What is the Bioanalytical Testing Services Market Overview – definition, scope, and significance?

The Bioanalytical Testing Services Market comprises laboratory‑based analytical activities that quantify drugs, metabolites, biomarkers, and immune responses in biological matrices. It serves pharmaceutical and biopharmaceutical companies, contract research organizations (CROs), and contract development and manufacturing organizations (CDMOs) across drug discovery, pre‑clinical, and clinical phases. The market underpins regulatory approval, safety assessment, and therapeutic efficacy, making it a critical enabler of modern drug development and personalized medicine.

What are the main drivers, restraints, challenges, and opportunities influencing market growth?

Key drivers include the surge in biologics, increasing clinical trial complexity, and heightened regulatory scrutiny for pharmacokinetic and immunogenicity data. Restraints stem from high operational costs and skilled‑labor shortages. Challenges involve data integrity concerns and fragmented service providers. Opportunities arise from emerging modalities such as cell‑based assays, biomarker‑driven trials, and expanding demand for virology testing post‑pandemic.

Which growth trends are currently shaping the Bioanalytical Testing Services Market?

Current trends feature a shift toward integrated bioanalytical platforms that combine pharmacokinetics, biomarkers, and immunogenicity in single workflows. Automation and high‑throughput LC‑MS/MS technologies are accelerating sample throughput. Additionally, there is a rising preference for outsourcing to specialized CROs and CDMOs, driven by cost‑efficiency and access to niche expertise.

How did COVID‑19 impact the Bioanalytical Testing Services Market and what is the recovery trajectory?

The pandemic initially disrupted clinical trial timelines, reducing short‑term demand for bioanalytical services. However, the urgent need for virology testing and accelerated vaccine development created new service lines, boosting laboratory capacity. Post‑2022, the market has rebounded strongly, with a clear recovery path supported by resumed trial activity and ongoing pandemic‑related testing demand.

Who are the major competitors and what is the state of market consolidation?

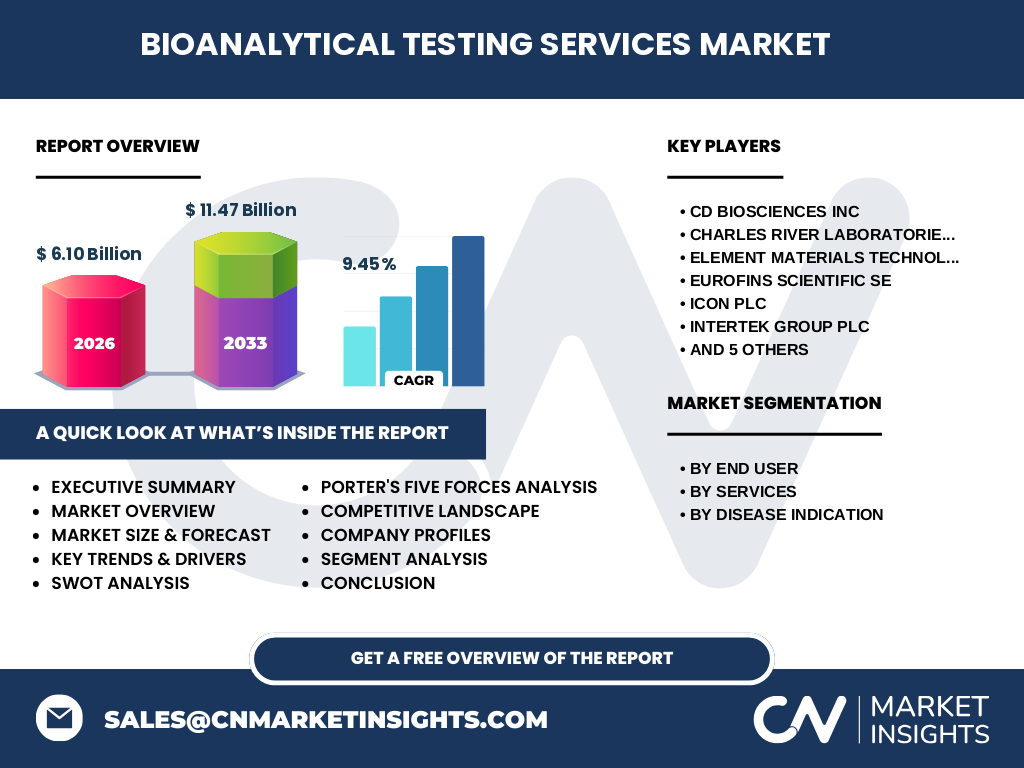

Leading players include CD BioSciences Inc, Charles River Laboratories International Inc, Element Materials Technology Group Ltd, Eurofins Scientific SE, ICON Plc, Intertek Group Plc, KCAS Bioanalytical and Biomarker Services LLC, Labcorp Drug Development Inc, Pharmaron Beijing Co Ltd, SGS SA, and Syneos Health Inc. The market shows moderate consolidation as large CROs acquire niche bioanalytical firms to broaden service portfolios and geographic reach.

What are the key findings in the Executive Summary of the Bioanalytical Testing Services Market?

