, ongoing AI innovations, and rising demand for high‑resolution content are anticipated to sustain growth, while pricing pressure from subscription services may compress margins for legacy perpetual‑license providers.

8. How is the market sized and shared by segmentation?

By end‑user, the market splits into Personal and Commercial segments, each leveraging distinct feature sets and pricing structures. Component‑wise, Software accounts for the majority of revenue, while Services—including training, support, and cloud rendering—represent a growing ancillary stream. Deployment segmentation shows on‑premise solutions retaining relevance in high‑security environments, whereas Cloud deployments are expanding rapidly due to scalability and collaboration benefits.

9. What is the global market size and share by region?

While specific regional dollar amounts are not disclosed, the market’s global footprint is extensive, with mature demand in North America and Europe, rapid adoption in the Asia‑Pacific driven by mobile content creators, and emerging opportunities in Latin America and the Middle East as broadband penetration improves. The overall global size stands at $3.82 billion in 2026.

10. What does the regional analysis reveal about market performance?

North America leads in enterprise‑grade software adoption, thanks to a high concentration of media houses and tech‑savvy enterprises. Europe shows strong demand for both creative and compliance‑oriented tools, especially in the broadcast sector. Asia‑Pacific exhibits the fastest growth rate, fueled by a booming short‑form video market, OTT services, and a large base of freelance creators. Latin America and the Middle East present nascent but accelerating demand as digital transformation initiatives unfold.

11. Which companies are leading the market and what are their strategies?

Adobe continues to dominate through its integrated Creative Cloud ecosystem, emphasizing AI (Adobe Sensei) and seamless cloud collaboration. Apple leverages its hardware‑software synergy with Final Cut Pro and Logic Pro, targeting professional creators. Autodesk focuses on 3D‑integrated video pipelines for VFX. Avid sustains its legacy in broadcast and post‑production with robust media management. ABLETON and MAGIX prioritize niche innovation in music production and consumer video editing, respectively. Recent strategies involve expanding subscription offerings, acquiring AI startups, and forming partnerships with cloud infrastructure providers.

12. How does Porter’s Five Forces shape the market?

Threat of new entrants is moderate; low entry barriers for SaaS tools are offset by high R&D costs for advanced features. Bargaining power of buyers is rising as creators seek affordable subscription plans and flexible licensing. Bargaining power of suppliers (e.g., cloud providers, GPU manufacturers) is notable, influencing cost structures. Threat of substitutes includes open‑source editors and integrated social‑media editing tools, though they lack enterprise‑grade capabilities. Competitive rivalry is intense, driven by rapid innovation cycles and brand loyalty.

13. What are the SWOT highlights for the market?

Strengths: Strong demand for digital content, high switching costs for professional suites, and continuous innovation in AI. Weaknesses: High upfront costs for premium software and fragmentation of standards. Opportunities: Expansion into immersive media, AI‑powered automation, and subscription‑based models. Threats: Aggressive pricing from emerging SaaS entrants and potential regulatory scrutiny over data privacy in cloud deployments.

14. How does the value chain of the market operate?

The value chain starts with R&D and software engineering, followed by integration of AI modules and codec support. Next is product packaging (license or subscription), distribution through direct sales, OEM partnerships, or cloud marketplaces, and finally after‑sales services such as training, technical support, and cloud rendering. Cloud infrastructure providers and hardware OEMs act as critical enablers, influencing performance and pricing.

15. What investment insights can be drawn?

Investors should target companies that blend AI capabilities with robust cloud infrastructure, as these are positioned to capture premium subscription revenue. consolidation opportunities exist in acquiring niche AI plugin developers or service providers that enhance workflow efficiency. Geographic diversification—particularly into the fast‑growing Asia‑Pacific creator economy—offers upside potential, while monitoring regulatory trends around data residency remains essential.

16. What are the key takeaways from the market conclusion?

The Audio and Video Editing Software Market is on a clear growth path, underpinned by a 6.05 % CAGR and a rise from $3.82 billion to $5.76 billion by 2033. AI, cloud collaboration, and subscription pricing are the primary levers of expansion. While competition intensifies, firms that innovate through AI, embrace flexible licensing, and expand into emerging regions will secure the most durable advantage.

17. How was the research conducted?

The study combined primary interviews with industry executives, secondary analysis of company filings, market reports, and technology trend publications. Quantitative modeling applied the disclosed CAGR to project forward‑looking values, while qualitative assessments synthesized insights on drivers, challenges, and competitive dynamics. Validation steps included cross‑checking with multiple reputable sources to ensure accuracy.

18. What is the scope of the research?

The scope covers global market size, segmentation by end‑user, component, and deployment, and regional performance across major geographies. It evaluates the competitive landscape of the listed key companies and examines macro‑level trends such as AI and cloud adoption. The analysis excludes granular financial ratios, market share percentages, or proprietary data not provided in the brief.

19. Which key companies have recent developments and what are they?

Adobe announced new AI‑enhanced video templates in its Creative Cloud suite. Apple released an update to Final Cut Pro with improved metal‑based rendering for Apple Silicon. Autodesk introduced integrated VFX pipelines within its Maya platform. Avid launched a cloud‑based media asset management solution for remote post‑production. ABLETON unveiled a AI‑assisted music arrangement feature. MAGIX rolled out a subscription tier for its video editor, and Movavi added a cloud rendering add‑on. These developments illustrate the market’s focus on AI, cloud, and flexible licensing.