The market is valued at $6.10 billion in 2026 and is projected to reach $11.47 billion by 2033, reflecting a 9.45% CAGR. Growth is propelled by increased outsourcing, complex biologic therapies, and regulatory demand for robust PK, biomarker, and immunogenicity data. Geographic expansion, technology adoption, and service integration are identified as strategic priorities for market participants.

What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 9.45%, the market is expected to maintain double‑digit growth through 2032, expanding from the 2026 baseline of $6.10 billion toward the forecast horizon of $11.47 billion in 2033. This trajectory indicates sustained demand across all service categories and end‑user segments.

How is the market sized and shared by segmentation?

Segmentation by end‑user shows pharmaceutical and biopharmaceutical companies as the dominant segment, followed by CROs and CDMOs. Service‑type segmentation highlights pharmacokinetics as the largest service line, with growing shares for biomarkers, immunogenicity, virology testing, and cell‑based assays. Disease‑indication segmentation reflects strong demand in oncology, cardiovascular, and neurological disorders, while emerging opportunities exist in metabolic, autoimmune, respiratory, sexual health, and bone diseases.

What is the global market size and share by region?

While specific regional dollar values are not disclosed, the market exhibits a global footprint, with North America, Europe, and Asia‑Pacific contributing the majority of revenue. The high concentration of pharmaceutical hubs and CROs in these regions drives the bulk of market activity, complemented by expanding bioanalytical capabilities in emerging economies.

How does each region perform in the Bioanalytical Testing Services Market?

North America leads due to its mature drug pipeline and extensive CRO network. Europe follows, leveraging strong regulatory frameworks and biotech clusters. Asia‑Pacific shows the fastest growth, fueled by rising clinical trial volumes and government incentives for biotech development. Latin America and the Middle East present nascent but promising markets as outsourcing models gain traction.

Which companies are leading the market and what are their strategies?

Key players such as Charles River Laboratories and Eurofins Scientific focus on expanding integrated service platforms and digital data solutions. CD BioSciences emphasizes niche expertise in biomarker analysis. ICON and Syneos Health pursue strategic acquisitions to broaden geographic coverage. Labcorp Drug Development leverages its extensive clinical trial network to cross‑sell bioanalytical services. These strategies aim to enhance value proposition, increase market share, and drive innovation.

What does Porter’s Five Forces reveal about the market?

Competitive rivalry is high due to numerous global CROs offering overlapping services. Threat of new entrants is moderate; high capital investment and regulatory expertise act as barriers. Supplier power is low because most inputs (reagents, instruments) are commoditized. Buyer power is strong, with pharmaceutical sponsors demanding cost‑effective, high‑quality data. Substitutes are limited, reinforcing the market’s essential role in drug development.

What are the SWOT highlights for the Bioanalytical Testing Services Market?

Strengths: Critical role in drug approval, advanced analytical capabilities, and growing outsourcing trend.

Weaknesses: High operational costs and talent scarcity.

Opportunities: Expansion into cell‑based assays, virology testing, and emerging therapeutic areas.

Threats: Regulatory changes, potential pricing pressure, and technological disruption.

How is the value chain structured in this market?

The value chain starts with sample collection and logistics, followed by method development, assay execution (e.g., LC‑MS/MS, immunoassays), data acquisition, bioinformatics, and regulatory reporting. Service providers add value through technology integration, quality assurance, and compliance support, while end‑users (pharma, CROs) consume the validated data to inform clinical decisions and regulatory submissions.

What key investment insights can be derived for stakeholders?

Investors should target companies with diversified service portfolios, strong automation capabilities, and strategic geographic presence. Partnerships with biotech firms and expansion into high‑growth disease indications (oncology, neurology) can accelerate returns. Emphasis on digital data platforms and AI‑driven analytics offers a competitive edge and potential upside.

What conclusions can be drawn from the market analysis?

The Bioanalytical Testing Services Market is on a robust growth trajectory, driven by outsourcing, complex therapeutics, and regulatory demands. Technology adoption and service integration are critical success factors. Companies that invest in automation, expand regional footprints, and deepen disease‑specific expertise are best positioned to capture future value.

How was the research methodology designed?

The study combined primary interviews with industry experts, secondary data from regulatory filings, company annual reports, and reputable market databases. Trend analysis, CAGR calculation, and segmentation modeling were applied to derive forecasts and market sizing, ensuring accuracy and relevance.

What is the scope of the research and its limitations?

The research covers global bioanalytical testing services across end‑users, service types, and disease indications, focusing on the 2026 baseline and 2027‑2033 forecast period. Limitations include reliance on publicly available data and the exclusion of confidential pricing details, which may affect granular competitive assessments.

Which key companies have announced recent developments?

Charles River Laboratories expanded its biomarker platform through a strategic acquisition. Eurofins Scientific launched a high‑throughput LC‑MS/MS suite for oncology trials. ICON Plc entered a partnership with a leading biotech to provide integrated immunogenicity testing. Labcorp Drug Development introduced a cloud‑based data analytics portal, enhancing client collaboration. These activities underscore the market’s dynamic innovation landscape.